Welcome to the Google Bank - Your Everyday Banking from Google, NOT a Bank

Google Bank is coming to a phone near you

Google is the latest tech company trying to get a stronger footprint into financial services. The project codenamed Cache was initially disclosed in December 2019. Then the Alphabet subsidiary was expecting to launch a checking account sometime next year. The accounts will reportedly be managed by Citibank, and a small credit union at Stanford University. According to Google, Citibank will handle the financial plumbing. In this regard, is sounds very much like Apple, which claimed its new card — which is backed by Goldman Sachs — was created by a tech company and not a bank.

Fast-forward to August 2020, Google is getting further into mobile banking through a new partnership with a total of eight US-based banks, including the US division of the Bank of Montreal (BMO) and BBVA. The bank accounts will exist entirely within Google Pay, with customers able to access checking accounts handled digitally on the front end by Google while partner banks handle the infrastructure, FDIC insurance, and other backend technology.

It’s remains unclear if customers will have access to physical debit cards issued through Google or its partners, but the banking feature is expected to go live sometime in 2021.

You may ask why the hell tech giant like Google is interested in Finance?

Well, it is pretty simple – there is a lot to gain for Google. Checking accounts can provide valuable insight into consumers’ day-to-day financial lives, including their income, where they shop, and how much and where they spend. Google will not sell users' financial data, according to Google executives. Of course, Google does not sell data at all - it simply uses it to target advertisements. Though, Google executives pointed out it does not use data from its mobile wallet Google Pay for advertising purposes. I wouldn’t be that certain…

Earlier Attempts into Finance

Google has made forays into financial services in the past, with mixed results: it launched Google Wallet in 2011 but shut down the associated Google Wallet card in 2016 (and has been rolling Google Wallet into Google Pay). It also ran a site to compare financial products like auto insurance and credit cards between 2015 and 2016 but shuttered it after about a year.

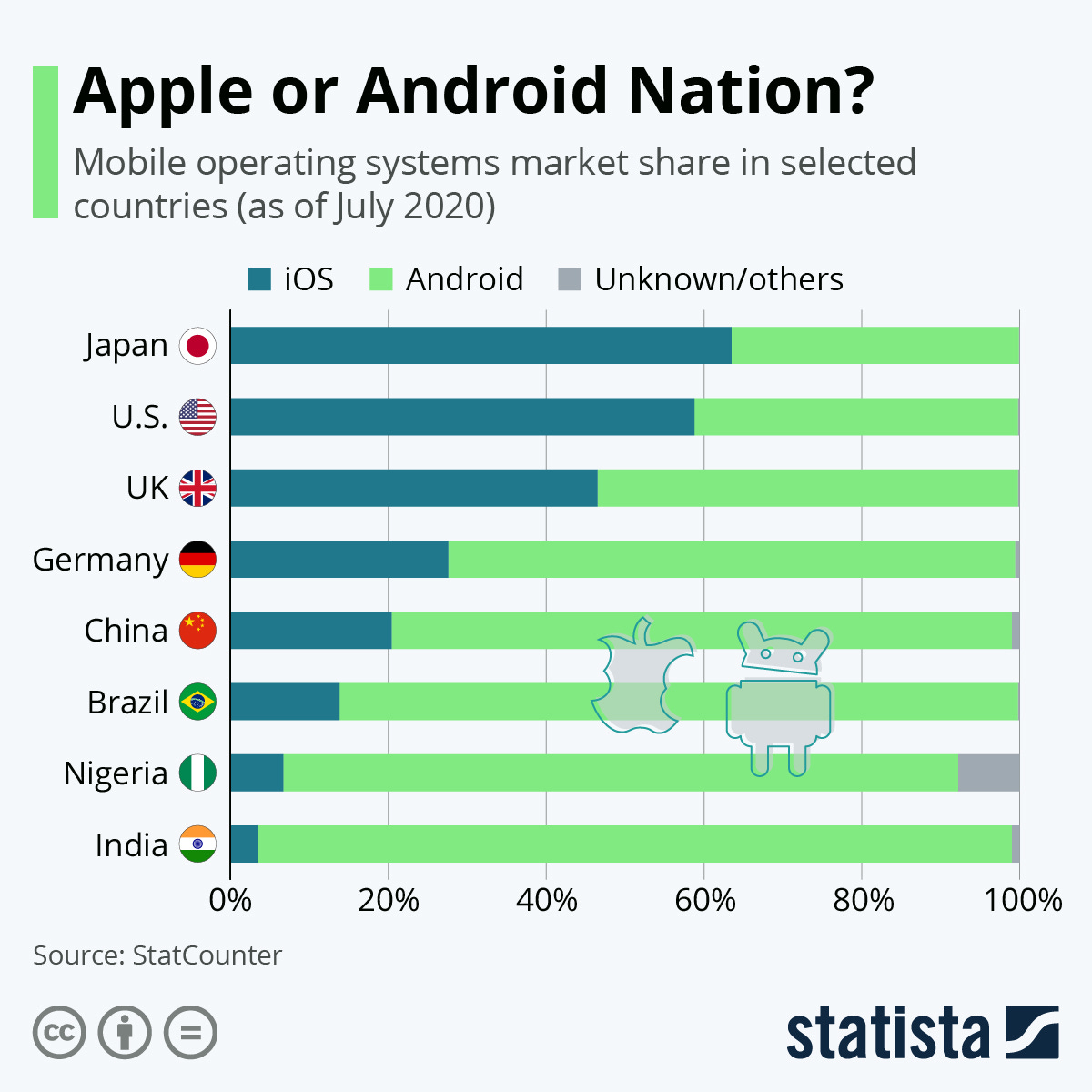

To launch a successful checking account, Google will need to incorporate features that stand out and encourage direct deposits. While Google has a sizeable enough addressable base — 40%+ of smartphones in the US run on Android, according to Statista — and some consumers would probably be interested in a Google checking account, the mixed results of its past financial services plays suggests that an if you build it they will come approach won't be enough.

From a global perspective though, Android is dominating, especially in emerging markets like India, Nigeria or Brazil.

Obviously, a deeper relationship for Google with people's finances provides several opportunities for the company, and it could help it compete with Amazon and Facebook, both of which have increasing insights into how consumers are spending their money.

Getting into Your wallets

One of the biggest advantages Amazon has over Google and Facebook is its direct access to its users' shopping history. It extends that data mining with its credit card and by incentivising Prime members to scan an app at Whole Foods. All that data allows Amazon to surface relevant product recommendations, craft promotional offers, and tailor services to get customers to spend more on its website. Amazon also has concrete measurement data to show advertisers, which is a key differentiator between it and Google or Facebook.

Facebook recently updated its payments service with a focus on increasing commerce across its various platforms. It explicitly said it will be using data for its advertising business.

Google might not be as aggressive with the data it collects from consumers' new checking accounts. They plan to use access to people's wallets to bring value to consumers, banks, and merchants, with services that could include loyalty programs.

There is a lot to gain for Google. Checking accounts can provide valuable insight into consumers’ day-to-day financial lives, including their income, where they shop, and how much and where they spend.

In this regard, it could look similar to Square's Boost cash-back program, something that's starting to become an advertising product instead of a customer acquisition tool. While Google might not use data from its checking product to target advertisements, it might use the data from users' other online activity with Google to target offers in the planned checking account. It could use consumers' spending behavior to measure effectiveness for merchants.

Google won't use data for online advertising. Really?

The company’s word choice is key when they said the company won't "sell" users' financial data. We all know that pretty much every bank uses its consumer data for marketing. That may be something like sending targeted credit card offers or other financial services like life insurance.

Google is more than capable of emulating that kind of marketing and bringing it into the digital age. It has nine products with over a billion users, which means you probably interact with at least one Google product on a regular basis -- perhaps daily. And customers signing up for a Google checking account product are much more likely to be fans of Google's other products. Having this in mind, Google has a lot of access to its users to make the marketing efforts seen from traditional banks more effective.

While consumer financial data might not feed into the ads users see in Search or on YouTube, it would not make sense for Google to invest in developing a new product without plans to leverage some of its biggest assets with its core competency: digital advertising.

Facebook is upfront about how it uses payment data. Amazon is not trying to hide the fact that it collects and uses your shopping data, either. Google should not be any different.

The Bottom Line

One thing is clear - it is all about more data, which effectively leads to more ads and more revenue. Yet, we also must understand that consumers these days practically expect tech companies to harvest their data anyway. Even so, some 58% of respondents in a recent survey from McKinsey & Co. said they would trust financial products from Google. That's better than Facebook (31%), but not quite as good as Amazon (64%). Google would be doing itself and investors a disservice if it did not use data from its banking product for advertisements.

Further, if we assume that Cache does take off, it could mean a windfall for Citibank (and other financial partners that would join). A Google checking account sounds like something that’d appeal to a younger generation, meaning the bank would be more likely to connect to new customers. Banks have a tendency to retain customers for a very long time: JD Power’s 2019 Banking Satisfaction Study showed only 4 percent of consumers switched banks last year, and a 2017 survey by Bankrate shows that the average American adult keeps the same checking account for around 16 years.

So maybe digital challengers like Monzo, Revolut, N26 and others that primarily serve the younger generation should be worried here instead? Google has scale, profitability, and technological powers that could potentially put neobanks' future prospects in jeopardy. Especially taking into account their massive cash burn and questionable profitability prospects.

Only time will show the answer. Either way - watch out, Google is coming to a phone near you.

Note: this article has been initially published on LinkedIn in December 2019. Due to the relevance and importance, it has been updated and published for my Substack community too.

***

About: I am a business developer, sales professional, FinTech strategist, as well as Cryptocurrency and Blockchain enthusiast. I'm highly passionate about Financial Technology and Digital Innovation, and strongly believe that it will change the world for the better. Apart from my daily job at a global payments startup where I'm leading company's expansion into Europe , I'm an active member of FinTech community and a TechFin evangelist.

If you've enjoyed this piece, don't hesitate to press like, comment what you think and share the article with others. Let's spread the knowledge together!

For more, you can check me on LinkedIn & Twitter where I’m sharing my thoughts and insights daily!🔥🚀