Revolut is the most profitable FinTech on Earth, and it hasn’t even started lending yet 🤯📈

FinTech is Eating the World, 24 March

Hey Everyone,

Good morning & happy Tuesday! Today, all eyes are on Revolut, which just dropped its 2025 annual report, and the numbers are genuinely absurd. We're going to unpack the fee-income fortress that makes Revolut structurally different from every competitor, the lending optionality coiled inside that balance sheet, the regulatory dominoes now falling in sequence, and whether $75 billion is expensive or whether the market is about to find out it was way too cheap (plus more bonus reads on Revolut, how it’s leveraging AI & bonus deep dives into the latest financials of Nubank, SoFi, Robinhood, and Coinbase inside). So let’s jump straight into the fascinating stuff 🌶️

Revolut is the most profitable FinTech on Earth, and it hasn’t even started lending yet 🤯📈

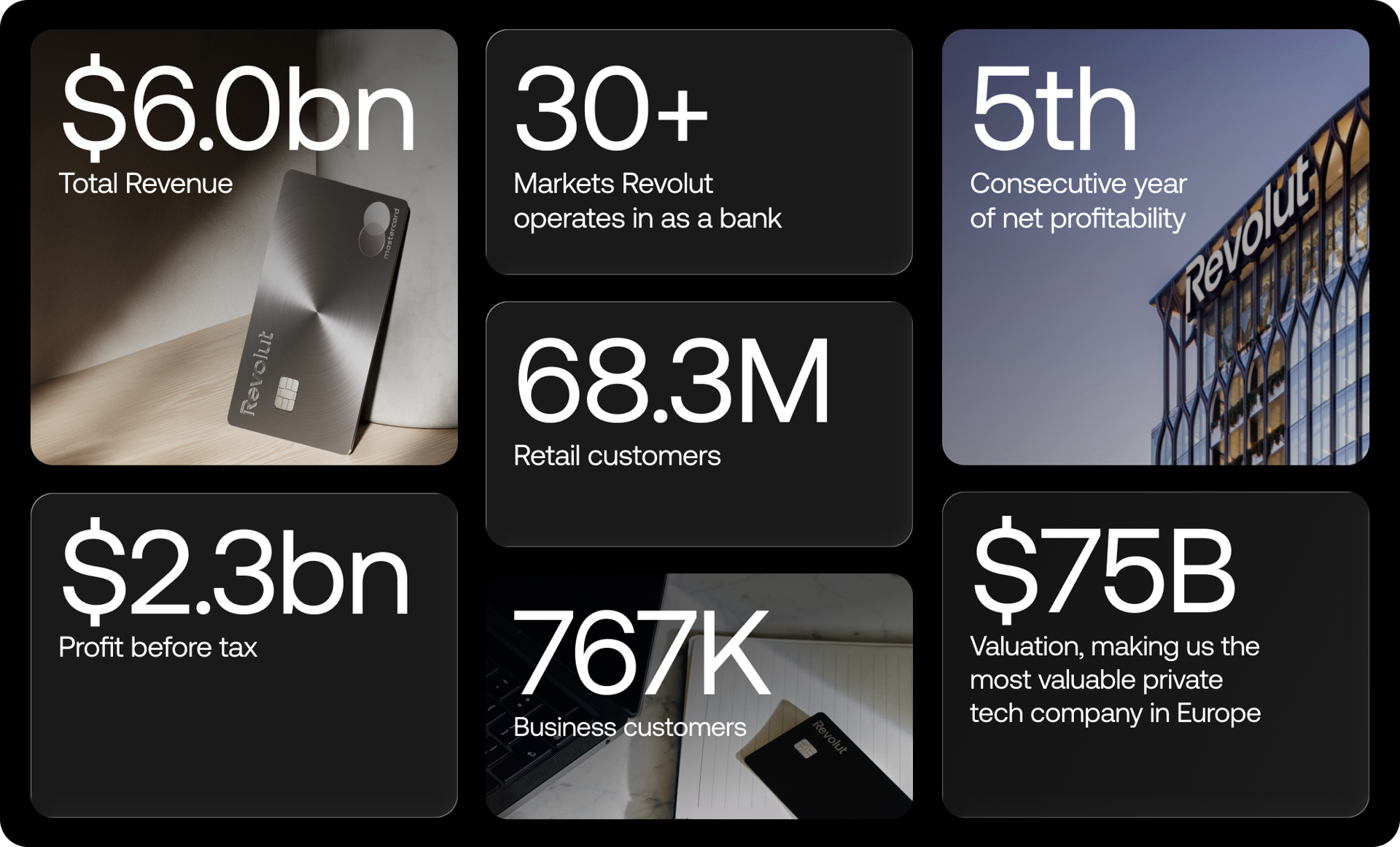

Following the money 💸 Europe’s most valuable private company just published its 2025 financial results and annual report. And one number buried in Revolut’s 2025 annual report tells you more about the company’s future than any headline figure.

It is not the £4.5 billion in revenue, the £1.7 billion in pre-tax profit, or the 68.3 million customers. It is the loan-to-deposit ratio: 6.2% 😳

That number means Revolut is sitting on roughly £36 billion in on-balance-sheet deposits and has lent out only £2.2 billion.

→ A typical European bank lends 70% to 90% of its deposit base.

→ JPMorgan Chase JPM 0.00%↑ runs above 50%.

→ Even Nubank NU 0.00%↑, the closest global comparator, deploys deposits far more aggressively.

Revolut, by contrast, has built one of the most profitable financial technology companies in history while leaving almost its entire balance sheet idle. The lending engine has not been switched on. When it is, the math changes in ways the current $75 billion valuation does not fully capture.

Let’s dive in, unpack the most important financial facts & figures, and see what’s next for Revolut.