Japan’s cash graveyard just found its gravedigger: why PayPay may be the most asymmetric FinTech IPO of the decade 😳🇯🇵

FinTech is Eating the World, 10 March

Hey Everyone,

Good morning & happy Tuesday! FinTech IPOs are back, so today all eyes are on Japanese mobile payments giant PayPay that's expected to price this week on the Nasdaq under the ticker $PAYP 🔔 We're talking about a SoftBank-backed Super App with 72 million users that just went from burning cash to printing 30% EBITDA margins in just under 2 years, and now it's coming to market at a valuation that got marked down from ~$19.6B to ~$12.4B thanks to macro jitters, not business problems 😳 We're going to unpack the closed-loop payments model, the lending engine hiding inside, and the SoftBank governance question to figure out whether this is the most asymmetric fintech IPO setup in years (plus, cornerstone bets from Visa, Qatar Holding, and Abu Dhabi Investment Authority tell you the smart money is already paying attention & a bonus dive into Brazil’s PicPay inside). Let’s jump straight into the fascinating stuff 🌶️

Japan’s cash graveyard just found its gravedigger: why PayPay may be the most asymmetric FinTech IPO of the decade 😳🇯🇵

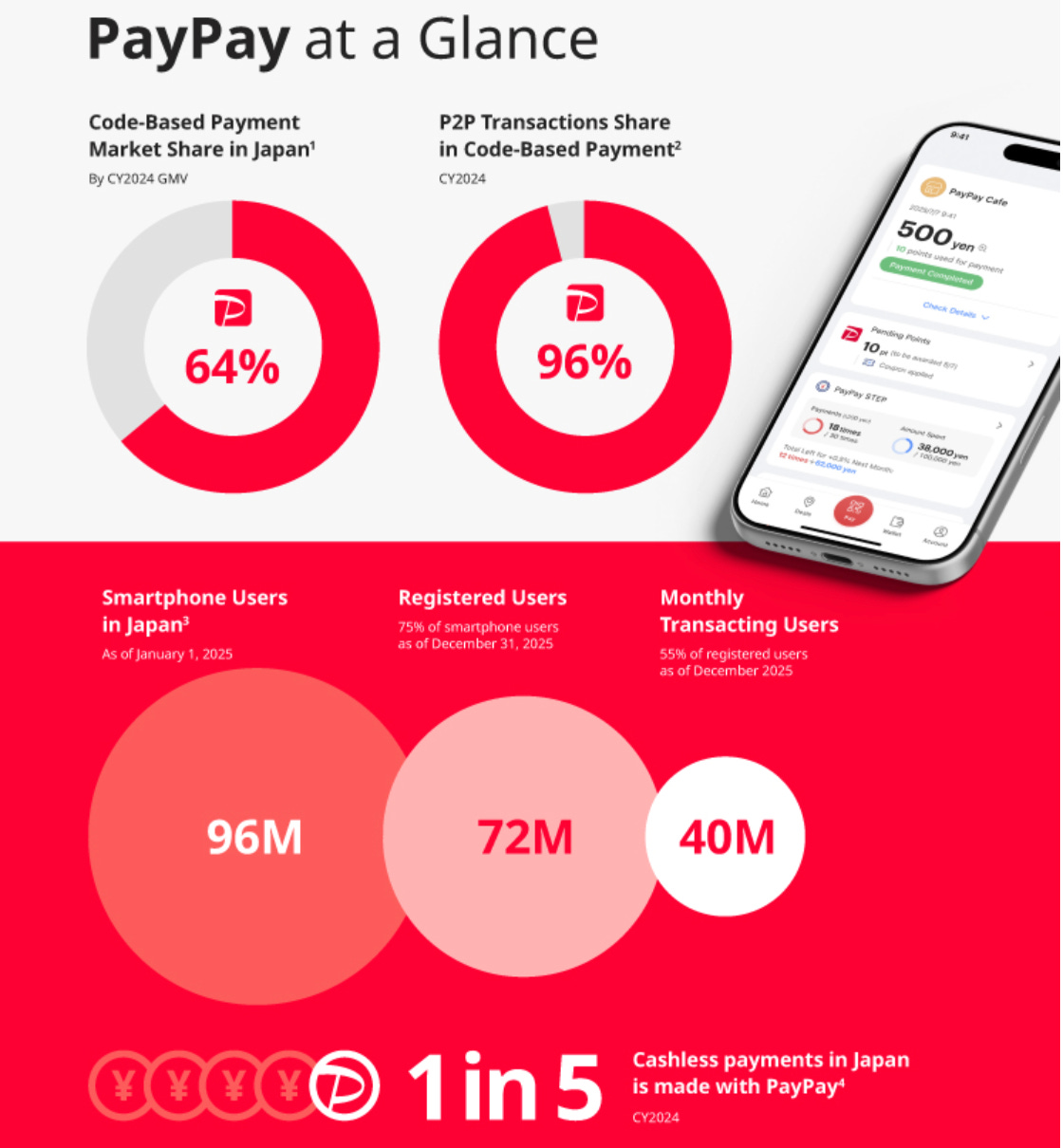

Following the money 🤑 FinTech IPOs are back, and Japanese FinTech giant PayPay Corporation is bringing to the U.S. public markets what amounts to a monopoly-in-formation over Japan’s ¥273 trillion (~$1.8 trillion) consumer payments economy.

At an IPO price range of $17-$20 per ADS, implying a fully diluted market cap of ~$11.4–$13.4 billion on approximately 669 million shares outstanding, we are being offered a company with 72 million registered users (75% smartphone penetration in Japan), ¥15.39 trillion (~$103B) in annual Payment Segment GMV, and a business that just flipped from operating losses to a 22% operating margin in 9 months 🤯

Most importantly, every trend line is still accelerating.

The initial valuation target was reportedly above $19.6 billion. Macroeconomic headwinds and a relatively weak fintech IPO market pushed that down to the current range of ~$12-$13B. The markdown is exactly what makes this fintech opportunity more attractive, not less.

Let’s dive in.