BREAKING: Silicon Valley Bank. Silvergate 2.0? 🤯; Welcome to the Kraken Bank 🏦; Cash App is preparing for global domination 🌏

FinTech is Eating the World, 9 March

Hey Everyone,

Good morning! This week’s workload is crazy, so apologies for the delay. But it’s absolutely worth the wait as today we’re looking at the Silicon Valley Bank that is breaking (unpacking the situation & is it Silvergate 2.0?), Kraken becoming a bank (what it means?), and Cash App which is preparing for global domination (the global FinTech beast is about to be born + 3 more deep dives you cannot miss). Let’s jump straight into the mindblowing stuff 🌶

BREAKING: Silicon Valley Bank. Silvergate 2.0? 🤯

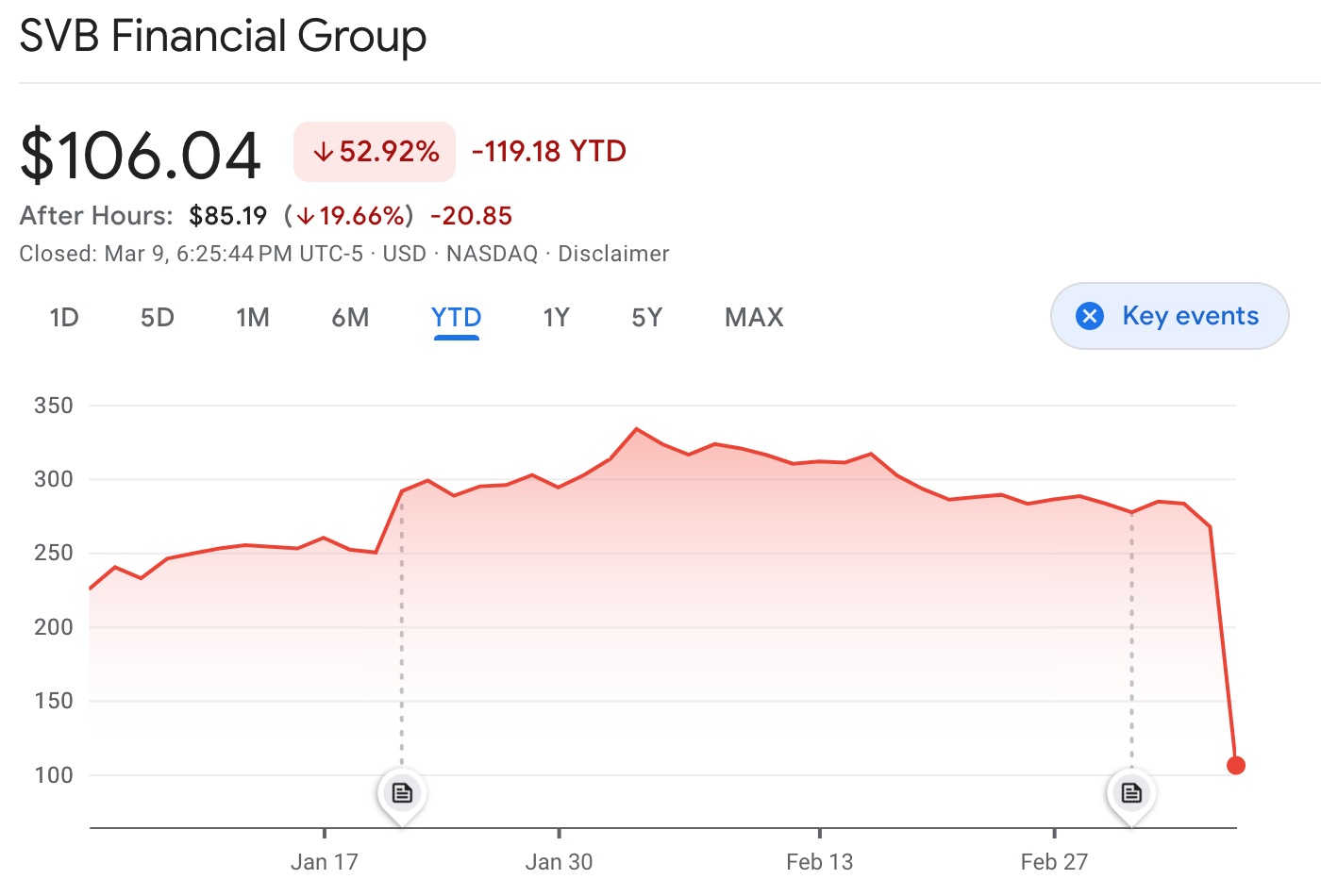

Another one… 😳 Yesterday we had Silvergate, today it’s Silicon Valley Bank (SVB) that’s fighting for survival. Investors dumped shares of SVB SIVB 0.00%↑ and a swath of U.S. banks after the tech-focused lender said it lost nearly $2 billion selling assets following a larger-than-expected decline in deposits.

This is worrisome and could be bigger than Silvergate, so let’s unpack the story.

More on this 👉 Founded in 1983, SVB is on the list of largest banks in the United States, and is the biggest bank in Silicon Valley based on local deposits.

How we got here? 🤔 Here’s a step-by-step breakdown:

SVB is a leading provider of banking and financial services to the technology and life sciences sectors, which are major areas of focus for many VC firms. Those companies raised lots of money from VC in a low-interest-rate environment.

The bank had parked $91 billion of its deposits into long-dated securities such as US Treasuries, which are considered safe but have decreased in value since SVB purchased them because of rising rates. To be more precise, the company's $21 billion bond portfolio had a yield of 1.79% and a duration of 3.6 years. Compare that to today’s 3-year Treasury yield of 4.71%. Ups 😬

As rates went up, the tech market corrected and VC funding (which is a major source of deposits for SVB) dried up.

As the Fed increased rates, the value of the lower-rate bond holdings of SVB went down.

Thus, SVB sold $21.8B of those securities at a $1.8B loss in a bid to reposition the portfolio to maximize yield. To put this into perspective, that’s more than the net income of the entire company in 2021 ($1.5 billion). SVB is now raising capital to cover those losses.

The worst part is that it also has $91B of bonds labeled "held to maturity". The problem here is that, because of accounting rules, SVB does not have to recognize paper losses on those bonds. And this is exactly why the markets are shaking about the extent of those losses and whether SVB can cover their deposits:

If that wouldn’t be enough, most of the board members, investors, founders, etc. started advising everyone to remove all the funds from SVB. If that happens, it would cause a bank run, making everything very ugly very quickly.

Why is this important? 🤔 The collapse of Silvergate was already bad. But this could be much worse. Here’s more on this + the takeaway: