Finance giants launch AI Shopping Agents in agentic commerce race 🤖🛍️; Revolut & N26 dial into €500B telco market 😳📲; JPMorgan alerts that AI skyscrapers are being built on digital quicksand 🤖🏜

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The Ultimate Beginners Guide to AI 📚🤖 [5,500+ pages of knowledge to transform your understanding from beginner to AI authority]

The Ultimate List of Resources about AI Agents 🤖 [unlock the power of AI Agents: your gateway to the future of autonomous agentic systems]

The Ultimate List of Stablecoin Use Cases 🪙 [discover how stablecoins are quietly revolutionizing finance, business, and daily life across industries]

Agentic AI Playbook for Finance 🤖💸 [a field‑ready reference for product, engineering, and risk teams building autonomous agents in FinTech 📚]

Fiserv is weathering the growth skepticism storm despite strong fundamentals & margin expansion 👀💳 [how the payments giant is weathering the growth skepticism storm despite strong fundamentals & margin expansion and whether it’s worth your time and money in 2025 & beyond + more bonus reads inside]

Citi predicts stablecoins could reach $3.7 trillion by 2030 🪙🔥 [uncovering key insights from the latest Citi report, what to expect next + bonus list of 110+ stables use cases & a deep dive into Citi’s latest financials]

Revolut set to disrupt Irish mortgage market 🇮🇪🏦 [what it’s all about & why it’s exciting + bonus deep dive into Revolut’s 2024 financials]

Mastercard is embracing stablecoin revolution 🪙😤 [what it’s all about & what to expect next + bonus dive into the ultimate list of 110+ stablecoin use cases]

Nubank’s Mexican banking license set to transform digital banking landscape 🏦🇲🇽 [why it matters & what’s next + bonus deep dive into NU and how it’s leveraging AI today]

Banks finally offload $13B in 𝕏 debt 👀💰 [quick recap of the financial engineering here + a bonus dive into x/xAI combo that Musk is going all in with now]

Global 6,200+ Investor Database to Fast-Track Your Funding in 2025 💸 [shorten your fundraising time, find your perfect investors, and close rounds faster]

As for today, here are the 3 phenomenal FinTech stories that are transforming the world of financial technology as we know it. This was yet another intense week in the financial technology space, so make sure to check all the above stories.

Finance giants launch AI Shopping Agents in agentic commerce race 🤖🛍️

The (BIG?) News 🔥 Finance behemoths Mastercard MA 0.00%↑, PayPal PYPL 0.00%↑, and Visa V 0.00%↑ have all unveiled new AI-powered shopping initiatives, signaling a significant shift toward agentic commerce where AI assistants can make purchases on behalf of consumers.

These almost simultaneous announcements from payment industry leaders highlight the rapid acceleration of AI integration into everyday financial transactions.

Let’s take a look at this and see why it matters.

More on this 👉 Let us start with Mastercard's Agent Pay.

Mastercard has introduced Agent Pay, partnering with Microsoft MSFT 0.00%↑ to integrate AI technologies, including Azure OpenAI Service and Microsoft Copilot Studio. The system aims to create more personalized payment experiences by embedding payment capabilities directly into generative AI conversations.

In practical applications, Mastercard envisions scenarios where consumers planning events can interact with AI agents that curate product selections based on preferences, venue considerations, and even weather forecasts. For businesses, AI agents could handle sourcing, optimize payment terms, and manage logistics with international suppliers.

For security, Mastercard has emphasized that AI agents must be registered and verified before executing payments, with enhanced tokenization technology securing transactions initiated through conversational interfaces.

Then comes PayPal's Developer-Focused Approach.

PayPal's announcement centers on enabling developers to create agentic AI experiences where customers can pay, track shipments, and manage invoices within an AI agent environment. The company unveiled the PayPal Agent Toolkit during its Developer Days event, designed to simplify integrations for building AI-driven commerce experiences.

CEO Alex Chriss positioned these developments as part of a broader strategy emphasizing payment service provider capabilities and value-added services. PayPal demonstrated integrations with partners including Google GOOGL 0.00%↑ Cloud, AWS, and Azure AI for various commerce applications.

Of course, Visa joined the movement too.

Following its competitors, Visa announced Intelligent Commerce, which enables AI agents to shop and make purchases based on consumer-specified preferences. Visa Chief Product Officer Jack Forestell emphasized consumer control, stating, "Each consumer sets the limits, and Visa helps manage the rest."

Visa is collaborating with numerous technology partners, including Anthropic, IBM IBM 0.00%↑, Microsoft, OpenAI, and Stripe to develop these capabilities.

✈️ THE TAKEAWAY

What’s next? 🤔 First and foremost, we must note that the simultaneous push into agentic commerce by major payment networks signals a fundamental transformation in how consumers will interact with financial systems. As AI agents increasingly mediate purchasing decisions, payment providers positioning themselves at the core of these transactions ensure their continued relevance in an AI-driven economy. For consumers, these developments promise convenience through delegated shopping that respects preferences while removing friction. For merchants, agentic commerce represents both opportunity and challenge - potentially expanding market reach while requiring adaptation to AI-mediated purchasing behaviors. Looking ahead, the next development phase will likely focus on standardization and interoperability between competing systems. As consumers adopt multiple AI assistants across various platforms, payment providers that ensure seamless authentication and consistent experiences across ecosystems will gain an advantage. Regulatory frameworks governing AI agent payment authority will also need rapid development to address novel questions of liability and consent in this emerging payment paradigm. AI is the way 🤖

ICYMI:

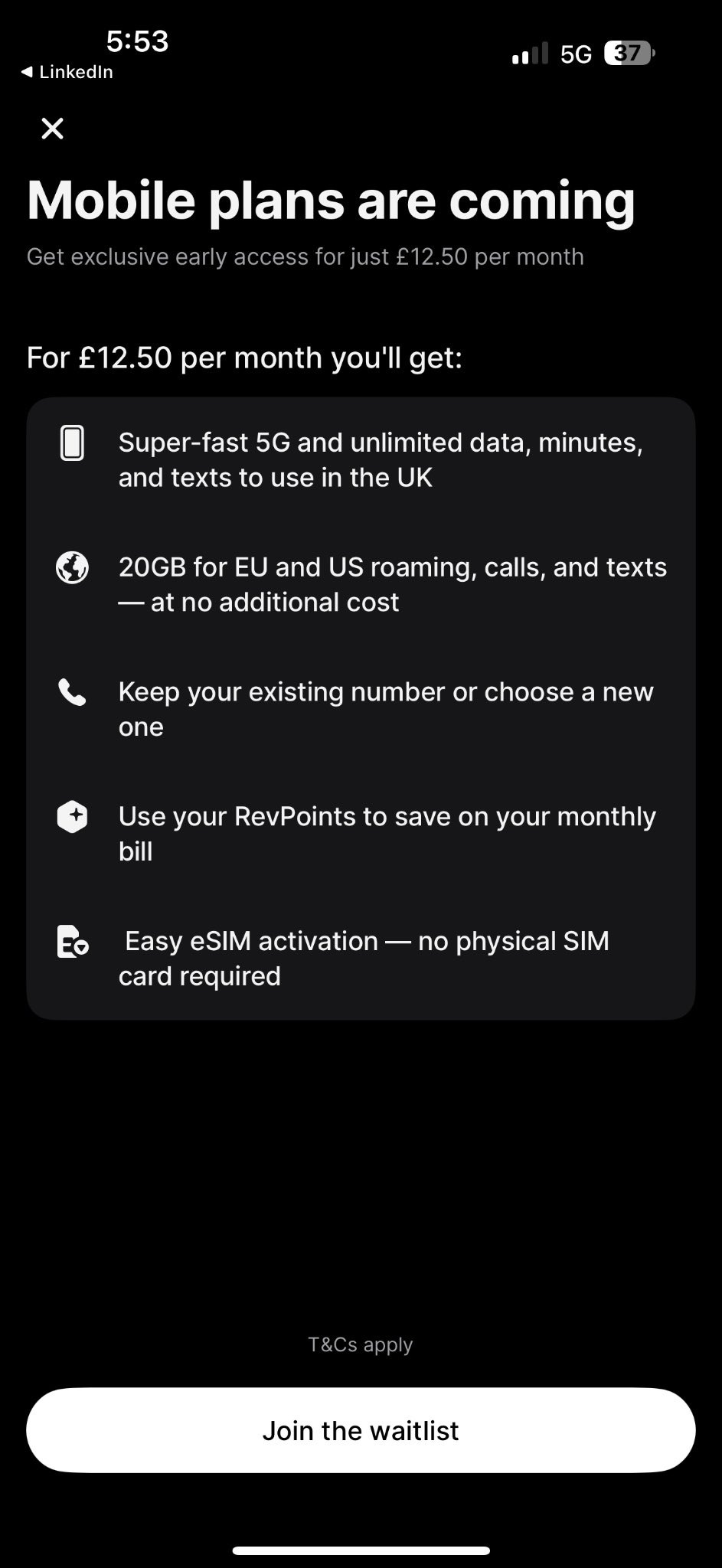

Revolut and N26 dial into €500 billion telecoms market 😳📲

The BIG News 🔥 European neobanking giants Revolut and N26 are expanding beyond financial services to enter the telecommunications sector, with both companies announcing plans to launch mobile services in the UK and Germany.

Let’s take a look at this, see why it matters, and what’s next.

More on this 👉 Revolut will offer a full-service mobile package with unlimited texts, calls, and data at an introductory price of £12.50 in the UK. The plan includes a 20GB roaming allowance across Europe and the US, while German plans will feature 40GB of EU roaming.

The services will be integrated directly into Revolut's app, allowing customers to pay with the company's loyalty scheme points (RevPoints).

N26, based in Berlin, is also set to roll out telecoms services in Germany this month, though specific details of their offering remain unannounced.

Both FinTechs will enter the market as mobile virtual network operators (MVNOs), leasing network capacity from established players rather than building their own infrastructure.

This marks a departure from Revolut's typical strategy of developing projects in-house.

ICYMI:

Zoom out 🔎 The move builds on Revolut's successful eSIM product launched in 2024, which has become the company's top non-banking product in terms of usage, with 600,000 customers purchasing plans used across more than 100 locations worldwide.

While FinTechs may gain a reasonable customer base, they will likely remain smaller players compared to telecommunications giants like Deutsche Telekom, Vodafone, and BT Group that dominate Europe's €500 billion telecoms market.

At least for now.

✈️ THE TAKEAWAY

What’s next? 🤔 First and foremost, this strategic expansion represents a significant evolution in how FinTech companies are redefining their business models. By leveraging their existing digital infrastructure and customer relationships, Revolut and N26 are clearly positioning themselves as Super Apps that extend well beyond their financial origins. The telecommunications move follows Revolut's pattern of diversification, with the company also developing a points-based credit card, private banking for high-net-worth individuals, an AI-powered financial assistant, and mortgage products. With pre-tax profits doubling to £1.1 billion and revenue reaching £3.1 billion, Revolut has the financial flexibility to subsidize these new ventures while building additional customer engagement. Looking at the bigger picture, this represents a potential new playbook where digital-first financial companies leverage their technological advantages and customer trust to disrupt adjacent regulated industries. While telecommunications is today's target, tomorrow could see similar moves into HealthTech, utilities, or other service sectors. The key question here, of course, remains whether these FinTechs can successfully manage the operational complexities of telecommunications while maintaining their core financial offerings. If successful, we may witness the emergence of truly integrated digital service providers that blur traditional industry boundaries and redefine customer expectations across multiple sectors.

ICYMI: Revolut’s profit machine reaches escape velocity with 72% revenue surge and 149% profit growth in 2024 🤯🚀 [deep dive into their 2024 annual report, breaking down the most important numbers, what they mean & why you should be bullish on Revolut + lots of bonus reads inside]

JPMorgan alerts that AI skyscrapers are being built on digital quicksand 🤖🏜️

The news 🗞️ Banking giant JPMorgan Chase's JPM 0.00%↑ Chief Information Security Officer, Patrick Opet, has recently released a critical open letter warning that companies are rushing to deploy AI without understanding the serious security implications, particularly when built on top of already vulnerable SaaS ecosystems.

He isn't mincing words. The way we use SaaS & cloud is fundamentally broken, creating a massive blind spot.

Let’s take a quick look at this and uncover the key insights & lessons.

More on this 👉 The letter highlights how today's interconnected software landscape has created unprecedented risks. Organizations now heavily depend on a small set of SaaS providers, embedding concentration risk into global infrastructure.

Unlike historical software distribution across diverse environments with unique security practices, today's model means an attack on one major provider can immediately impact countless customers.

Opet identifies several critical concerns:

Systemic Risk: Reliance on a few tech giants creates dangerous single points of failure

Security as Afterthought: Competition drives rushed features over robust protection

Collapsed Boundaries: Traditional security walls have disappeared as modern tools connect directly via APIs and tokens

Integration Dangers: Implicit trust between external services and internal systems

AI Amplification: The rapid growth of AI tools magnifies these risks exponentially

JPMorgan has witnessed these threats firsthand, with multiple third-party provider incidents requiring swift isolation of compromised vendors and substantial resources for threat mitigation.

The bank's call to action demands that security must be non-optional and built-in by default. It advocates for modern authorization methods, continuous verification rather than annual checks, and securing connections before deploying powerful AI tools into sensitive environments.

✈️ THE TAKEAWAY

What’s next? 🤔 This warning should be read by everyone in the financial sector, especially those who have eagerly adopted both SaaS solutions and AI technologies. Financial institutions now face a critical dilemma: balancing innovation against security fundamentals. We're likely witnessing the beginning of a significant security paradigm shift. Financial organizations may start demanding more transparency from their tech providers, implementing stricter vendor assessment protocols, and potentially developing more isolated AI deployment models that limit access to sensitive systems. When it comes to FinTech startups, this represents both a challenge and an opportunity. Those who can demonstrate "security by design" principles may gain a competitive advantage, while larger institutions may slow their AI adoption timelines to ensure proper security foundations. Looking ahead, the industry appears headed toward a necessary recalibration – not abandoning innovation, but ensuring it's built on secure architecture. Just as regulatory frameworks eventually emerged for cloud computing, we can expect similar developments for AI implementation in financial services, with JPMorgan's warning serving as a catalyst for this essential evolution.

ICYMI:

P.S. You can read the full letter here.

🔎 What else I’m watching

JP Morgan's Kinexys Gains Traction in the Middle East 🏦 JP Morgan's Kinexys blockchain platform has signed up Qatar National Bank and Saudi National Bank, enhancing their corporate payment systems. Kinexys Digital Payments addresses cross-border payment challenges and enables real-time, programmable payments for treasury operations. With eight major banks in the MENA region now using Kinexys, JP Morgan is supporting the digital transformation of finance in the area. ICYMI: JPMorgan's fortress capital & diversification excellence position it for outperformance amid mounting economic uncertainty 😤 [deep dive into JPMorgan’s latest Q1 2025 financials, breaking down what they mean & what’s next + bonus reads on how JPM is leading in all things AI & more resources inside]

Google Wallet Introduces Digital IDs in UK 📱 Google Wallet now allows UK users to create digital ID passes using their passports, with an initial partnership with Rail Delivery Group for Railcard eligibility verification. Google is also exploring certification within the UK government's digital identity framework for broader use, such as alcohol purchases. Additionally, Google Wallet is expanding digital ID access in the US and launching in 50 more countries for digital pass usage.

Mastercard Enhances Stablecoin Transactions 💳 Mastercard is expanding its stablecoin capabilities with a comprehensive approach to make stablecoin transactions as seamless as traditional payments. Partnering with crypto platforms like MetaMask, Kraken, and Binance, Mastercard enables easy stablecoin use for consumers and businesses. Collaborations with Nuvei and Circle allow merchants to receive payments in stablecoins like USDC, enhancing efficiency and programmability in payments, disbursements, and remittances. ICYMI:

💸 Following the Money

Persona, the verified identity platform used by a host of fintechs, has raised $200M at a $2B valuation.

Dub, a copy trading app that enables users to mimic the portfolio strategies of notable investors, has raised $30M in funding.

Singapore FinTech Surfin snags $26.5M funding.

👋 That’s it for today! Thank you for reading and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Whoa, this is just too good! Cannot believe it's free... thank you sir.