Mastercard bridges crypto & TradFi with non-custodial Bitcoin debit card 🪙💳; Mercury expands FinTech offerings with Teal M&A 🤝🏦; Digital assets poised for major institutional adoption 📈💸

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The Startup Growth Toolkit: Top 5 Resources to Scale Your Business to New Heights 🚀 [unlock the secrets to startup success with these essential resources]

Top resources for building and scaling billion-dollar startups 🦄 [600+ pages of knowledge and advice to launch & scale your next unicorn in 2024]

Card Giants under fire: Visa & Mastercard face £4B lawsuit over "illegal" fees 😳💳 [what it’s all about, why it matters & what’s next + a bonus deep dive in both Visa & Mastercard]

FinTech M&A is back: Paylocity makes a move into spend management with $325M Airbase acquisition 🤝💸 [why it’s a good move that makes brilliant sense & how will it change the future intersection of all things HR + FinTech]

Fidelity Bank & Mastercard team up to revolutionize cross-border payments in Nigeria 🤝🇳🇬 [what’s the USP here & why it matters + a bonus deep dive into both Visa & Mastercard]

Middle East’s FinTech sector is heating up with strategic M&As 🇦🇪🇸🇦 [a holistic view of two interesting M&As, what they tell us & what can we expect next]

Revolut is aggressively expanding its B2B offerings 💸🚀 [what’s the latest B2B push is all about & why it matters + some bonus dives into Revolut inside]

Crypto.com and PayPal join forces to streamline crypto purchases 🤝💸 [what it’s all about & why it matters + a bonus deep dive into PayPal]

Gen AI for Compliance as the next growth frontier for FinTech? 🤖🛡️ [a look at Sedric AI that just closed their Series A, what’s their USP & why it’s interesting + what’s ahead of us & a bonus read on AI agents in FinTech]

As for today, here are the 3 fascinating FinTech stories that were transforming the world of financial technology as we know it. This was one of the most intense and fascinating weeks in the whole of 2024 so far, so make sure to check all the above stories.

Mastercard bridges crypto and traditional finance with non-custodial Bitcoin debit card 🪙💳

The launch 🚀 In a bid to bridge the worlds of cryptocurrency and traditional finance, payments titan Mastercard MA 0.00%↑ has just launched a euro-denominated debit card that allows users to spend Bitcoin and other cryptocurrencies directly from their non-custodial wallets.

Developed in partnership with crypto payment providers like Mercuryo, it enables Bitcoin holders to make purchases at over 100 million Mastercard merchants globally without first converting their crypto to fiat currency.

Let’s take a quick look at this and see why it matters.

More on this 👉 The new card reportedly addresses a key pain point for crypto enthusiasts by eliminating the need to transfer funds to a centralized exchange before spending.

Users can now maintain full control of their digital assets in self-custodial wallets while enjoying the convenience of widespread merchant acceptance. This approach aligns with the core cryptocurrency principle of self-custody, where users are solely responsible for securing their private keys and funds.

Mastercard's initiative includes several key features:

Support for multiple cryptocurrencies, with Bitcoin being a primary focus

Integration with Apple Pay and Google Pay for enhanced convenience

Automatic conversion of crypto to fiat at the point of sale

Availability to users in the European Economic Area, with plans for global expansion

Despite significant benefits, the card does come with some fees, including a €1.60 issuance fee, a €1 monthly maintenance fee, and a 0.95% transaction fee.

✈️ THE TAKEAWAY

What’s next? 🤔 First and foremost, this is all about mainstream adoption. By making it easier to spend Bitcoin and other cryptocurrencies, Mastercard is accelerating the mainstream adoption of digital assets. This could lead to increased acceptance of crypto as a legitimate form of payment among both consumers and merchants. In relation to that, we can expect more competition in the financial sector. Traditional banks may thus feel pressure to offer similar crypto-friendly services to remain competitive. And this could spark a wave of innovation in the banking sector as institutions scramble to integrate cryptocurrency services. Looking at the big picture, this move is also another step towards the evolution of payment infrastructure. Mastercard's initiative may thus prompt further development of payment infrastructure that seamlessly bridges fiat and cryptocurrency systems. This could effectively lead to more efficient, lower-cost payment solutions in the long term (which would be a massive win for everyone). Zooming out, Mastercard's non-custodial Bitcoin debit card represents a significant milestone in the convergence of traditional and decentralized finance. It has the potential to reshape how we think about and use money in the digital age, bringing us one step closer to a world where crypto is as easy to use in daily life as traditional currencies. Bullish.

ICYMI: Card Giants under fire: Visa and Mastercard face £4 billion lawsuit over "illegal" fees 😳💳 [what it’s all about, why it matters & what’s next + a bonus deep dive in both Visa & Mastercard]

Mercury expands FinTech offerings with Teal acquisition 🤝🏦

The news 🗞️ Mercury, a digital banking startup for businesses, is again making some solid strides in the increasingly competitive FinTech landscape.

The company just acquired Teal, a seed-stage startup specializing in accounting products, and introduced new software features to enhance its financial services offerings.

Let’s take a look at this, see why it matters, and what’s next.

More on this 👉 Founded in 2019, Mercury has quickly grown to serve over 200,000 customers, processing $4 billion in monthly outgoing payments. While initially focused on startups, the company has diversified its customer base, with startups now comprising less than 40% of its clients.

The acquisition of Teal brings valuable expertise in accounting and strengthens Mercury's relationships with accountants. More importantly, this move aligns well with Mercury's vision of simplifying complex financial workflows around bank accounts.

Zoom out 🔎 In addition to the above, we must remember that Mercury has been rolling out new software features integrated directly into its bank accounts, including:

Advanced bill pay capabilities with AI-powered features

Accounting automation with NetSuite integration

Invoicing tools (coming soon)

Employee reimbursement features (coming soon)

These additions therefore position Mercury in direct competition with established players like Brex, Ramp, and Bill.com. It’s clear that the company aims to provide a comprehensive financial hub for businesses, reducing the need for multiple disconnected tools.

ICYMI: Bill.com's Q4 2024: a high-growth FinTech juggernaut with an expanding moat, but valuation remains a concern 🤔📈 [breaking down the key Q4 2024 numbers, strategic outlook & what’s next for BILL 0.00%↑ + a collection of bonus deep dives into FinTech stocks you can’t afford to ignore]

But Mercury's expansion isn't limited to business banking. Earlier this year, the FinTech heavyweight has also ventured into personal banking, offering services for a $240 annual subscription fee upon first deposit.

✈️ THE TAKEAWAY

What’s next? 🤔 Both Mercury's acquisition of Teal and Paylocity's acquisition of Airbase (more on this - below) reflect a broader trend of consolidation in the FinTech space. Companies are increasingly looking to offer comprehensive financial management solutions that cover multiple aspects of business operations. More importantly, Mercury's move into accounting infrastructure through Teal also aligns with the growing competition for the CFO stack. Similar to how Paylocity is expanding from HR into finance, Mercury is expanding from banking into accounting. This trend hence suggests that FinTech companies are recognizing the value of offering integrated solutions that cater to various aspects of financial management. Zooming out, this M&A positions Mercury to compete more effectively not just with other neobanks, but also with traditional banks and financial software providers that might be slower to innovate. Given the trend of consolidation in the FinTech space, we might see Mercury make additional strategic acquisitions to further expand its capabilities, particularly in areas that complement its banking and accounting offerings. On top of that, like Paylocity, Mercury may find significant opportunities in catering to mid-market companies that need comprehensive, integrated financial solutions but may be underserved by enterprise-level offerings. Lastly, the combination of banking and accounting data could allow Mercury to develop unique insights and forecasting tools, potentially giving it a competitive edge in the market.

ICYMI: FinTech M&A is back: Paylocity makes a move into spend management with $325M Airbase acquisition 🤝💸 [why it’s a good move that makes brilliant sense & how will it change the future intersection of all things HR + FinTech]

Digital assets poised for major institutional adoption 📈🪙

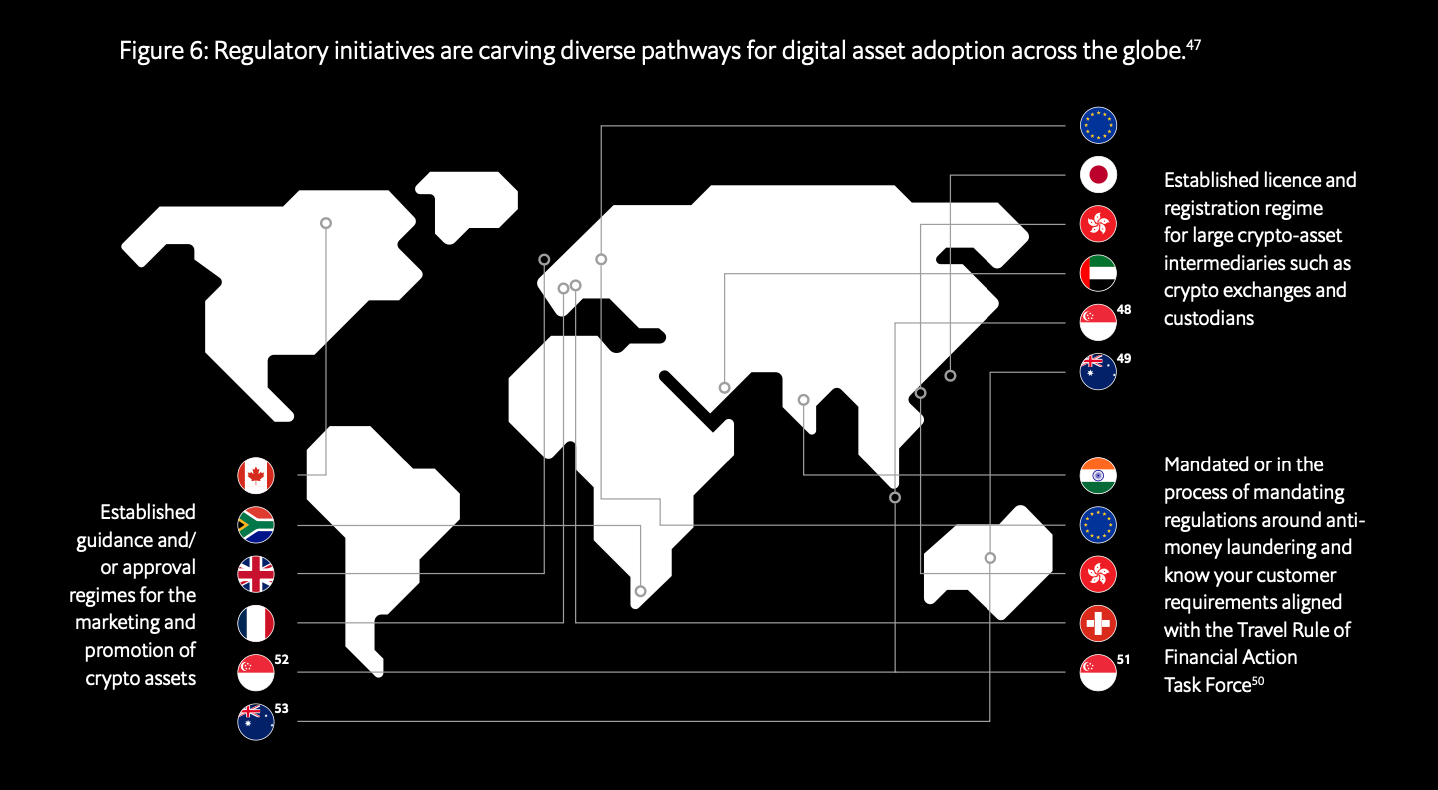

The news 🗞️ Digital assets are rapidly emerging as a significant opportunity for institutional investors, according to new research commissioned by crypto exchange OKX and authored by Economist Impact.

The study, which draws insights from industry leaders and experts, highlights four key areas of focus for institutions entering the digital asset market: asset allocation, custody, regulation, and risk management.

Let’s take a quick look at this, see why it matters, and what’s next.

More on this 👉 The research indicates a growing consensus among institutional investors that digital assets, including cryptocurrencies, NFTs, and tokenized private funds, have an important place in portfolio allocations.

Current allocations average between 1% to 5%, with projections suggesting this could increase to 7.2% by 2027.

An impressive 69% of institutional investors anticipate increasing their digital asset allocations within the next 2-3 years 😳

Custody solutions are evolving to meet institutional needs, with 80% of hedge funds investing in digital assets using third-party custodians. The institutional digital asset custody market alone is expected to grow at a compound annual rate of 23% through 2028, underscoring the demand for specialized security and management solutions. This is massive!

Regulatory developments are playing a crucial role in facilitating adoption. The convergence of regulatory frameworks across jurisdictions is addressing market uncertainties and enhancing consumer protection. Notable examples include the approval of spot Bitcoin ETFs in the US and comprehensive guidance on digital asset custody in Hong Kong.

ICYMI: HUGE: Ethereum ETFs are finally making waves on Wall Street 💸🌊 [why it’s huge, what’s next + a deep dive into Coinbase & why it’s a bullish indicator]

Risk management remains a critical consideration for institutions. The research highlights that many traditional finance risk management tools, such as value-at-risk models and stress testing, are being adapted for the digital asset space.

Real-time monitoring and advanced analytics are also becoming essential for managing the unique risks associated with digital assets.

✈️ THE TAKEAWAY

What’s next? 🤔 Looking ahead, the projected value of tokenized assets is expected to surpass $10 trillion by 2030, signaling a massive opportunity for growth and innovation. This surge in institutional interest and investment is likely to drive further development of infrastructure, custody solutions, and regulatory frameworks tailored to digital assets.

That said, as institutional adoption increases, we can expect to see greater liquidity in digital asset markets, potentially leading to reduced volatility and increased market efficiency. On top of that, the integration of digital assets into traditional financial systems may accelerate, with more financial products and services incorporating blockchain technology and cryptocurrencies. Zooming out, the next steps in this evolution may include the development of more sophisticated risk management tools specifically designed for digital assets, as well as increased collaboration between traditional financial institutions and crypto-native companies. We may also see a push for global regulatory harmonization to facilitate cross-border transactions and investments in digital assets. All in all, this research yet again suggests that digital assets are on the cusp of becoming a mainstream component of institutional portfolios, potentially reshaping the financial landscape and driving innovation in ways we are only beginning to understand. Bullish.

🔎 What else I’m watching

Revolut Launches Virtual Crypto Payment Cards 💳 Revolut is rolling out dedicated virtual crypto payment cards for everyday spending. Integrated with Apple Pay and Google Pay, these cards allow users to pay in person and online using cryptocurrencies, from big-budget items to daily essentials like commuting and morning coffee. Users can easily set up their cards through the Revolut app and choose which cryptocurrency to spend. Revolut promises no exchange fees on shopping, although 'fair usage fees' may apply depending on the user's premium subscription options. ICYMI: Revolut is aggressively expanding its B2B offerings 💸🚀 [what’s the latest B2B push is all about & why it matters + some bonus dives into Revolut inside]

Danish Family Finance App MyMonii Shuts Down 🚫 Family-focused financial services app MyMonii has shut down after eight years in business. The Danish FinTech offered a parental-controlled Visa credit card and app for setting savings goals for kids and teens aged 7-18. Founder Louise Ferslev cited unit economics as the reason for the closure, stating that the cost of running and scaling MyMonii outweighed the revenue per family. Despite efforts to make the business break even, profitability remained elusive. The shutdown adds to the growing list of smaller FinTech startups struggling to achieve profitability amidst a funding drought.

PayPal Revamps App with Choice Rewards Programme 💳 PayPal PYPL 0.00%↑ is rolling out a new rewards programme and more personalized ways for users to manage their spending. The enhanced rewards include the ability to choose a monthly spending category, such as groceries or clothing, to receive 5% cash back on up to $1,000 per month when using their PayPal Debit MasterCard MA 0.00%↑ . Customers can also stack rewards by saving offers from top brands in the PayPal app. For example, selecting Restaurant as a monthly category can provide 5% cash back, with an additional 10% cash back from a saved DoorDash DASH 0.00%↑ deal. PayPal is also introducing an auto-reload option for setting a balance threshold. Additionally, customers can now add their PayPal Debit Card to Apple Wallet and use it with Apple Pay. ICYMI: Crypto.com and PayPal join forces to streamline crypto purchases 🤝💸 [what it’s all about & why it matters + a bonus deep dive into PayPal]

💸 Following the Money

Oslo-based Cardboard, a software subscription management platform, raised €1.9M in funding from Skyfall Ventures.

Mexican FinTech company Stori has raised $100M in new investment in the South American nation, planning to kick off its operations in Colombia.

Chpter, a Kenyan e-commerce startup, has raised $1.2M in a pre-seed funding round to enhance its technology and expand into Egypt and Nigeria.

👋 That’s it for today! Thank you for reading and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Sundays are worth it because of this - thanks for another great read!