Robinhood is one of the cheapest FinTechs right now 😯; PayPal is just too good to ignore right now 🤑

FinTech is Eating the World, 21 August

Hey Everyone,

Happy new week! Slightly behind schedule, we’re coming back with another special issue as today we’re looking at two ridiculously undervalued FinTech goliaths. Robinhood, which is probably the cheapest financial technology company out there (a closer look at their numbers + what everyone’s missing & lots of bonus reads), and PayPal that’s just too good to ignore right now (numbers back it up as a brilliant long-term investment + a deep dive into PayPal). Let’s jump straight into the fascinating stuff 🌶

Robinhood is one of the cheapest FinTechs right now 😯

The news 🗞️ Last week was pretty intense for all things FinTech, so it’s not surprising that some things were missed or left out. And one of the things that’s definitely worth talking about today is Robinhood HOOD 0.00%↑.

The retail trading giant just reported its latest monthly data, which together with its recent quarterly earnings, indicate that it’s currently one of the cheapest public FinTech stocks out there.

Let’s take a closer look and see why it’s worth your time and money.

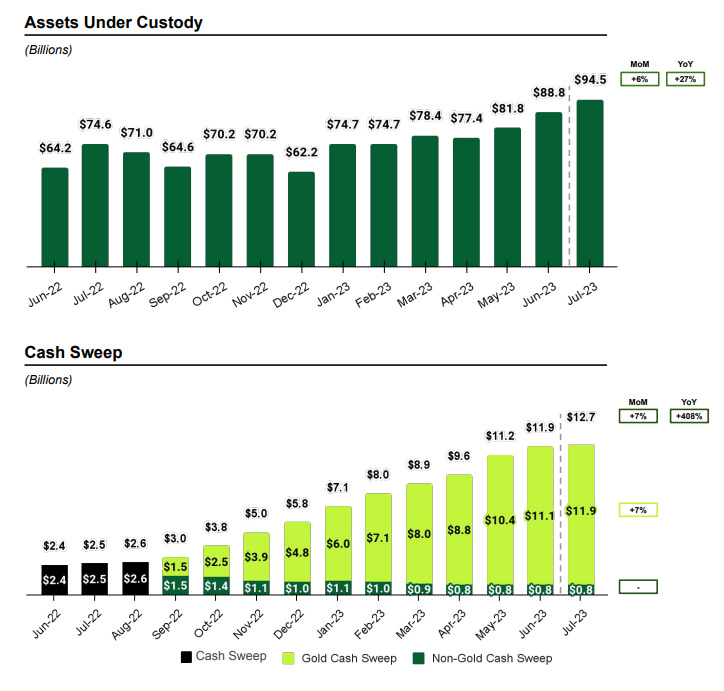

More on this 👉 Here are the key takeaways from Robinhood’s latest monthly data:

Net Cumulative Funded Accounts (NCFA) at the end of July were 23.2M, up approximately 50k from June 2023.

Monthly Active Users (MAU) increased to 11.0M in July, up approximately 200k from June 2023.

Assets Under Custody (AUC) at the end of July were $94.5B, up 6% from June 2023.

Net Deposits were $1.4B in July, translating to a 19% annualized growth rate relative to June 2023 AUC. Over the last twelve months, Net Deposits were $16.8B, translating to an annual growth rate of 23% relative to July 2022 AUC.

Trading Volumes in July were higher for equities and crypto and lower for options compared to June 2023. Equity Notional Trading Volumes were $69.2B (up 3%). Options Contracts Traded were 106.1M (down 4%). Crypto Notional Trading Volumes were $3.4B (up 3%).

Cash Sweep Balances (your uninvested cash that’s FDIC insured and pays 1.5% Annual Percentage Yield (APY) for regular users or 4.9% for Robinhood Gold members) at the end of July were $12.7B, up $0.8B (7%) from the end of June 2023.

Out of the above, Assets under Custody is probably the most important metric, and Robinhood will soon surpass $100B in AUC. On top of that, it got $800M on Net Deposits directly into Cash Sweep in July alone. Solid.

Now let’s take a look at the key takeaways from Robinhood's Q2 2023 earnings results:

Total net revenues were $486M, up 10% sequentially driven by higher net interest and seasonally higher other revenues. This was a 53% increase compared to Q2 2022.

Net income was $25M compared to a net loss of $295M in Q2 2022. Robinhood achieved GAAP profitability for the first time as a public company.

Adjusted EBITDA was $151M, up 31% sequentially. This is a significant improvement from the ($80) million Adjusted EBITDA loss in Q2 2022.

Average Revenue Per User (ARPU) increased to $84, up 9% sequentially. We’re clearly on the path to 2021 numbers…

✈️ THE TAKEAWAY

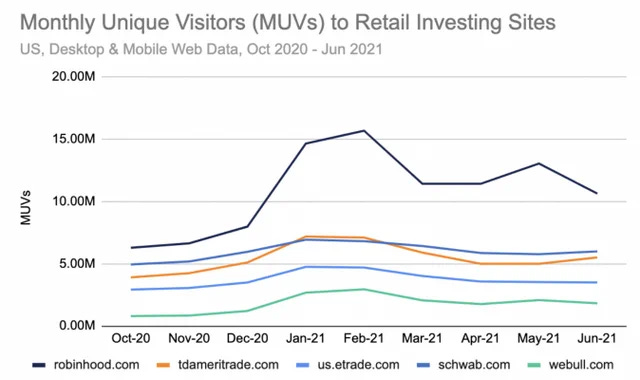

Why should you care? 🤔 First and foremost, Robinhood just turned GAAP profitable and has an enterprise value of near zero. To put it another way, HOOD 0.00%↑ at $10 (Robinhood’s current stock price) means $9 billion for the following: $3B for the trading platform & 11M users + $6B of cash. If that doesn’t look like a bargain to you, we must remember that E-Trade was bought for $13B by Morgan Stanley MS 0.00%↑ while TD Ameritrade was bought for $26B by Charles Schwab SCHW 0.00%↑. Sure, some valuations were inflated, but when it comes to users, Robinhood is dominating the space (the data below is not recent but gives a good sense of where things stand):

The above coupled with the strong net revenue growth, improved profitability, and lower expenses are positive signs for Robinhood's business fundamentals and make them outrageously cheap. If you don’t hold any of their stock, now might be one of the best times to reconsider your position.

ICYMI: Robinhood goes UK🇬🇧: Part III 👀 [international expansion is a massive room for growth + lots of bonus reads]

Disclaimer: this isn’t investment advice and I’m a shareholder of Robinhood.