Goldman Sachs wants to end the Apple Card partnership 💳😵; Shopify is building a single-stop FinTech for merchants 🛍; Meta's Threads raises questions for banks and credit unions 🏦

FinTech is Eating the World, 28 July

Hey Everyone,

TGIF! What a week it was… 🤯 And it’s not over as today we’re looking at Goldman Sachs which wants to exit the Apple Card partnership (a deeper dive into the deal, why it matters & what’s next + some solid bonus reads), Shopify which is building a single-stop FinTech for merchants (it’s a FinTech beast you cannot ignore!), and Meta's Threads that raises questions for banks and credit unions (how others are leveraging it & what you should know). Let’s jump straight into spicy stuff 🌶

Goldman Sachs wants to end the Apple Card partnership 💳😵

The HOT news🔥 As Goldman Sachs GS 0.00%↑ looks to end its credit card partnership with Apple AAPL 0.00%↑, an interesting tidbit has recently come to light - the bank's own underwriting system initially rejected Tim Cook's card application. Ouch 🥶

But let’s take a holistic look at this and see why it matters.

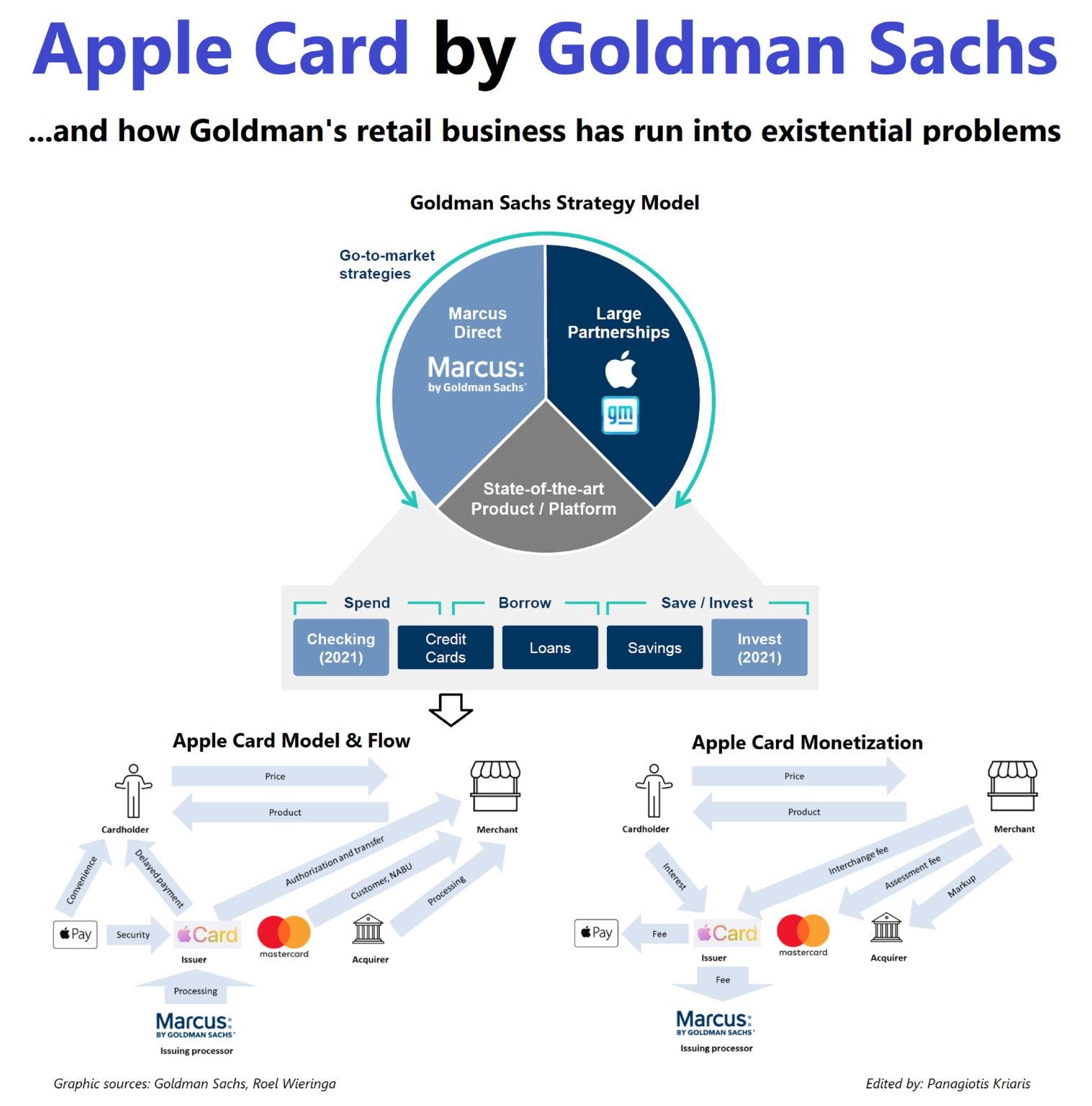

More on this 👉 Goldman Sachs traditionally serves large institutions and high-net-worth individuals. But it entered the retail banking industry with much fanfare in 2016 when the bank introduced Marcus, a digital-only bank designed for everyday consumers, and began offering personal loans to users. The service had attracted over $50 billion in consumer deposits by the time the bank struck its deal with Apple.

Goldman has been Apple's credit card partner since the card's launch in 2019 and has expanded its collaboration to include other banking services for the tech giant (i.t. it’s also powering Apple’s consumer saving account, which was unveiled in April). However, GS has been shifting away from the consumer market, spinning off its digital bank Marcus and creating a new unit that includes the Apple business alongside other operations.

ICYMI: Goldman Sachs' Marcus shows just how difficult FinTech really is 😔

The new unit reported substantial losses in recent years, prompting Goldman's interest in cutting ties with Apple and potentially passing the business to American Express AXP 0.00%↑. However, potential deals with AmEx or other partners like JPMorgan Chase JPM 0.00%↑ might prove challenging, as they are not keen on co-branded cards or taking a secondary branding role.

Apple Finance 🍏🚀 With that in mind, Apple will probably continue moving deeper into financial services directly and may consider bringing much of Goldman's contribution in-house, handling underwriting, fraud prevention, and customer service on its own while potentially working with a less prominent lender for regulatory purposes.

Side note: acquiring GS consumer division or Goldman altogether might be an even bigger thing long term… 👀

ICYMI: The deal Apple needs to make: acquiring Goldman Sachs' Consumer Division would be the M&A of the century 🤯

Anyways, any transition away from Goldman could take up to 18 months to complete, according to reports.

You can’t make this up… 😬 Interestingly, before the Apple Card launch, even Apple's CEO Tim Cook faced a hurdle in getting approved for the card. Goldman's underwriting system rejected his application, not due to his creditworthiness, but because he was a high-profile target for potential fraud. However, the bank eventually made an exception to issue Cook a card. Phew 😮💨

✈️ THE TAKEAWAY

Looking ahead 👀 It’s quite prophetic that one of the most high-profile alliances between a tech and finance company began inauspiciously. But I guess you have to learn the hard way that FinTech is hard, and getting into lending (& doing it profitably) as a new entrant in the market is nearly mission impossible. Given that Goldman is going to have one hell of a hard time getting AmEx (not to mention JPM) to take Apple off its hands, it’s going to be super interesting to follow where this ends. But one thing is clear - Apple won’t be the one that loses here. It rarely does.

Worth reread: Apple might become the First Super App of the West 🍎 [+4 more reads]