Chime’s flywheel is spinning fast, but can this neobank outrun its own valuation? 🤔🏦; SoFi just made stablecoin settlement a banking feature, not a crypto experiment 🪙🏦

FinTech is Eating the World, 4 March

Hey Everyone,

Good morning & happy Wednesday! Today’s issue is the best one yet as we’re diving deep into Chime to see whether this neobank can outrun its valuation (deep dive into their latest Q4 & full 2025 year financials, breaking down the most important facts & figures, what they mean and whether Chime is worth your time & money in the years to come), and SoFi, which just partnered with Mastercard to enable SoFiUSD stablecoin settlement across the entire payments giant’s network (what it’s all about, why it could be huge & change lots of things + bonus deep dives into SoFi, Mastercard, and the ultimate list of stables resources inside). So let’s jump straight into the finnovative stuff 🌶️

Chime’s flywheel is spinning fast, but can this neobank outrun its own valuation? 🤔🏦

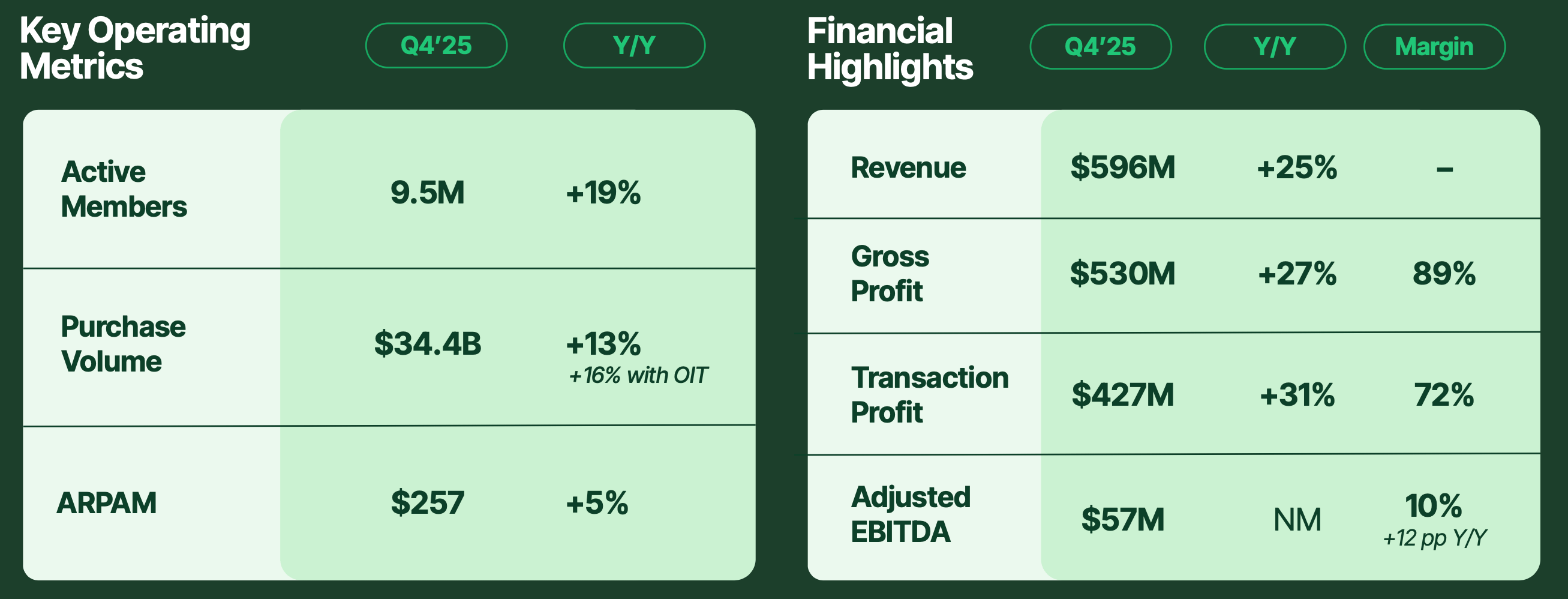

Earnings time ☎️ Chime CHYM 0.00%↑ is now the dominant US neobank, and its Q4 2025 results confirm that the company is well transitioning from hypergrowth fintech into a durable, profitable financial platform.

Full-year revenue hit $2.19 billion (up 31%), Q4 adjusted EBITDA reached $57 million at a 10% margin, and the credit card mix shift is accelerating revenue per member without adding a single new customer. Nice!

The business is real. The key question now is whether the current equity price adequately discounts the execution risk ahead.

Let’s dive deeper into this, break down the most important Q4 and full-year 2025 financial facts & figures, understand what they mean, and see whether Chime is worth your time and money in the years to come.