EMEA FinTech gets hit the hardest in funding downturn 📉🫣; Rapyd acquires a piece of PayU from Prosus for $610M 🤯; Klarna kills its Open Banking brand 😵

FinTech is Eating the World, 1 August

Hey Everyone,

Happy Tuesday! Today we’re looking at the latest data on the global FinTech funding for H1 2023 (EMEA FinTech gets hit the hardest + priceless startup resources), Rapyd that just acquired a piece of PayU for $610M (it’s all about FaaS), and Klarna which just killed its Open Banking brand (but it’s a smart move!). Let’s jump straight into interesting stuff 🌶

EMEA FinTech gets hit the hardest in funding downturn 📉🫣

The latest data is out 📊 In early July, I talked about European FinTech funding in the first half of 2023, and it wasn’t good. We now have data on the global FinTech funding for the first 6 months of 2023.

Let’s take a brief look at the most important things.

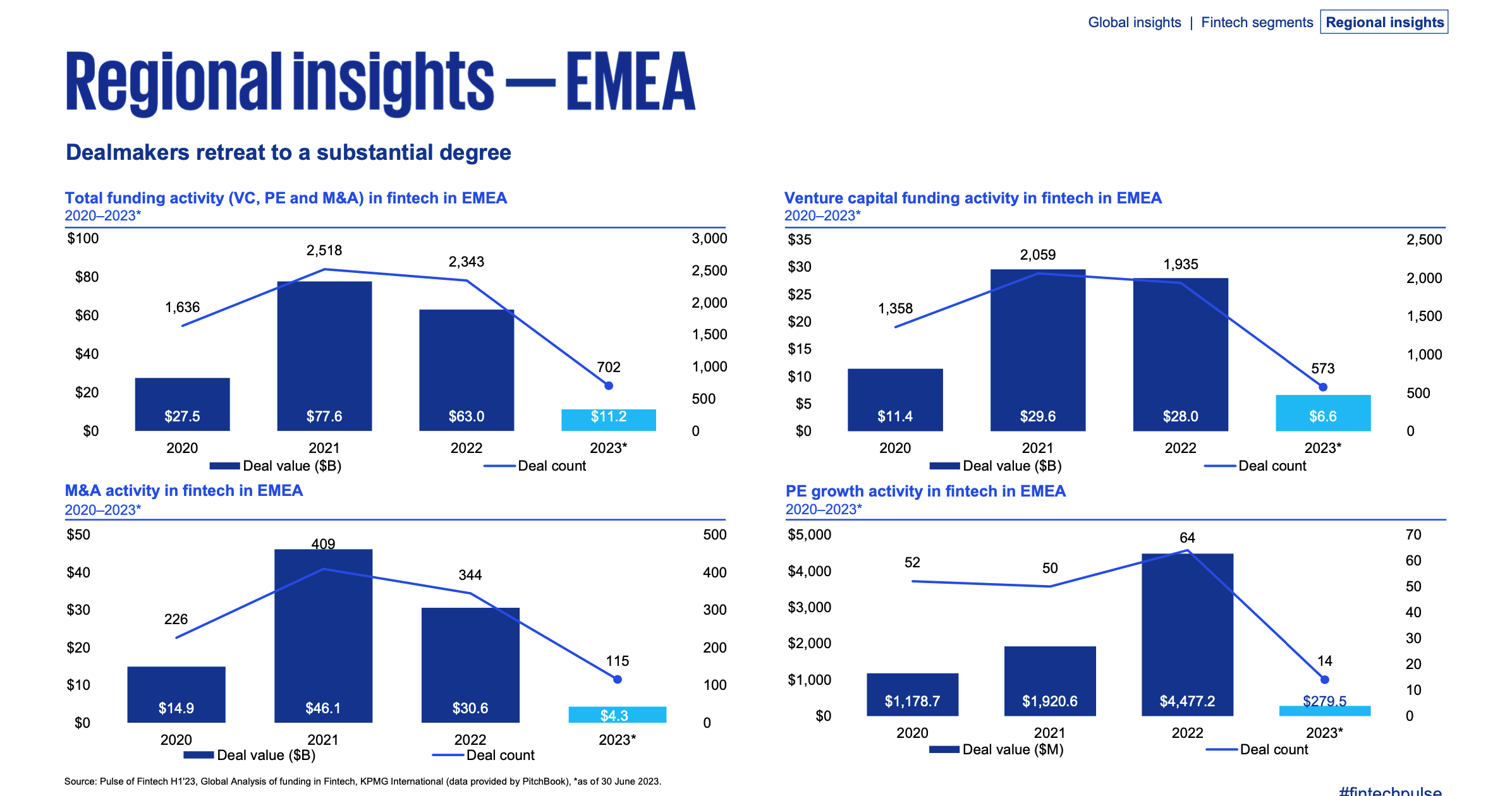

More on this 👉 Top things to know from the latest KPMG Pulse of FinTech report:

Global FinTech funding fell sharply from $63.2 billion in H2'22 to $52.4 billion in H1'23, with Q2'23 results particularly weak at just under $18 billion invested. This reflects a pullback by investors amid high inflation, rising interest rates, the Russia-Ukraine conflict, depressed valuations, and a lack of exits.

The US accounted for over two-thirds of global FinTech funding in H1'23 with $34.9 billion invested. The Americas overall saw funding rise from $28.9 billion in H2'22 to $36 billion in H1'23. Not bad! 👏

Funding in the EMEA and ASPAC regions declined significantly in H1'23 compared to H2'22. EMEA dropped from $27.3 billion to $11.2 billion and ASPAC went from $6.7 billion to $5.1 billion. Brutal… 🤕

Fintechs focused on improving operational efficiency and cash flows as funding sources dried up. Investors enhanced due diligence and prioritized profitable, sustainable business models.

Payments remained relatively resilient, attracting over $16 billion in H1'23. However, funding shifted from BNPL models to more mature, core payments capabilities.

Interest in AI and generative AI solutions accelerated, especially for cybersecurity, wealth management, and insurance use cases. This is likely to drive funding in H2'23.

Crypto funding slowed dramatically but interest persists in blockchain for ESG applications like carbon credits.

✈️ THE TAKEAWAY

What’s next? 🤔 Looking ahead, funding is likely to remain subdued in H2'23 until macro conditions stabilize. But the long-term outlook is still positive. Key trends to watch for the future include increasing M&A (3 of them in today’s newsletter + resources below), more corporate ventures investing in operational efficiency solutions, accelerating the development of AI solutions, and resilient funding in payments. To be prepared and make the most of it, I’ve got some valuable stuff for you👇🏼

If you’re building and scaling, read this:

If you’re raising right now, check these:

If you’re looking to do an M&A, these are must: