Robinhood’s Q1 2026: the best brokerage, the wrong price 🤷♂️💸; Anthropic made the EU come asking for Claude Mythos 😳🇪🇺

FinTech is Eating the World, 2 June

Hey Everyone,

Good morning & happy Tuesday! Today we’re diving deep into Robinhood’s latest financials to see why it’s the best brokerage at the wrong price (breaking down the most important facts & figures from Robinhood’s Q1 2026 to see whether Robinhood is worth your time & money + bonus deep dive into the latest financials of its bigget competitor Coinbase, and why Robinhood’s Agentic AI play is exactly what Anthropic recently told AI founders to build in 2026), and Anthropic, which just made the EU come asking for Claude Mythos (what it tells us, what it matters & what’s next for AI deployment + bonus deep dive into Everything Anthropic Shipped in 2026 & How to Actually Use It). So let’s jump straight into the interesting stuff 🌶️

Robinhood’s Q1 2026: the best brokerage, the wrong price 🤷♂️💸

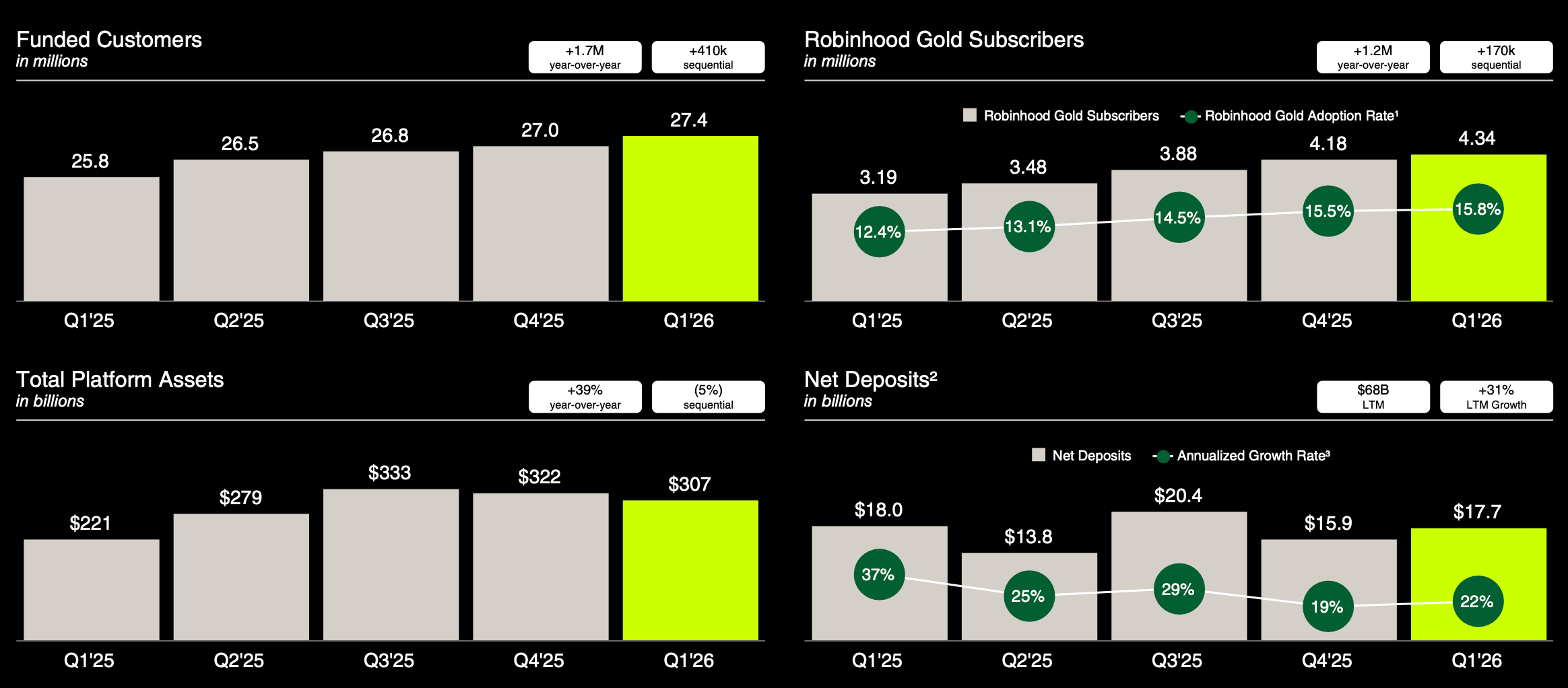

Earnings time 🤑 Robinhood HOOD 0.00%↑ is the best-run brokerage of its generation, and the first quarter proved that quite well.

Platform assets reached $307B, up 39% year over year. Trailing-twelve-month net deposits hit $67.8B, and they keep flowing straight through every market drawdown. Gold subscribers climbed 36% to a record 4.3M. Revenue crossed a billion dollars in a single quarter, on what Morningstar calls the richest unit economics of any broker its size. Let that sink in.

And yet the most important number in the quarter wasn’t the 15% revenue growth or the 39% jump in platform assets. It was 92% - the share of revenue that is cyclical trading flow or rate-sensitive spread, the part that thins the moment crypto cools and the Fed starts cutting. You didn’t have to wait to watch it happen. Sequentially, revenue fell 17%, and net income fell 43%, the instant both did 🤕

The tension between those two stories, a franchise that compounds through anything and a P&L that buckles on a dime, is exactly what makes Robinhood arguably the most interesting risk/reward profile in fintech right now. The market pays north of 40 times earnings, the multiple of a secular compounder, for a business that just behaved like the high-beta cyclical it has always been.

Let’s dig in deeper into Robinhood’s Q1 2026, unpack the figures that actually matter, and see whether Robinhood is worth your time & money in the years to come.