Toll booth on internet’s money highway: Circle’s $75B stablecoin empire is printing cash, but yield curve is its landlord 🤷♂️🏦; Revolut is building a valuation staircase to a $150B IPO 😳📈

FinTech is Eating the World, 26 February

Hey Everyone,

Good morning & happy Thursday! Today’s issue is focused on going deep into Circle, the toll booth on the internet’s money highway (deep dive into their latest Q4 2025 financials, breaking down the most important facts & figures, and why Circle is one of the most interesting risk/reward setups in fintech right now + bonus deep dive into its key partner Coinbase inside), and Revolut, which soon could be worth a whopping $100 billion (what’s the bigger play here, why it matters & what’s next + bonus dive into Revolut, and how it’s brilliantly leveraging AI inside). So let’s jump straight into the awesome stuff 🌶️

The toll booth on the internet’s money highway: Circle’s $75B stablecoin empire is printing cash, but the yield curve is its landlord 🤷♂️🏦

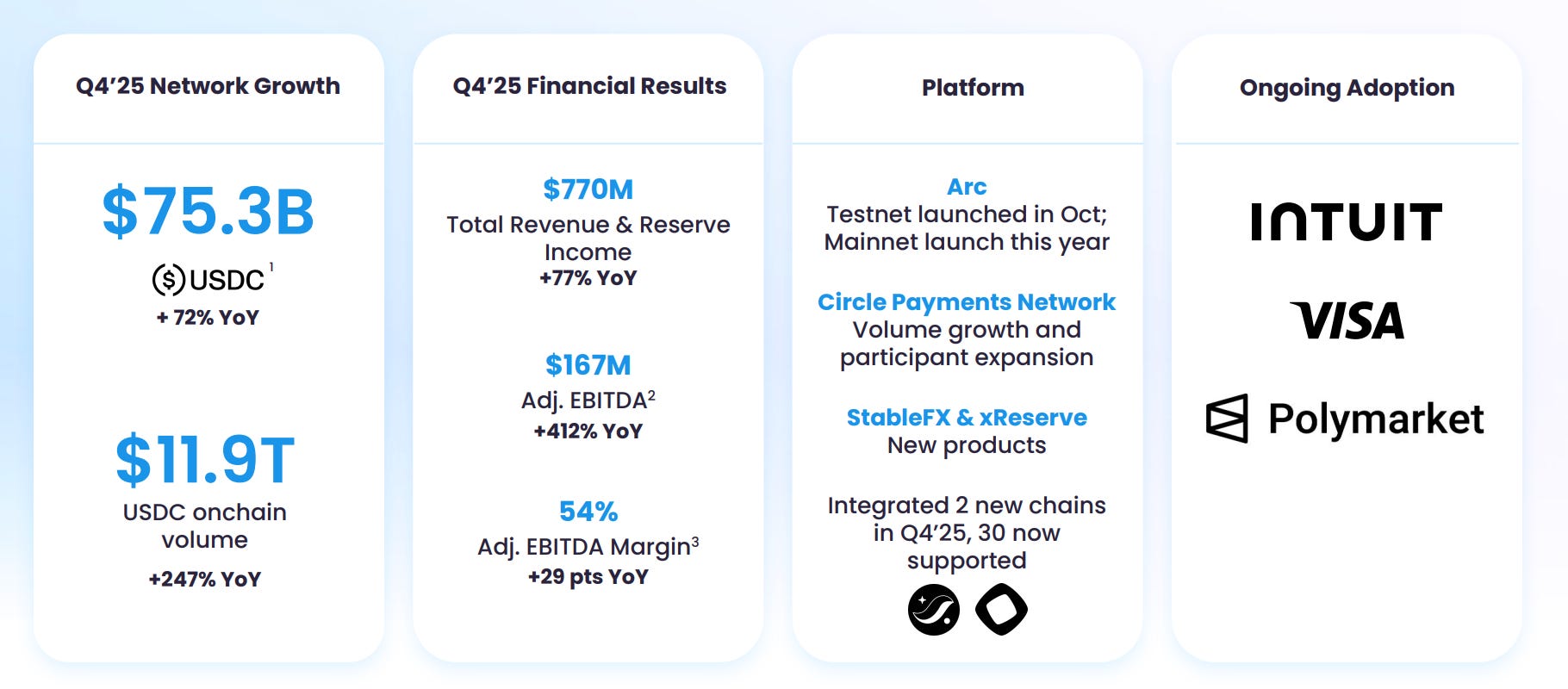

Earnings time ☎️ Stablecoin giant Circle CRCL 0.00%↑ just dropped its Q4 and full-year 2025 earnings, and the results tell the story of a company caught between explosive adoption and a macro variable it cannot control.

The stock currently trades around $80, down roughly 75% from its all-time high of ~$250 reached just weeks after its June 2025 IPO at $31, implying a market cap of ~$20 billion 😳

The chart looks brutal, but consider what that valuation buys: a company that generated $2.75 billion in revenue in FY25 (up 64% YoY), issued $75.3 billion worth of the world’s second-largest stablecoin, processed $11.9 trillion in on-chain transaction volume in Q4 alone, and just beat consensus on both revenue and EPS by wide margins.

The market is pricing Circle at roughly 26x adjusted EBITDA for a business where USDC circulation is compounding at 72% YoY, new revenue streams are emerging, and regulatory moats are deepening. The catch? 96% of revenue comes from interest on T-bill reserves - which means the Fed, not management, holds the biggest lever on Circle’s P&L. That tension between growth and rate sensitivity is what makes Circle one of the most interesting risk/reward setups in fintech right now.

Let’s dive deeper into Circle’s latest financials, break down the most important facts & figures, understand what they mean, and see why CRCL 0.00%↑ deserves a closer look.