Adyen + Tink, or why the future of payments is open 💸; Crypto is here to stay. And it's time to talk about MENA 🚀; Lessons from another failed neobank 🧠

FinTech is Eating the World, 6 October

Hey Everyone,

Happy Thursday! Today’s issue is super interesting as it focuses on the global shifts that are changing the status quo in FinTech. We’re going to look at Adyen partnering with Tink, or why the future of payments is open (& why Open Banking is the Next BIG Thing in FinTech since plastic + Adyen’s quest to become a FinTech powerhouse), see why crypto + MENA is a winning combination (if you’re in crypto biz, you just can’t ignore this!), and try to unlock the lessons from another failed neobank (bonus is a read on how to swim in the world of sinking neobanks). Let’s jump straight into the awesome stuff:

Adyen + Tink, or why the future of payments is open 💸

The deal 🤝 Netherlands-based global FinTech giant Adyen has partnered with Open Banking platform Tink to enable its customers to offer open banking payments.

More on this 👉 Adyen will tap Tink’s payment initiation technology to enable businesses to access account-to-account payments, beginning in the UK with more markets to follow in 2023.

We must note that the agreement builds on a partnership Adyen and Tink already have for Account Check technology, which lets Adyen’s customers instantly verify account ownership to streamline payouts.

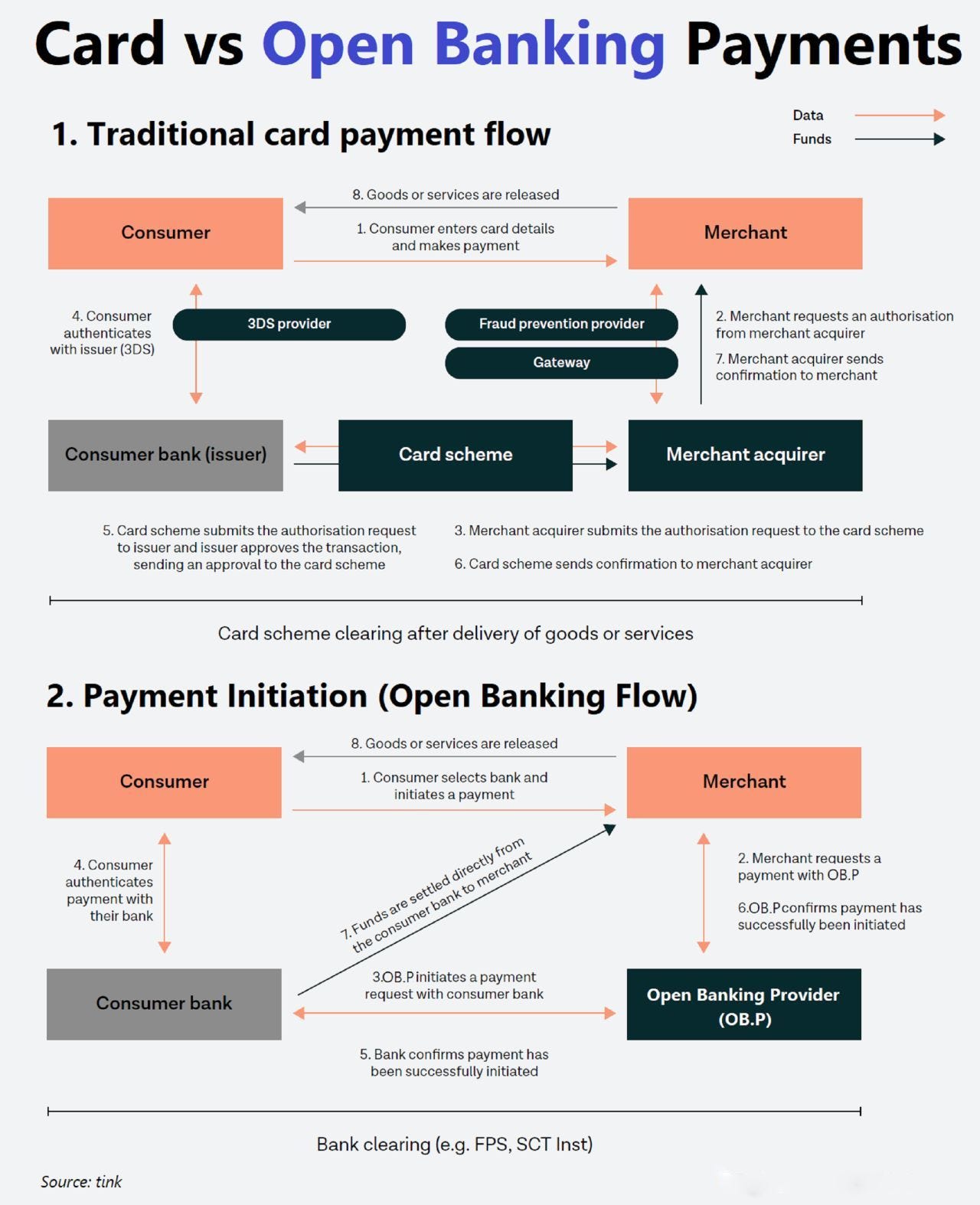

A refresher 💦 Before we dive further, here’s a brilliant graph showing the difference in card vs. open banking payment flow:

Why is this important? 🤔 First and foremost, it yet again shows that Open Banking is the Next BIG Thing in FinTech since plastic. Secondly, it furthermore proves that Adyen is an underrated FinTech giant that could soon emerge as a leading global powerhouse when it comes to all things Finance.

Here’s more on that + the takeaway: