LatAm’s new FinTech gem is now worth $4.8B 💎; Facebook says 'Carpe Diem' for the last time💀; Apple to turn iPhones into payment terminals 🤯

You're missing out... Weekly Recap 🔁

Good morning Everyone,

And happy Saturday! This week was crazy hot… In fact, it’s probably the hottest week in FinTech this year so far! 🤯 Hence, I invite you to take a look at the three stories that were moving the headlines this week in the financial technology world. You can uncover other stories, keep the FinTech pulse daily and get at least X5 more by becoming a subscriber. Join the community here:

And here’s a mix of 3 hot & fresh FinTech stories from this week:

LatAm’s new FinTech gem is now worth $4.8B 💎

The funding 💸 Brazilian secured lending platform Creditas has hit a whopping $4.8 billion valuation off the back of a $260M Series F funding round.

Fidelity Management and Research Company, Actyus, and Greentrail Capital joined the round, alongside existing shareholders QED Investors, VEF, SoftBank Vision Fund 1, among others.

The newest funding grew Creditas’ valuation almost 3 times - it’s now up from the FinTech’s $1.75B valuation at the time of its $255M raise in December 2020 🤯

The USP 🥊 Founded in 2012, Creditas is a digital-first secured lending platform, with a mission of reducing the Brazilian consumer debt burden by offering consumer loans at more affordable rates by using borrower collateral like homes, autos, and payroll.

The numbers 📊 In the third quarter of 2021, Creditas notched $46.8M in revenue – up 233% from $14M in the 2020 third quarter. That’s solid!

At the same time, as it has been investing in its growth, the company’s net loss widened to $14.8M compared to $8.25M. Founder and CEO Sergio Furio projects annualized revenue of about $200M for 2021.

Creditas is LatAm’s newest FinTech gem that’s definitely worth keeping a close eye on. Here’s why👇🏼

✈️ THE TAKEAWAY

Crazy growth & platform focus. First and foremost, it must be noted that although Creditas is already 10 years old, their growth is impressive, to say the least. In fact, such rapid revenue growth is more often seen in younger startups rather than a decade-old firm. Second, Creditas is among very few FinTechs globally that gives a glimpse into its finances. This kind of transparency is not common, yet very refreshing, and definitely has the benefit of preparing the company well for its eventual path to the public markets (which is being monitored closely according to their CEO). Finally, looking at the bigger picture, one of the most interesting things about Creditas is their platform focus. Or in their own words, Creditas is working toward being “a one-stop solution for those seeking a digital-first experience in everything related to their house, car, motorcycles, and salary-based benefits.” Think of them like a Financing Super App. If we can take Nubank’s triumph as a proxy here, Creditas might be another FinTech success story in the making.

Facebook says Carpe Diem for the last time 💀

The news 👀 Mark Zuckerberg is seeing the demise of his cryptocurrency project Diem due to regulatory pressures, Bloomberg reported.

The Diem Association, which used to be known as Libra and which is backed by Meta, is looking at selling its assets as a way to potentially return capital to investor members.

The history 👉 Meta’s Facebook debuted the idea for a stable digital currency in 2019, purporting that it could deliver big changes for global finance. The company collaborated with dozens of others at the time. However, the partnerships weren’t enough to protect it all from a huge amount of scrutiny — Zuckerberg was called to testify before Congress, and then several partners (i.e. Stripe, PayPal, Visa, Mastercard, among others) dropped out of the project.

The big pushback 🥊 Politicians and central banks wasted little time from Day 1 in declaring that Libra had the potential to undermine the U.S. dollar and trigger financial stability — with some even claiming that this digital asset could do more harm to America than 9/11. Others argued that the tech giant was unfit to operate a private currency following a string of controversies.

The project then changed its name to Diem from Libra after Zuckerberg’s testimony. But it provided little help.

What’s happening now 🤔 Now, according to Bloomberg, Diem is speaking with investment bankers on strategies to sell off its intellectual property. It will also seek to find new homes for the engineers who developed the tech, cashing out any other value remaining in the venture.

In retrospect, it was inevitable.

✈️ THE TAKEAWAY

Mission: Impossible from Day 1. Although Facebook’s intentions were clear from day one (in essence, to dominate the world of finance like it now does with social media), it was somewhat expected that the regulators, both US & worldwide, would hardly allow it. Especially for a company that has been facing lots of controversies lately. Regardless of the potential scale and impact (including positive one), it was more of a David versus Goliath than anything else. It became clear that Diem’s ambitions might not materialize when David Marcus, an executive who had played an instrumental role in creating and leading the project, announced he was leaving Novi. As Elon Musk once put it, In retrospect, it was inevitable.

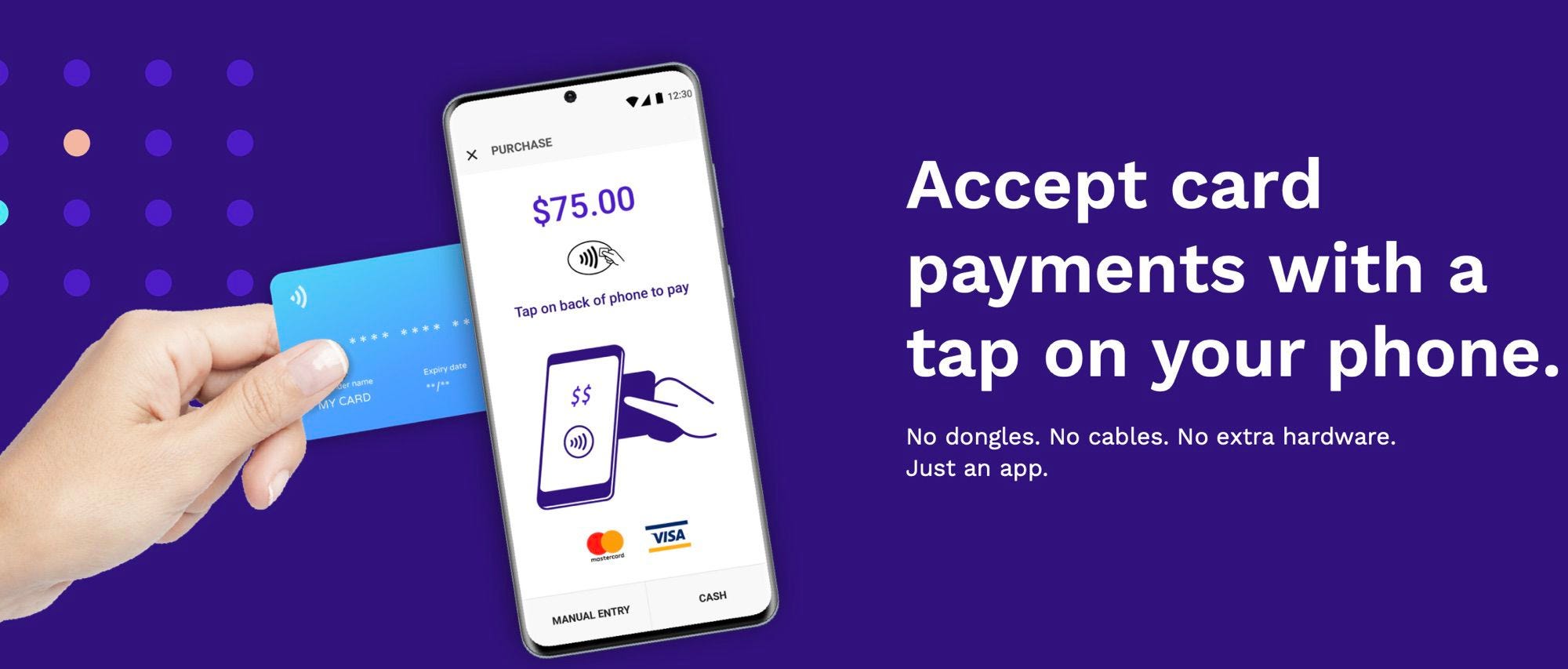

Apple to turn iPhones into payment terminals 🤯

The news 👀 Tech giant Apple is reportedly working on an update that will transform its iPhone into a payment terminal, enabling users to accept payments with the tap of a card.

The PFWTM 👉 Citing people with knowledge of the matter, Bloomberg says the company has been working on the new feature since around 2020 when it paid $100M for Canadian startup Mobeewave.

New rivalry ⚔️ The feature is likely to provide a setback to Square, PayPal’s iZettle, and the new breed of SoftPOS vendors, by providing the tap-and-pay functionality as an integrated part of the device, with no need for third party help.

Apple may begin rolling out the feature via a software update in the coming months, say Bloomberg sources. The company is expected to release the first beta version of iOS 15.4 in the near future, which is likely to see a final release for consumers as early as spring.

✈️ THE TAKEAWAY

POSless payments. While it’s still not clear as to how Apple will roll this out, the news is huge for a couple of reasons. First and foremost, Apple’s move could definitely shake up the market for payments providers like Block’s Square, or SumUp which dominate the space in different countries/regions. Of course, it all depends on how the iPhone maker proceeds with merchants and the use of its system by other apps. On the other hand, Square/SumUp and others, for example, could continue accepting payments using Apple devices without the need for its own hardware. If Apple makes it mandatory for retailers to use Apple pay or its own payment processing system, however, it then would directly rival the current mPOS providers. Zooming out, it looks like POSless payments are probably the future, and Apple could be one of the firms perfectly positioned to dominate it.

🔎 What else I’m watching

Fed’s Digital Dollar Report 👉 The Federal Reserve has finally dropped its long-awaited central bank digital currency report and it is careful, raising more questions than giving answers. The report, Money and Payments: The U.S. Dollar in the Age of Digital Transformation, does give a window into the U.S. central bank’s thinking on the subject. Most notably, the Fed’s thinking is to make very, very clear that it is in no way advocating for or against the creation of a digital dollar. It is, the third sentence in the report states, “the first step in a public discussion.” Read the report here.

Plaid pays 👀 Plaid, which connects consumer bank accounts to services like Venmo, Robinhood, Coinbase, and other apps, has been accused of collecting excessive financial data from consumers. While denying any wrongdoing, it agreed to pay $58M to all consumers with a linked bank account to any of its approximately 5,000 client apps. The lawsuit accused Plaid of collecting more financial data than was needed from users. It also claimed that the company obtained users’ bank login information via its own ‘Plaid Link’ interface. On top of the $58M payouts, the company was forced to change some of its business practices. Earlier in January 2022, Plaid has splashed out around $250M on ID verification company Cognito.

YouTube considers NFTs 👉 According to YouTube CEO Susan Wojcicki, the online video giant could be looking at blockchain technologies as a way for its creators to make money. Precisely how NFTs will work for the platform is not clear, but what is plain at this juncture is that nearly every major digital brand is going to at least try NFTs out in case they work for their users.

💸 Following the Money

Sequoia Capital India has made its investment debut in the Arab Gulf by leading a $33M Series A funding round for Lean Technologies. In addition to Sequoia and existing investors, General Electric Co.’s former chief Jeff Immelt participated in the financing round.

UAE-based financial infrastructure company M2P Solutions has announced a $56M Series C1 funding round to further build its technology while expanding internationally.

Cross-chain bridge Switch, previously known as Polkaswitch, raised $6M to continue building its protocol that enables crypto users to bridge between a number of L1 and L2 blockchains, including Ethereum, Polygon, Avalanche, Binance Smart Chain, Arbitrum, and Moonriver.

👋 That’s it for today! Thank you for reading and have a productive weekend! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

P.S. This is a free and short issue that might not be published every week. Subscribe now and keep the FinTech pulse daily, make sense of what’s happening in the financial technology space every day and stay ahead. You will save at least 180 minutes. Every week!