World’s Tollbooth: Visa’s unbeatable moat justifies premium valuation, but upside is limited 🤷♂️💳; Permanent Number Two: Mastercard’s quality is unquestionable, but so is the valuation 🤔📈

FinTech is Eating the World, 4 February

Hey Everyone,

Good day & happy Wednesday! Today, all eyes are on two of the most powerful companies in payments, as we’re going to dive deep and break down the latest financials of Visa (breaking down the most important Q1 2026 financial facts & figures, understanding what they mean, and what’s next for Visa), and Mastercard (deep dive into their Q4 2026, what stood out and whether Mastercard is worth your time & money in the years to come). So let’s jump straight into the interesting stuff 🌶️

World’s Tollbooth: Visa’s unbeatable moat justifies premium valuation, but upside is limited 🤷♂️💳

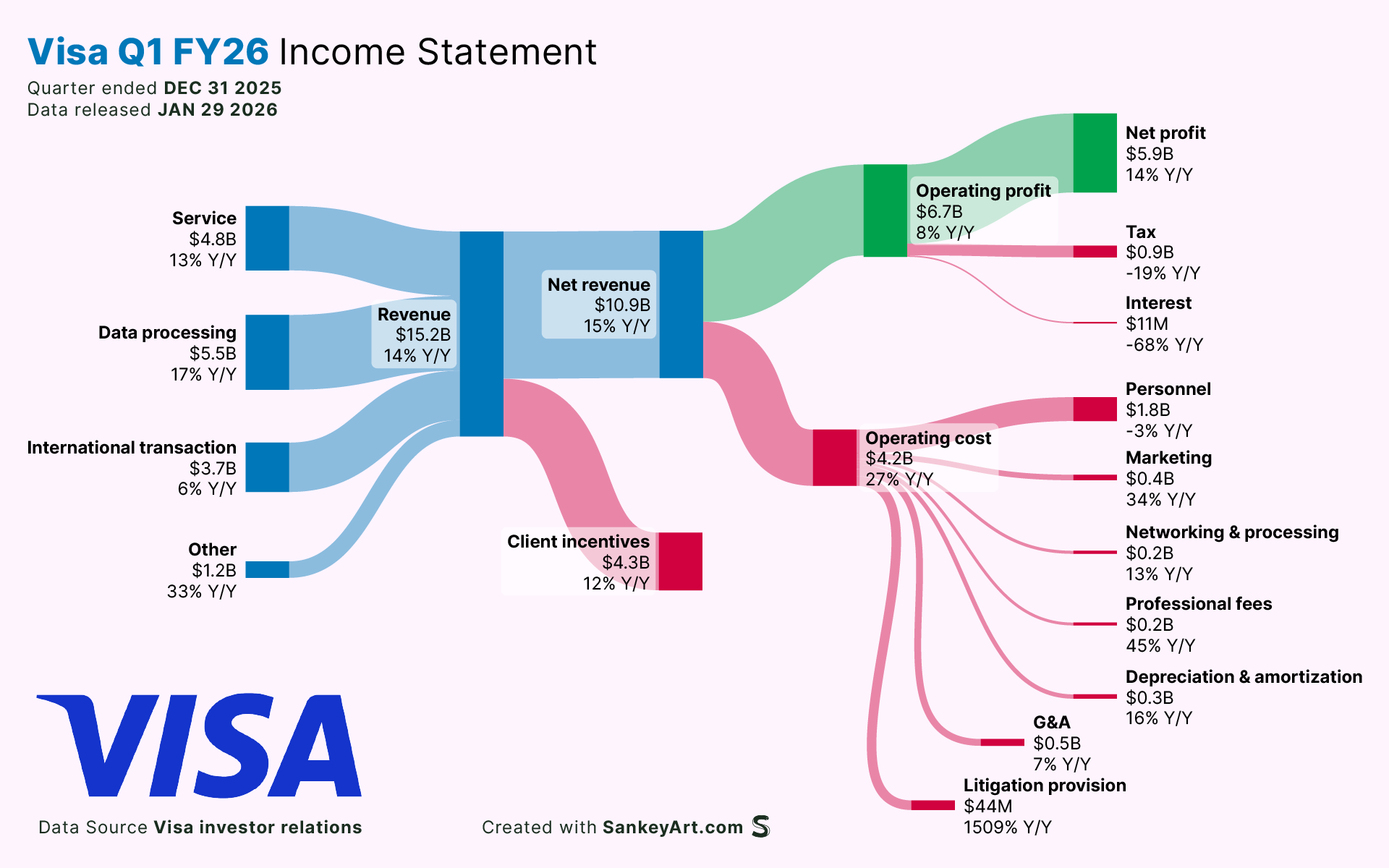

Earnings time 🤑 Every time you tap a card or check out online, Visa V 0.00%↑ takes a cut. The company operates what amounts to a digital tollbooth on roughly $17 trillion in annual payment volume, making it one of the most elegant business models ever built in finance.

Visa’s Q1 FY2026 results confirm the machine keeps delivering: net revenue of $10.9 billion (up 15% year-over-year), EPS of $3.17 (up 15%), and free cash flow of $6.4 billion. With 56% non-GAAP net margins, ROIC exceeding 90% when excluding goodwill, and a wide economic moat, Visa meets virtually every criterion for a fundamentally sound long-term investment.

The problem is the price. At ~$330, trading already at a fair value estimate and 30x earnings, the risk/reward is balanced rather than compelling.

Let’s dive deeper into this, break down the most important financial facts & figures, understand what they mean, and see what’s next for Visa.