BNPL is dead, long live (B2B) BNPL!? 🤔; Affirm + Stripe shows why ecosystems are crucial in FinTech 🕸; Are neobanks running out of money? 😬

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Regulators are coming after BNPL’s excessive subprime borrowers 💳

Misleading crypto ads: Coinbase & Crypto.com lead the way 🤷♂️

Banking & payments infrastructure for Web3 economy (could be huge) 👀

NFTs have an insider trading problem 👀

and more!

As for today, here are the 3 FinTech stories that were making a difference this week. It undoubtedly was one of the hottest weeks this year!

BNPL is dead, long live (B2B) BNPL!? 🤔

The money 💸 Only 7 months after it raised a $14M seed round last October, Berlin-based B2B Buy Now, Pay Later (BNPL) startup Mondu is to expand across Europe on the back of a $43M Series A round led by Valar Ventures.

Previous investors Cherry Ventures, FinTech Collective, and tech entrepreneurs and senior executives from Klarna, Zalando, and SumUp have continued to support Mondu in its Series A. To date, the company has raised $57M.

The USP 🥊 Mondu’s BNPL product currently allows for flexible payment terms via direct integration into the checkout process of online merchants. If a business customer decides to use one of the payment methods offered (i.e. invoice (Rechnungskauf) and direct debit (Lastschrift)), while also having flexibility with regards to payment terms, Mondu coordinates the processing of the payments as well as associated services.

The firm last month secured a Banking-as-a-Service collaboration with Raisin Bank, which will add a new option for instalment payments in the future, in addition to setting deferred payment dates via the merchant checkout.

So, what does this mean? In short, BNPL is dead, long live (B2B) BNPL! Here’s the takeaway:

✈️ THE TAKEAWAY

B2B BNPL > B2C BNPL 🚀 Despite this news is following the recent difficulties for BNPL players in the consumer sector, especially given that just last week Klarna fired 10% of its workforce and is set to cut its valuation by 30%, B2B is a whole new story. As it has been said earlier, the B2B payments market is huge and much bigger than its B2C counterpart. Given its accelerated transition to digital over the past couple of years as well as considering that the B2B e-commerce market is also larger than B2C, it’s clear what companies like Mondu are after (so as Playter, Hokodo, Billie, and Tranch, to name just a few). Furthermore, B2B BNPL is believed to be a $200B opportunity just in Europe and the US, which is already bigger than the global consumer BNPL market. Given that the market is currently underserved by existing offerings, and that supply chain financing is a growing need, particularly for SMBs, this could actually be the next big driver in the BNPL market globally.

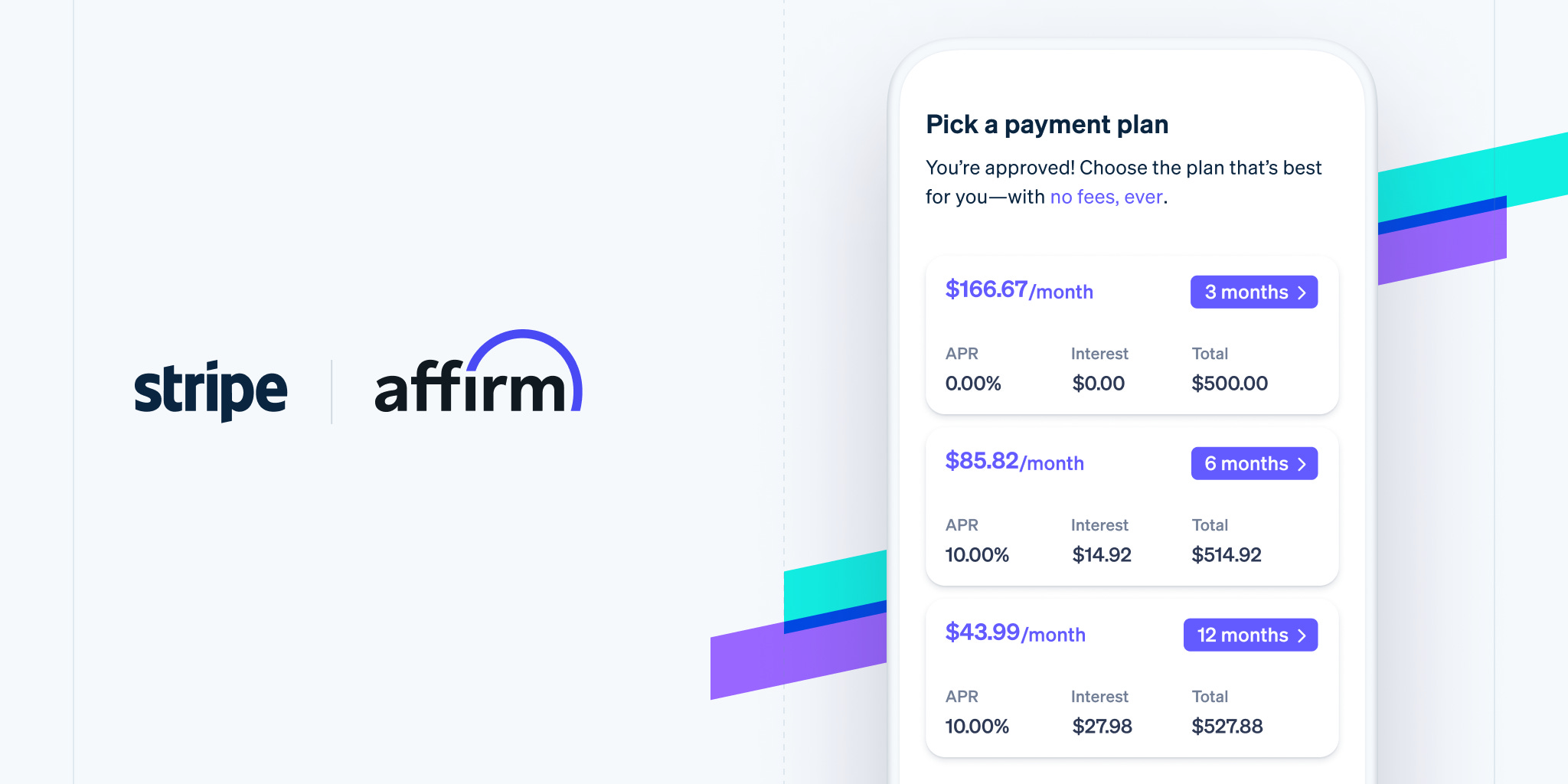

Affirm + Stripe shows why ecosystems are crucial in FinTech 🕸

The deal 🤝 Buy Now, Pay Later (BNPL) pioneer Affirm has partnered with FinTech heavyweight Stripe to drive growth, making Affirm’s Adaptive Checkout available to Stripe users across the US.

In short, this means that thousands of companies using Stripe will now be able to offer their customers the option to pay in installments.

More on this 👉 Affirm’s Adaptive Checkout tool uses the company’s smart decision engine to make a real-time underwriting decision and provide consumers with optimized bi-weekly and monthly installment options side by side.

Businesses using Stripe can now quickly integrate Affirm’s technology and eligible shoppers can split the cost of purchases ranging from $50 to $30,000, with a maximum credit limit of $17,500. Affirm reportedly commits to never charging late fees or hidden charges.

Why does this matter? 🤔 For Stripe, it means more flexibility since now their merchants can offer more options and potentially increase the average order values. While for Affirm, this partnership gives them an opportunity to generate more revenue as it makes money in part on interest fees.

But there’s more to that. Affirm + Stripe is all about the importance of ecosystems. Here’s the takeaway:

✈️ THE TAKEAWAY

The importance of ecosystems & the only proper way of growth. First and foremost, we must stress that Affirm is very good at partnering. I mean, really good. Over the last couple of years alone, the BNPL pioneer in the US has partnered with heavyweights like Adyen, Shopify, Walmart, Amazon, and now Stripe, among others. Zooming out, we must say that partnerships is probably the only single thing that matters in BNPL. The old model that Affirm used (going to each individual merchant directly) was time-consuming, inefficient, and hard to scale. The new one they pivoted to, despite potentially lower revenues, is the real growth engine that gives you access to x1000 more merchants in the same time period. Because the ultimate goal for any BNPL player is to have the largest (exclusive or not) coverage as quickly as possible. So B2B2B2C > B2B2C. That’s the only proper way of growth and Affirm executes it remarkably well.

Are neobanks running out of money? 😬

The news 🗞 US challenger bank Varo Bank risks running out of funds before the end of the year, according to a regulatory filing, as per Banking Dive.

More on this 👉 One can remember that Varo was the first US neobank to obtain a banking charter from the Office of the Comptroller of the Currency (OCC). It was a huge and long-anticipated milestone that reportedly cost Varo around $100M and took 3 years.

Having achieved the above, the challenger bank raised $510M last year and was valued at $2.5 billion. The valuation was mostly associated with their banking charter.

Yet, according to the regulatory filing, by the end of March this year, Varo had $263M in equity and a burn rate of $84M in Q1 2022. At that rate, the bank might run out of money by the end of the year. Wow! 😬

Responding to the reports, Varo’s CEO Colin Walsh assured that the bank would not need to raise additional capital to stay afloat, stating that the figures in the report were taken out of context.

Why does this matter? First, Varo might not be able to raise any fresh funding because of its performance. Second, Varo could be used as a proxy for assessing the future of other neobanks. Here’s the takeaway:

✈️ THE TAKEAWAY

Neobanking is tough. One of the key things to realize about Varo is that it’s not profitable and it’s struggling to become one. Varo used the latest funding to invest in marketing, engineering, product development, etc. but that’s yet to turn a profit. Varo attracted 2.7M new accounts in 2021, but it’s unclear how many of those accounts remain active. Also, the bank has focused on lending as part of its push to obtain a banking charter, but this practice has not been a revenue generator as Varo generates 98% of its revenue from interchange and fee income. Zooming out, we must say that Varo’s struggle for profitability is common within the neobanking space. As noted earlier, most neobanks struggle to turn a profit, with an estimated less than 5% of them breaking even. That’s really little. And without profitability (or at least a clear path towards it), another round of funding is inevitable. But the problem here is that both the current environment as well as Varo’s position are very weak for the new funding to be secured. If Varo goes under, it might definitely hurt the credibility of neobanks globally.

🔎 What else I’m watching

NAB in 4? 😎 National Australia Bank has invited its customers to pre-register for the forthcoming launch of a new Buy Now, Pay Later offering named 'NAB Now Pay Later'. Under the scheme, NAB customers will be able to access up to USD 1,000, split purchases into four payments, use it anywhere Visa is accepted and add NAB Now Pay Later to their digital wallets for online and in-person payments. Unlike other instalment payments or pay-in-four products, NAB’s offering has no late fees, no interest, and no account fees. It’s going to get tough for Aussie BNPLs…

A big boss loss? 🤔 Dutch payments service provider Mollie has appointed Klarna CTO Koen Köppen as its new chief technology officer. Prior to Mollie, Koen spent more than a decade at Klarna, holding several leadership positions and finally becoming its CTO almost 5 years ago. At Mollie, Koen will be responsible for the reliability, scalability, and development of Mollie’s technology platforms. This seems quite a big loss for Klarna which further adds to all the issues it is currently experiencing. A CTO that’s been a decade with the biz doesn’t simply quit if everything is okay…

No SPAC? 🤔 The Binance-supported deal to take Forbes public via SPAC has been called off. This follows the crypto exchange’s $200M strategic investment in the media company in February, which was meant to redirect its focus to covering the emerging digital economy. Given the current market conditions, it makes a ton of sense.

💸 Following the Money

Growth capital funding startup Bloom raised 300M pounds (roughly $376M) to grow its business across Europe and become a leading provider of revenue-based lending for digital startups.

Global payments platform for digital account-to-account transactions Trustly has acquired the UK-based Open Banking Payments platform Ecospend.

HitPay, a payments platform for small- to medium-sized businesses (SMBs), has raised $15.7M in a Series A funding round.

👋 That’s it for today! Thank you for reading and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up: