Bill.com, Melio, & Tipalti might have a Revolut Problem, and it’s getting worse 💸; Robinhood targets SEA's retail investors with 2 Indonesian M&As 🇮🇩; Klarna’s secret weapon against Affirm? 👛

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The Ultimate List of Resources about Stablecoins 🪙 [your one-stop resource list for understanding the most disruptive force in global finance]

The Ultimate LLM Toolkit for Unleashing AI Innovation 🤖📚 [100+ battle‑tested tools and frameworks to accelerate your AI projects and stay ahead in the LLM race]

Agents 20: Top AI Agent Startups of 2025 🤖💸 [these AI Agent startups are defining 2025. Find who’s backing them, unlock their exclusive pitch decks, and learn from the best]

Stripe’s Agentic Commerce Suite signals a new era in AI-powered payments 🤖💳 [what it’s all about & why it’s huge, why FinTech giant’s strategy here is brilliant & what to expect next + bonus dive into Stripe’s quest to become the financial backbone of the AI economy & 100+ battle‑tested tools and frameworks to accelerate your AI projects inside]

Gemini’s -60% post-IPO crash: the most asymmetric risk/reward setup in digital assets today? 🤔 [breaking down’t their 3Q 2025 financials, understanding what they mean & what’s next for Gemini + bonus deep dives into Coinbase, Robinhood & eToro inside]

The first true Bitcoin-native public company debuts on NYSE 📈🔔 [what its rocky debut tells us, why it’s interesting & what to expect next + bonus deep dive into Circle and their latest financials]

Mollie seals GoCardless takeover, creating European payments powerhouse to rival Stripe and Adyen 💳🇪🇺 [what it’s all about & why it makes a ton of sense + bonus dive into Stripe’s recent M&A game, and how they want to own the full AI payments stack]

Paradigm plants flag in Latin America with $13.5 million bet on Brazil’s leading real-pegged stablecoin 🇧🇷🪙 [what does it indicate & what can we expect next + bonus deep dive into Circle & the ultimate list of stables resources inside]

The Ultimate List of 790+ Seed Funds 💰 [a curated, data-rich directory built to save you weeks of research and help founders get in front of the right investors, faster]

Inside Asseta AI’s pitch deck: how AI-powered family office startup is targeting the $4B market gap 💰📈 [Family offices control more wealth than Meta and Tesla combined. Most still manage it with Excel and fax machines, so Asseta AI just raised $4.2M to change that]

As for today, here are the 3 fascinating FinTech stories that are changing the world of financial technology as we know it. This was yet another solid week in the financial technology space, so make sure to check all the above stories.

Bill.com, Melio, and Tipalti might have a Revolut Problem, and it’s only getting worse 👀💸

The news 🗞️ FinTech giant Revolut has entered the accounts payable automation market with BillPay, an AI-powered tool that threatens to disrupt established players while potentially adding hundreds of millions in annual revenue to the digital banking giant’s bottom line.

Let’s take a closer look at this.

More on this 👉 Launched in 2024, BillPay automates invoice scanning, data extraction, approval workflows, and payments across more than 150 countries. The product integrates directly with cloud accounting platforms, including QuickBooks, Xero, and FreeAgent, targeting small and mid-market businesses that handle substantial invoice volumes but operate below the complexity threshold of enterprise procurement systems.

Revolut’s strategic positioning centres on cross-border SMEs, digital-first finance teams, and companies managing multi-currency payables. The company is leveraging its existing distribution network of hundreds of thousands of active business customers, with more than 20,000 new businesses onboarding monthly, to drive adoption without the customer acquisition costs that burden standalone AP vendors.

Zoom out 🗞️ The competitive implications could be significant here. SMB-focused AP automation providers such as Bill.com’s smaller business segment, Melio, Plooto, and Stampli face direct overlap with BillPay’s core functionality.

Spend management platforms, including Ramp, Brex, and Airbase must now contend with Revolut’s expanding all-in-one finance proposition. European business neobanks like Wise Business and Qonto, which have historically differentiated on multi-currency accounts and basic payments, risk losing ground as Revolut builds deeper finance automation capabilities.

Our analysts estimate BillPay could generate between $200 million and $400 million in annual revenue at scale, representing a 30-70% uplift on Revolut Business’s current approximately $600 million revenue base. Not too shabby!

This projection accounts for subscription fees, transaction revenue, and the secondary benefits of increased FX volume, card interchange, and deposit balances flowing through Revolut accounts.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, Revolut’s expanded entry signals broader consolidation in SMB financial services, where bundled propositions increasingly outcompete point solutions. The next logical step would be integrating working capital financing or supplier credit directly into BillPay, thus transforming accounts payable data into an underwriting advantage. If that’s the case, this means that for incumbent AP specialists, survival likely depends on either moving upmarket toward enterprise complexity or achieving deeper vertical specialisation that horizontal platforms cannot easily replicate. Looking ahead, the winners in this evolving landscape will be those who recognise that AP automation is no longer just a standalone category but rather a feature within comprehensive business finance ecosystems.

ICYMI: Revolut’s trillion-token reckoning signals a new era of AI Economics in FinTech 🤖📊 [what it’s all about & what it indicates about how FinTechs will be using AI in the future + bonus deep dive into Revolut inside]

Robinhood targets Southeast Asia’s retail investing surge with two Indonesian M&As 💸🇮🇩

The news 🗞️ Robinhood Markets Inc. HOOD 0.00%↑ has just announced its entry into Indonesia through the acquisition of two local financial firms, marking a significant step in the American broker’s global expansion strategy.

The California-based company signed agreements to acquire PT Buana Capital Sekuritas, an established Indonesian brokerage, and PT Pedagang Aset Kripto, a licensed digital asset trading platform.

Let’s take a quick look at this, see why these M&As matter, and what’s next for Robinhood.

More on this 👉 The transactions, expected to close in the first half of 2026 pending regulatory approval from Indonesia’s Financial Services Authority, represent Robinhood’s first major foothold in Southeast Asia.

Financial terms were not disclosed. Robinhood shares rose more than 3% in premarket trading following the announcement.

Zoom out 🔎 Indonesia’s appeal lies in its rapidly expanding investor base. The country now boasts more than 19 million retail stock market investors, a remarkable increase from just 3.8 million five years ago. The crypto market has proven equally dynamic, with 17 million digital asset investors and transaction values reaching approximately $26 billion through October 2025. Notably, more than half of these investors are under the age of 30, aligning closely with Robinhood’s core demographic strength.

Patrick Chan, Robinhood’s Head of Asia, emphasized the strategic rationale, stating that Indonesia represents a fast-growing market ideal for advancing the company’s mission to democratize finance. The firm plans to launch a localized trading application in early 2027, with an initial target of attracting hundreds of thousands of users within its first year of operations.

Pieter Tanuri, the majority owner of both acquired entities and a prominent Indonesian businessman, will remain as a strategic advisor following the transaction’s completion. Robinhood intends to maintain existing Indonesian brokerage services for Buana Capital customers while gradually introducing its proprietary products, including access to U.S. equities and global cryptocurrencies.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, this acquisition signals a broader industry shift toward emerging markets as Western FinTech firms seek growth beyond saturated domestic territories. Robinhood’s dual-track approach - acquiring both traditional brokerage and crypto licenses simultaneously - positions it to capture value across Indonesia’s converging equity and digital asset markets. If successful, this model could serve as a template for expansion into other high-growth Southeast Asian markets such as Vietnam, the Philippines, and Thailand. Looking ahead, Robinhood’s move also underscores the strategic imperative of establishing regulatory-compliant footholds in markets where young, mobile-first populations are rapidly embracing financial technology. Coinbase, your move now! 👀

ICYMI: Robinhood is building the Nasdaq of Reality, where every headline becomes a trade 🤑📈 [why the latest M&A of LedgerX is a masterstroke and how it ties into their bigger vision in the space + bonus deep dive into Robinhood’s latest financials, why I’m bullish & more reads on their biggest competitor Coinbase inside]

Klarna’s secret weapon against Affirm? Wallet partnership with Privy, and further move beyond just BNPL 👛🪙

The news 🗞️ Swedish FinTech giant Klarna KLAR 0.00%↑, which counts 50 million users across 45 countries, just announced a research partnership with Privy to develop a consumer-friendly crypto wallet embedded directly within its app.

This collaboration represents another calculated expansion of Klarna’s ambitions well beyond its Buy Now, Pay Later (BNPL) origins.

Let’s take a quick look at this and understand why it matters.

More on this 👉 Privy, acquired by Stripe (yes, Stripe again 👀) for $230 million in June 2025, provides wallet infrastructure that powers over 100 million accounts across 1,500 developers. The company’s technology eliminates the friction that has historically hindered mainstream crypto adoption by allowing users to authenticate through familiar methods such as email, phone, or social login rather than managing complex seed phrases. This approach directly addresses a persistent barrier: research indicates that 85% of users who connect wallets to decentralized applications abandon the process before completing their first transaction.

The new partnership builds on Klarna’s November launch of KlarnaUSD, a dollar-pegged stablecoin constructed on Stripe’s Tempo blockchain infrastructure.

ICYMI:

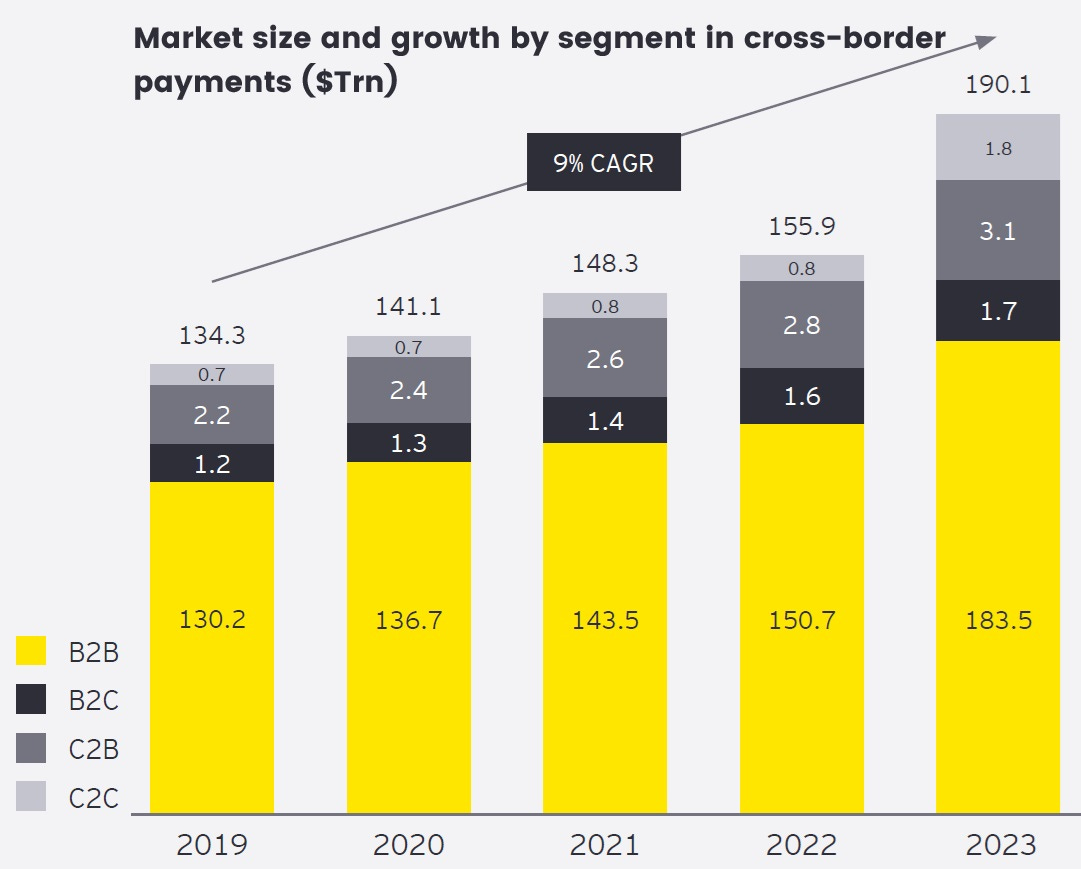

Together, these initiatives position Klarna to capture value in the $194 trillion cross-border payments market, where traditional correspondent banking networks impose fees of 3% to 7%. Stablecoin-based settlements can reduce these costs to under 1%, potentially saving Klarna $1-2 billion annually on international transactions as adoption scales. Not too bad!

Zoom out 🔎 For Klarna’s core business, the integration creates compelling merchant value propositions. Instant stablecoin settlement eliminates the days-long wait for traditional bank transfers, while crypto payments reduce verification failures and chargeback risks.

These improvements alone strengthen the case for Klarna’s premium merchant fees, which have expanded to 2.77% as the company demonstrates measurable conversion and order value increases for retail partners.

THE TAKEAWAY ✈️

What’s next? 🤔 At the core, this partnership better positions Klarna at the intersection of traditional commerce and digital asset payments, a convergence that could reshape competitive dynamics across FinTech. As regulatory frameworks such as MiCA in Europe and U.S. stablecoin legislation provide greater clarity, Klarna’s existing banking licenses offer a compliance advantage that pure crypto companies lack. Looking at the bigger picture, we must note that the broader implications here extend beyond Klarna itself. Competitors, including Affirm and Block will clearly face pressure to develop comparable crypto capabilities or risk differentiation gaps. Meanwhile, traditional payment networks may accelerate their own stablecoin initiatives in response. But if Klarna successfully converts even a modest fraction of its user base into crypto wallet adopters, it could demonstrate the viability of embedded digital asset services for mainstream consumers, thus potentially catalyzing similar integrations across the financial services industry. Crypto is here to stay, folks.

ICYMI: Klarna wants to challenge premium credit card giants with a debt-free membership model 🤔💳 [can it really challenge AmEx Platinum & Chase Sapphire Reserve with a debt-free membership model, why it matters + bonus deep dive into Klarna inside]

The Honest Network effect, or why Affirm’s data moat is worth $50 billion 🤑📊 [breaking down BNPL leader’s latest financials, understanding what they mean & why you should be bullish on AFRM 0.00%↑]

🔎 What else I’m watching

Kalshi Secures Temporary Relief in Connecticut 🏛️ Kalshi has secured a temporary pause on enforcement actions from Connecticut regulators. The company argues that its event-based contracts are regulated derivatives, not illegal gambling. The court has set a schedule for further proceedings, with oral arguments expected in mid-February. This is part of a broader legal battle Kalshi is facing in several states. ICYMI: From $5 billion to $11 billion in 60 days: inside the most aggressive valuation jump in FinTech history 🤯📈 [latest $1 billion fundraise & what it indicates, what to expect next + bonus deep dive into Robinhood and how it’s building the Nasdaq of Reality]

BNY Enhances AI Platform with Google Cloud 🤖 BNY has integrated its AI platform Eliza with Google Cloud’s Gemini model to enhance market analysis and automate routine tasks. This collaboration aims to combine BNY’s financial expertise with advanced AI capabilities, with nearly all BNY employees trained in AI and over 110 AI solutions in production. ICYMI:

Axyon AI Launches Agentic AI Platform for Thematic Investing 📈 Axyon AI has launched Axyon Foresight, an Agentic AI platform that streamlines the thematic investing process by combining human insight with AI. The platform reduces the time required to create thematic investment products from months to hours and uses a systematic methodology to minimize bias. Demonstrated with use cases on Post-War Ukraine Development and US tax reform, Axyon Foresight enhances investment strategies with advanced AI. ICYMI:

💸 Following the Money

Blackstone and EQT-backed Dutch payments group Mollie has agreed to acquire the UK FinTech GoCardless for €1.1B. The deal is more than 90% composed of stock and a small cash component. ICYMI: Mollie seals GoCardless takeover, creating European payments powerhouse to rival Stripe and Adyen 💳🇪🇺 [what it’s all about & why it makes a ton of sense + bonus dive into Stripe’s recent M&A game, and how they want to own the full AI payments stack]

Struggling French payment firm Worldline is to offload its Swedish payments orchestration business CoreOrchestration to Incore Invest in an all-cash transaction valued at €160M.

AI-powered credit intelligence platform AIR has raised $6.1M in a seed funding round co-led by Work-Bench Ventures and Lerer Hippeau.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

This is great - thanks!