Visa’s payment processing throne is a masterclass in network economics 👏😤; Mastercard’s wide moat justifies premium valuation 📈💳

FinTech is Eating the World, 13 November

Hey Everyone,

Good morning & happy Thursday! Today’s issue is a special one as we’re going to dive deep into the latest earnings of two of the most powerful payments companies in the world 💳 As you’re well aware, we’re looking into Visa’s payment processing throne, which is a masterclass in network economics (deep dive into their 4Q 2025 earnings, breaking down the most important facts & figures, and what’s next for the payments heavyweight + bonus dives into Visa’s Trusted Agent Protocol & more reads on agentic finance inside), and Mastercard’s wide moat that justifies its premium valuation (breaking down the most important facts & figures from their 3Q 2025 earnings, understanding what they mean and whether Mastercard is worth your time and money in 2025 & beyond). So let’s just jump straight into the interesting stuff 🌶️

Visa’s payment processing throne is a masterclass in network economics 👏😤

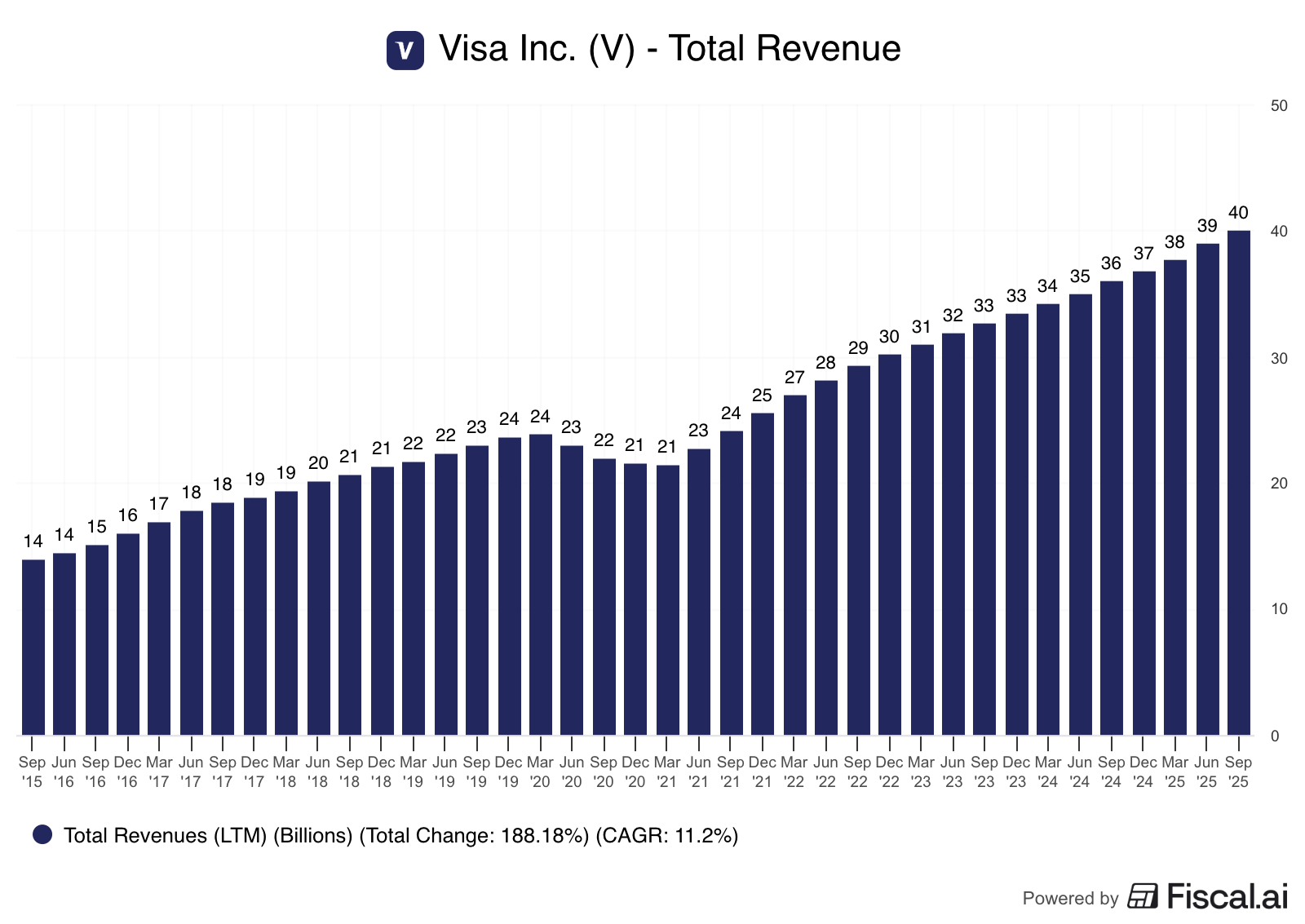

Following the money 🤑 Finance titan Visa just delivered a textbook display of wide-moat dominance in fiscal 2025, posting a whopping $40 billion in net revenue (up 11% YoY) and non-GAAP EPS of $11.47 (up 14% YoY), while generating $21.6B in free cash flow and returning $22.8B to shareholders. Let that sink in… 🤯

The numbers perfectly illustrate what separates Visa from ordinary businesses: a payment processing tollbooth with 257.5B transactions globally, 4B cards in circulation, and an operating margin on net revenue approaching 67%. This isn’t just growth - it’s scalable, capital-light compounding at its finest 👏

Let’s dive deeper into Visa’s latest earnings, break down the most important facts & figures, and see what’s next for the payment heavyweight.