Revolut is building a valuation staircase to a $150 billion IPO 😳📈; Robinhood’s listed VC fund is a Trojan horse for the entire private market 😳📈

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

Productize Yourself 🧠 [Naval Ravikant’s framework for building a one-person company is the best startup strategy of 2026. Here’s the operating system, and 13 AI prompts to run it]

The 2035 Global Intelligence Crisis 🌍🧠 [The most dangerous AI prediction isn’t the one that went viral]

What to Build in 2026 🚀 [The startup ideas every top VC is funding right now, the pitch decks that worked, and how to build them]

Stripe doesn’t need PayPal. That’s why it might buy it 💳♟️ [~3,000 words deep dive into why Stripe doesn’t actually need PayPal and that’s exactly why it might buy it, the real strategic logic most coverage is missing, how Adyen fits into the picture, the Elon Musk angle, and what a deal would mean for the entire payments industry + lots of bonus reads & resources on Agentic Commerce, AI in Finance, etc. inside]

The Android of Commerce - How Google Is Building the Interface Between AI & Money 🤖💸 [why recently introduced WebMCP is a game-changer, how it stacks perfectly into Google’s Android of Commerce playbook, things worth watching, what’s next for FinTechs/Banks/Payments companies, etc. + bonus deep dives into Google’s UCP, how I built an AI OS to run startup with Claude, and how AI is eating software today]

Klarna is a $5 billion digital bank growing at 38%, but the market is pricing it like a broken subprime lender 🤷♂️🏦 [deep dive into Klarna’s latest financials, breaking down the most important facts & figures, what they mean & why Klarna might be worth your time and money this year + bonus deep dives into Klarna’s AI plays inside]

The toll booth on the internet’s money highway: Circle’s $75B stablecoin empire is printing cash, but the yield curve is its landlord 🤷♂️🏦 [deep dive into their latest Q4 2025 financials, breaking down the most important facts & figures, and why Circle is one of the most interesting risk/reward setups in fintech right now + bonus deep dive into its key partner Coinbase inside]

AI Just Killed the User Interface 🧠🖥️ [Anthropic AI launched an app layer inside Claude, & it changed the role of SaaS entirely]

Turn Claude From a Chatbot Into a Thinking Partner 🧠 [Most people prompt Claude like it’s Google. Here’s the framework Anthropic actually recommends]

Turn Claude Sonnet 4.6 Into Financial Analyst That Never Sleeps 📊 [Most analysts are leaving 90% of Claude on the table. Here’s the framework that turns the world’s best-value AI into a senior financial analyst]

Top 10 AI Startups to Watch in 2026 🤖🦄 [Strategies, stories, and GTM blueprints from the fastest-growing AI companies that have collectively raised $500M+]

As for today, here are the 2 fascinating FinTech stories that are transforming the world of financial technology as we know it. This was yet another wild week in the financial technology space, so make sure to check all the above stories.

Revolut is building a valuation staircase to a $150 billion IPO 😳📈

The news 🗞️ Revolut doesn’t need the money. It’s raising anyway 🤷♂️

The $75 billion fintech is weighing another secondary share sale for the second half of 2026, with investors pushing for a $100 billion price tag. That would mark the third step in a valuation ladder that started at $45 billion in 2024, climbed to $75 billion last year, and is aimed squarely at a $150 billion IPO 🤯

Each round has been oversubscribed. Each round has brought in heavier names: Coatue, Fidelity, Andreessen Horowitz, T. Rowe Price, and Nvidia’s NVentures. The pattern is deliberate.

Let’s understand why.

More on this 👉 What Revolut is doing isn’t fundraising in the traditional sense. The company is running a price discovery exercise in slow motion, using secondary sales to ratchet up its valuation with institutional anchors before it ever files an S-1. Every oversubscribed round becomes a data point that de-risks the IPO pricing conversation. And with £4.1 billion ($5.5 billion) in projected 2025 revenue, the growth story is real enough to sustain it.

Meanwhile, the company picked up a quieter win: the FCA selected Revolut as one of just four firms (from 20 applicants) to test stablecoins in its regulatory sandbox. Revolut is exploring a pound-denominated stablecoin pegged one-to-one to sterling. For a company that still hasn’t exited its UK banking licence “mobilisation” phase after 18 months, getting chosen for a new regulatory program is a useful signal that the relationship with UK watchdogs isn’t as frozen as the licence delays suggest.

ICYMI:

Zoom out 🔎 The listing question remains unresolved but telling. CEO Nik Storonsky said in December that an IPO is “not a priority” and sits 2 to 3 years out, with Wall Street the likely venue over London.

Chancellor Rachel Reeves personally opened Revolut’s Canary Wharf headquarters last year and reportedly tried to broker a meeting with regulators, only to be blocked by Bank of England Governor Andrew Bailey over concerns about political interference.

If Revolut does choose New York, it will be the most expensive rejection the City of London has absorbed in years. Though not really surprising…

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch for two things. First, whether the $100 billion round closes before year-end. If it does, the IPO timeline likely compresses regardless of what Storonsky says publicly. Second, the stablecoin sandbox. If Revolut ships a functional GBP stablecoin while its banking licence remains in limbo, it will have built a parallel payments rail inside the UK system without the full licence that the Bank of England has been slow to grant. That’s a negotiating position, not just a product.

ICYMI:

Robinhood’s listed VC fund is a Trojan horse for the entire private market 😳📈

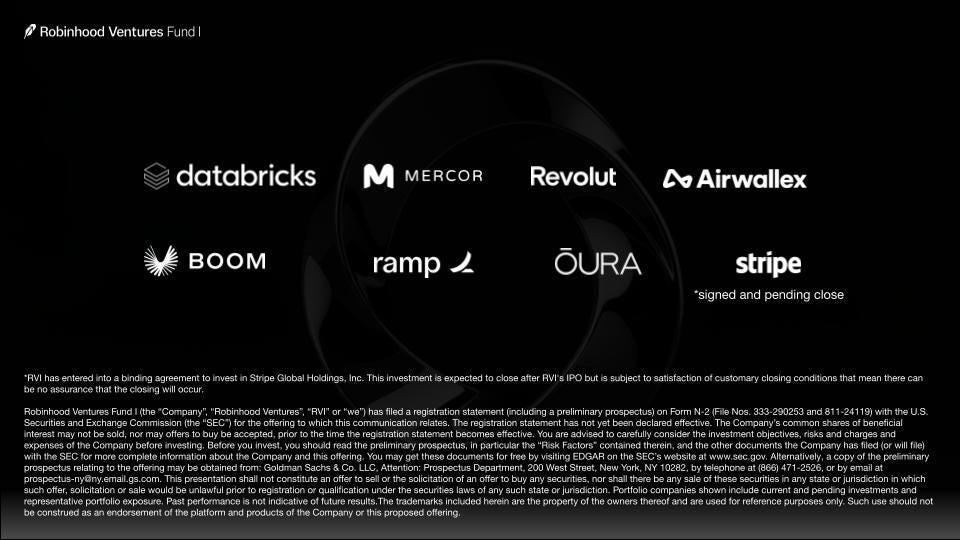

The news 🗞️ The most interesting thing about Robinhood Ventures Fund I isn’t what it holds. It’s what it permits.

Let’s take a quick look at this.

More on this 👉 Robinhood filed to IPO a closed-end fund on the NYSE under ticker RVI, targeting $1 billion at $25 per share. The fund holds stakes in Databricks ($75 million), Revolut ($50 million), Airwallex, Ramp, Oura, and others, with a post-close commitment to buy $14.6 million in Stripe secondaries.

No accredited investor requirement. No minimum check. A 2% management fee, halved for the first six months, and zero carry. Goldman is leading the book. Trading is expected by early March.

Zoom out 🔎 The structure matters more than the portfolio. By wrapping private stakes in a listed CEF, Robinhood sidesteps the regulatory barriers that have kept retail money out of venture for decades. Unlike its failed attempt to tokenize OpenAI stock for European users last year, the fund actually owns the equity - common and preferred shares bought with the company cooperation. Databricks, Ramp, and Airwallex all named Robinhood Ventures in their round announcements.

But CEFs are a known minefield. Destiny Tech100, the closest precedent, currently trades at a 47% premium to NAV because retail demand for SpaceX and OpenAI exposure overwhelms the tiny float. If RVI follows that pattern, early buyers get a meme stock wearing a venture costume. Robinhood selling 5 million of its own shares at IPO - pocketing roughly $125 million - doesn’t exactly quiet the alignment questions 🤔

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, the second-order play is far more interesting. Fundrise and Akkadian Ventures both plan competing public fund listings within weeks. Coatue dropped its LP minimum to $50,000 last year. As Fundrise CEO Ben Miller put it, these “PVCs” - public venture capital - will be normal within a few years. If RVI trades well, expect every large VC firm to start modeling a retail-facing vehicle. If it trades like Destiny Tech100, regulators will have a fresh reason to intervene. Watch the NAV premium on day one. That single number will tell you whether Robinhood built a product or a hype trade.

ICYMI: Robinhood: the $4.5 billion revenue dark horse that Wall Street still underestimates 🤷♂️📉 [deep dive into their Q4 & full year 2025 financials, what stands out, and why I’m still really bullish]

What else I’m watching

AI Targeting Finance Jobs 🤖 Deutsche Bank’s AI tool, dbLumina, predicts that AI will increase global GDP and labor productivity but will disrupt data-rich sectors like IT and finance. Wealth management is expected to see significant disruption, with AI already impacting algorithmic trading, fraud detection, and customer service. Jobs involving structured data processing are at risk, while sectors relying on emotional intelligence, manual dexterity, or strategic leadership are safer. Careers in AI-related fields are also expected to be secure. ICYMI:

Anthropic Enhances Claude Cowork for Finance 💼 AI giant Anthropic has introduced customizable plugins for its Claude Cowork agent software, designed to automate tasks in financial services areas such as investment banking and wealth management. These plugins enable enterprises to tailor Claude into specialized agents for various roles and departments. Key features include tools for financial analysis, investment banking, equity research, and private equity, each offering specific functionalities like market research, document review, and portfolio analysis. Additionally, clients can connect Claude Cowork to existing tools like Google Drive, Gmail, DocuSign, and FactSet to streamline workflows without replacing current expertise or software. ICYMI:

RBC Advances AI Integration 🤖 The Royal Bank of Canada has formed a dedicated AI Group to hasten the adoption of artificial intelligence, aiming to generate up to C$1 billion in enterprise value from AI by 2027. This new team, led by Bruce Ross, will focus on transitioning early-stage AI projects to scalable deployments and advancing research in generative and agentic AI while ensuring security and regulatory compliance. With nearly 27,000 employees already using AI tools like RBC Assist and Aiden, the group will also provide training and support to over 100,000 employees worldwide to integrate AI into their daily work, enhancing decision-making and productivity. ICYMI:

💸 Following the Money

SME-focused Allica Bank has raised $155M in a Series D round that values the fast-growing fintech at $1.2B.

Stripe and PayPal Ventures have joined in a $16.6M funding round for Indian cross-border payments business Xflow. ICYMI: Stripe doesn’t need PayPal. That’s why it might buy it 💳♟️ [~3,000 words deep dive into why Stripe doesn’t actually need PayPal and that’s exactly why it might buy it, the real strategic logic most coverage is missing, how Adyen fits into the picture, the Elon Musk angle, and what a deal would mean for the entire payments industry + lots of bonus reads & resources on Agentic Commerce, AI in Finance, etc. inside]

Visa has struck a deal to buy Argentinian payments firms Prisma Medios de Pago and Newpay from private equity giant Advent International. Financial terms were not disclosed. ICYMI: World’s Tollbooth: Visa’s unbeatable moat justifies premium valuation, but upside is limited 🤷♂️💳 [breaking down the most important Q1 2026 financial facts & figures, understanding what they mean, and what’s next for Visa]

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Good read - thank you!