Results from Shopify, Visa/MC, Amazon, etc., indicate the Great Normalisation & digital cooldown 📉; Block’s strong Q1 & Cash App’s huge growth potential 🚀; BNPL turns to BNPN (Buy Now, Pay Now) 👀

You're missing out... Weekly Recap 🔁

👋 Hey, Linas here! Welcome to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

What if Bitcoin isn’t a hedge at all? One metric you need to watch 📉

Major roadblock for Revolut’s "Global Super App" ambitions 👀

Google’s new feature that just killed a 100 FinTechs 🤯

and more!

As for today, here are the 3 FinTech stories that were moving headlines this week. It was one of the hottest weeks this year!

Results from Shopify, Visa/MasterCard, Amazon, among others, indicate the Great Normalisation & digital cooldown 📉

Trend spotting 🔍 I’ve earlier covered Meta, Visa/Mastercard, among others. Given that we now have the latest results from Shopify (which is also a FinTech), Amazon, etc., we can see some very clear trends emerging. And they might not be very good…

More on this 👉 In the past two (pandemic) years, nearly 1/5 of every dollar spent in the US came from online orders. It seems that now consumers are returning to their 2019 spending habits and the boom in e-buying is losing momentum. As an effect:

E-commerce & FinTech giant Shopify’s sales rose 22%, to $1.2B. But that was a fraction of its 110% gain from the same quarter last year. Hence, shares of $SHOP sank 15% after the popular e-commerce platform saw sales slow for the fourth straight quarter. That’s already a trend.

If blaming inflation, labor shortages, and a return to real-life shopping wasn’t enough, Shopify execs said the rest of the year doesn’t look much better. The trend continues.

Amazon joined the stage too, reporting a 3% drop in online sales in the first three months of 2022, and forecasting a meager 3% sales growth for the current quarter. Its shares plunged for their biggest one-day drop since 2006. Ouch!

Amazon’s results were basically a warning sign that shoppers are logging off as virtually every major online retailer’s earnings since then have shown continuous signals of a clicking cooldown.

For example, both Etsy and eBay lowered their sales forecasts for the year and didn't say when (or if) they’d return to pandemic-era profits.

As a cherry on top 🍒, we can look at the latest results (and data) from both Visa & Mastercard. In short, it shows that people aren’t spending less — they’re spending differently. The money is now hence moving from digital and e-commerce to the real world - into restaurants, travels, and delayed vacations.

When you zoom out, it’s clear that we’re already seeing the Great Normalisation and that e-buying is losing momentum. This means that some of the biggest pandemic winners (including FinTehs) will inevitably experience a cooldown. Here’s the takeaway:

✈️ THE TAKEAWAY

Welcome to the Great Normalisation. First, let’s zoom out again - US e-commerce sales have dropped 3X compared to 2020 levels. That’s huge and it’s a very clear indication that some of the biggest pandemic winners will hit a cooldown mode. Not only in the US - but globally. Pandemic-fuelled boredom and work-from-home gave a huge boost to everyone in e-commerce (from platforms/marketplaces to payment processors and other FinTechs). As COVID-19 is fading, consumers are shifting their spending as they eagerly want to experience real life back again. This effectively means that companies like Shopify/Amazon/eBay, or online-only processors/BNPL players need to adjust expectations for the new new normal of more balanced spending. Also, it’s yet another proof of the importance of revenue diversification and the power of an omnichannel strategy in retail. Finally, it’s too early to say how far away are we from the real cooldown aka recession as consumers are still opening their wallets — they just have new priorities now. But you cannot and must not ignore this.

Block’s strong Q1 & Cash App’s massive growth potential 🚀

Earnings call ☎️ FinTech heavyweight Block, which is led by Twitter co-founder Jack Dorsey, reported rather strong results with first-quarter operating profit that topped Wall Street targets.

Block's shares rose 10% in extended trading even though the company, formerly known as Square, reported a lower-than-anticipated adjusted profit.

Key numbers 📊 Here’s what you need to know from Block’s 1Q2022:

Block’s gross payment volume (GPV) surged 31% year over year (YoY) in Q1, hitting $43.5B.

Monthly active users averaged 21 transactions across Block’s ecosystems, and March had the strongest monthly Cash App engagement. Increased adoption of the Cash App card and direct deposits fueled growth for the peer-to-peer (P2P) payments app.

Monthly active Cash App users sent more than 350,000 leads to Afterpay sellers in Q1 as the $29B M&A starts paying dividends.

Block also started letting Cash App users send and receive Bitcoin to compatible external wallets via the Lightning Network. BTC is one of the core elements of the Block ecosystem.

So what’s next? Despite the fact that the Block is severely undervalued right now, Cash App is where our eyes should be as it has massive growth potential. Here’s the takeaway:

✈️ THE TAKEAWAY

Undervalued $SQ & huge Cash. Despite good results, Block has dropped around 20% in the last 5 days alone, and almost 50% year-to-date. That’s brutal. Growing recession fears, an uncertain geopolitical environment, and plunging Bitcoin (and Block makes a significant amount of money from customers using Cash App to buy & sell BTC) all have contributed to the $SQ selloff. But this isn’t something that worries me too much. For now. First and foremost, we should look at Cash App, and Block’s core app has a lot of growth potential. Stronger social components is one of them. As noted by the company’s executives, the firm was already experimenting with integrations like a search function that lets Cash App users discover BNPL offers and Afterpay merchants. Moreover, Cash App could introduce a Venmo-like payment feed that should further drive engagement and usage of the app. Next, we should mention the global expansion, which is probably the biggest untapped resource for Block. The firm already lets Cash App users send money between the UK and US, but it could easily expand the service to other markets, like Spain given its acquisition of the Spanish P2P payment app Verse. If we zoom out and look at Block again, two other important revenue drivers appear. First, airlines and online travel companies suggest strong demand heading into the summer, thus positioning Block to benefit as consumers prepare to spend money away from home on areas like retail and restaurants. Second, Block’s Cash App now housing Credit Karma’s former tax-preparation business allows Block to capitalize on a potential surge of tax refunds coming into the Cash App, which consumers would then have the chance to spend or invest. All in all, Block still has a lot of room for growth and $SQ looks like a very undervalued stock.

BNPL turns to BNPN (Buy Now, Pay Now) 👀

Spotting the trends 📉 Buy Now, Pay Later aka BNPL was one of the hottest verticals in FinTech. But the tides might be shifting. Afterpay, Klarna, Affirm, and other BNPL players that were thriving recently might need to regroup very soon.

More on this 👉 Let’s look at the data that’s merging into a worrisome trend:

San Francisco-based Affirm is one of the biggest BNPL companies, which allows shoppers to obtain unsecured instalment loans when they buy clothes, electronics, and other goods online. Despite its luck with Peloton and signing both Amazon & Walmart as partners, Affirm’s market cap has fallen to less than $5B (= a decline of more than 80% from a high last November). Quarterly results due on Thursday are expected to show a net loss of $156M on $345M of revenue, according to a Bloomberg poll of analysts. That’s not good…

Further, shares of FinTech Upstart tanked 56% yesterday alone, despite the company's better-than-expected earnings (revenue more than doubled and profit rose 3X). The AI-driven platform connects people with less-than-stellar credit scores to lenders with favorable terms. If that wasn’t enough, Upstart cut its revenue forecast for the year and predicts lower sales and zero profit for this quarter. Ouch.

Ok, this is US-only maybe, so too early to worry, right? Unfortunately… BNPL stocks have come under heavy selling pressure in Australia too. Shares in Zip Co, Australia’s largest BNPL provider, have dropped 72% this year as shareholders balk at the prospect of rising bad debts.

On top of that, BNPL player BizPay has laid off 30% of its workforce, saying tough market conditions for tech companies have forced it to streamline its operations.

While others aren’t taking such harsh measures just yet, they have clearly put a stop to hiring. For instance, hiring at Afterpay (that got acquired by Square aka Block for $29B) fell significantly in early February of this year and is nearly at year-to-date lows:

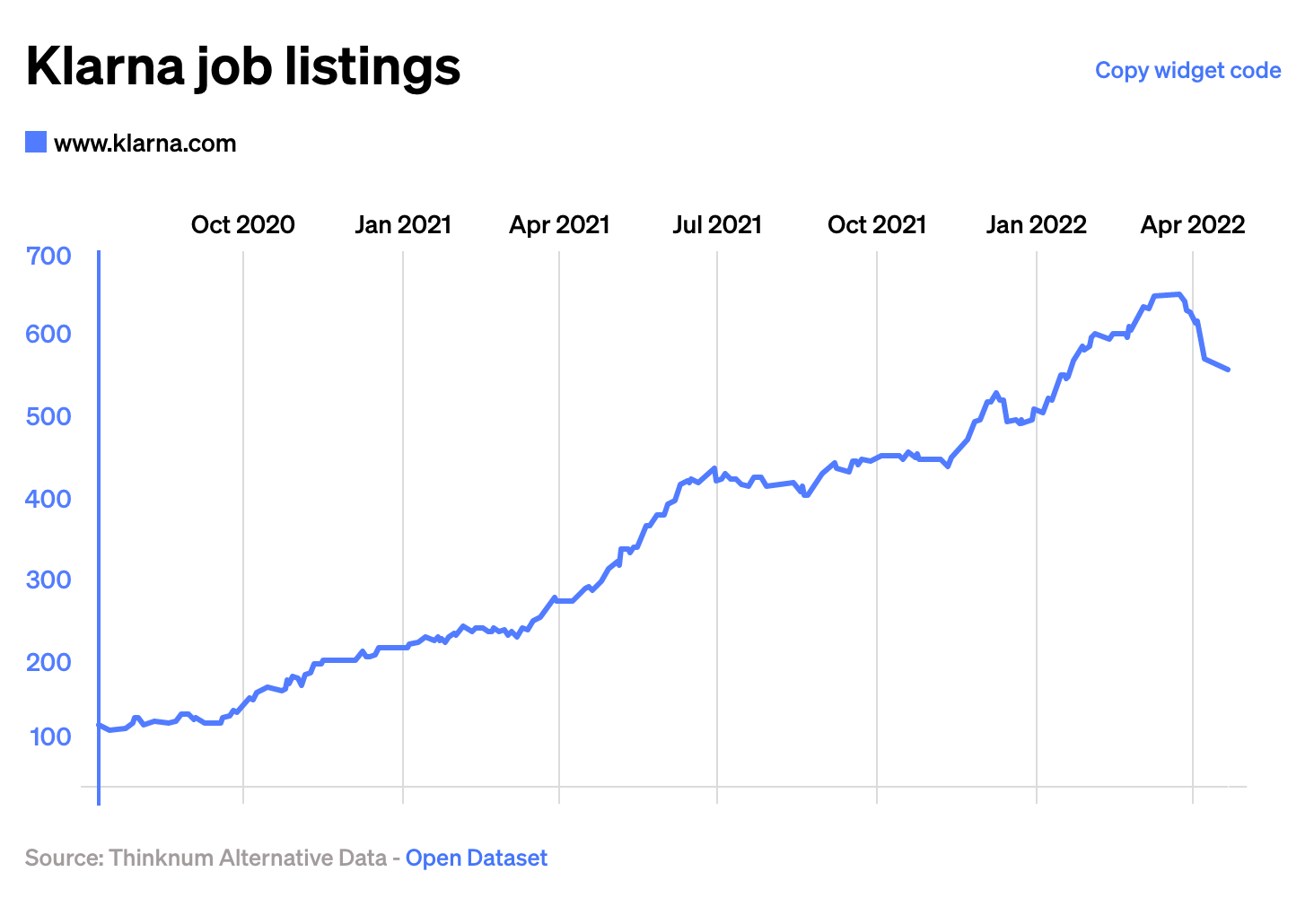

Hiring growth Klarna, one of the most valuable private FinTechs in the world and some of the most prominent BNPL players, has also started falling since March 24 after steady going up since July 10, 2020:

So what does this tell us? There’s clearly a shift happening in the market as we speak and Buy Now Pay, Later is transitioning to Buy Now, Pay Now. Here’s the takeaway:

✈️ THE TAKEAWAY

Inverse relationship. In short, the reality is this - BNPL doesn’t sound as good as it used to. At the core, the days of near-zero interest rates are gone, and hence it's hurting loan providers — from BNPL firms to alternative lenders (Upstart). Rising rates globally make loans more expensive so consumers might start taking out fewer loans. Hence, the BNPL sector is being repriced to reflect that, and debt-laden Gen Zers are starting to turn against the services whose growth they fueled (ironic, isn’t it?). When you zoom out, it’s an almost perfect inverse relationship - when interest rates are down, BNPL demand grows, but when the rates rise - BNPL is losing. The worst part? Interest rates are only starting to climb…

🔎 What else I’m watching

CBDC interest is 🚀 Nine out of 10 central banks around the world are exploring central bank digital currencies (CBDC), according to a survey conducted by the “central bank of central banks” Bank for International Settlements (BIS). More than half of those banks are developing or testing a retail CBDC, a digital currency designed to be used by consumers.

Marqeta earnings 📈 Consumers have continued to spend using cards. Buy now, pay later (BNPL) has become less a novelty than a firmly entrenched payment method. Those trends continued to be in evidence in Marqeta’s most recent earnings results, where spending via Block (formerly Square) helped boost several key metrics. In the latest supplemental filings that accompanied earnings, the company said that quarterly total processing volumes were up 53% to $37B. That’s higher than forecasts in the most recent quarterly commentary, which had estimated that TPV would grow by 40% through the rest of the year. Jason Gardner, the CEO, said that the 53% growth rate in TPV was notable given the fact that the prior period had been boosted by government stimulus payments.

💸 Following the Money

NFT startup Zora has raised $50M in funding led by Haun Ventures.

French blockchain gaming platform Cometh has raised $10M.

Buy now, pay later (BNPL) startup Walnut closed a $110M Series A led by Gradient Ventures.

👋 That’s it for today! Thank you for reading and have a relaxing weekend! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

I really especially enjoy when you highlight VC trends in FinTech and blockchain. If you did a deep dive on a16z that would be amazing!