Starling Bank’s 2026 financials: 2.5x Monzo’s profit on half the revenue, and a £70M SaaS pipeline that changes the IPO math 📈🧠; Your next broker is a chatbot 🤑🤖

FinTech is Eating the World, 27 May

Hey Everyone,

Good morning & happy Wednesday! Today we’re diving deep into another British digital banking gem Starling Bank, which just published its 2026 annual report (unpacking the most important financial facts & figures, how it stacks against Monzo & Revolut, & why Starling’s balance sheet is a fortress + bonus deep dives into the latest financials of Monzo & Revolut inside), and why your next broker and investment advisor could be Claude AI or ChatGPT (what Liquid Co-Invest is all about, why it’s interesting & what it tells us about the future of agentic finance + bonus dive into how this perfectly fits the AI products Anthropic itself told founders to build in 2026 & the full Claude Playbook for Finance inside). So let’s jump straight into the good stuff 🌶️

Starling Bank’s 2026 financials: 2.5x Monzo’s profit on half the revenue, and a £70M SaaS pipeline that changes the IPO math 📈🧠

Following the money 💸 All three biggest UK neobanks finally published their annual results, with two of them within days of each other. The headlines wrote themselves: Revolut posted £1.7 billion in pre-tax profit on £4.5 billion in revenue. Monzo crossed £1.7 billion in revenue and added 3 million customers. Starling’s revenue fell 5.6% 🤕

Starling clearly lost the headline war. But it may have won everything else.

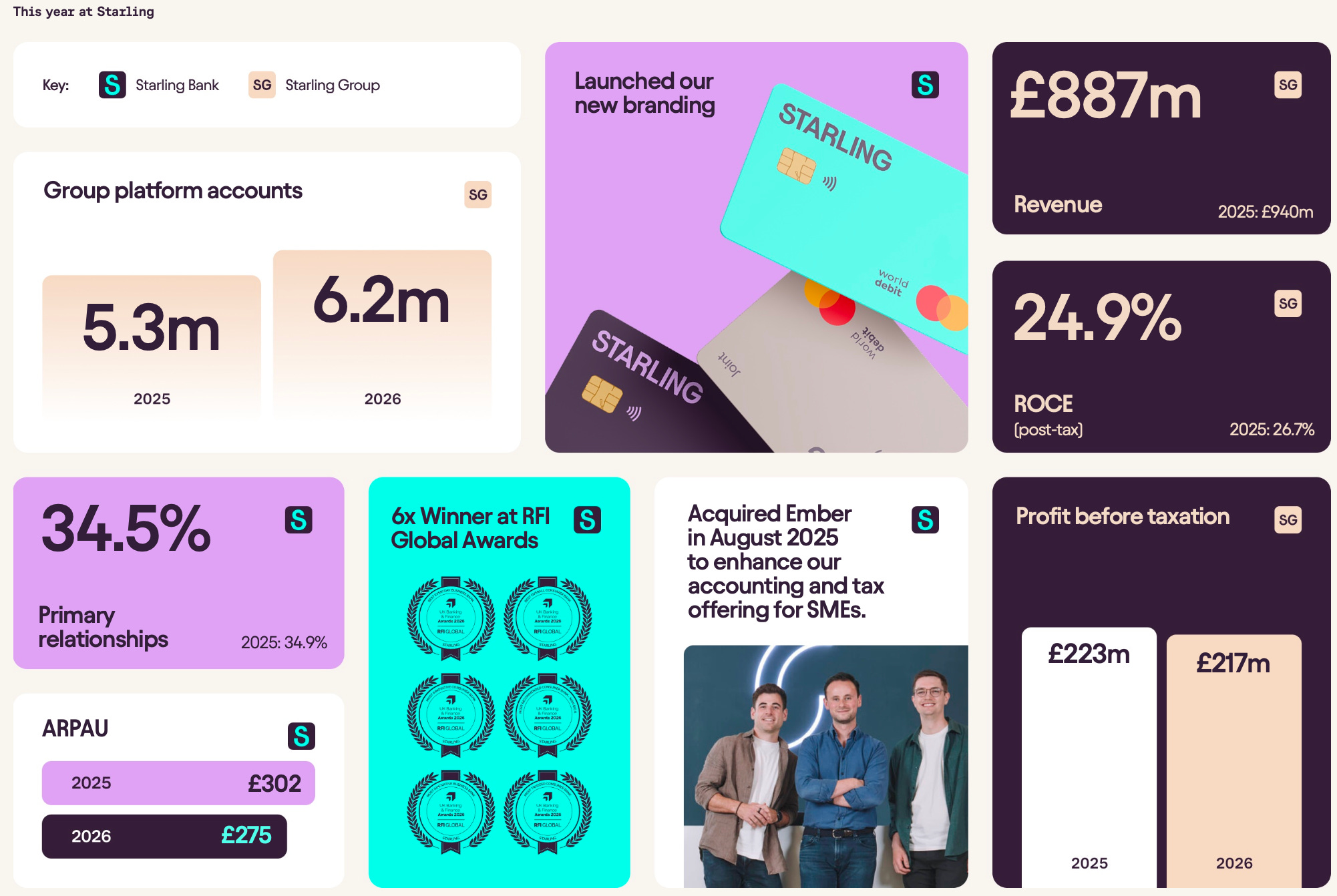

On £887M in revenue, Starling produced £217M in statutory profit, a 24.5% PBT margin. Monzo, on nearly double the revenue, managed £87M, a margin of roughly 5%. Revolut is in a different category entirely: a global fee-income platform serving now over 70 million customers across 39 countries, barely lending at all. Starling is thus the only one of the three that looks like an actual bank, lends like an actual bank, and earns like the best of them 🏦

But the number that should change how you think about Starling isn’t in the P&L. It’s buried in the platform business.

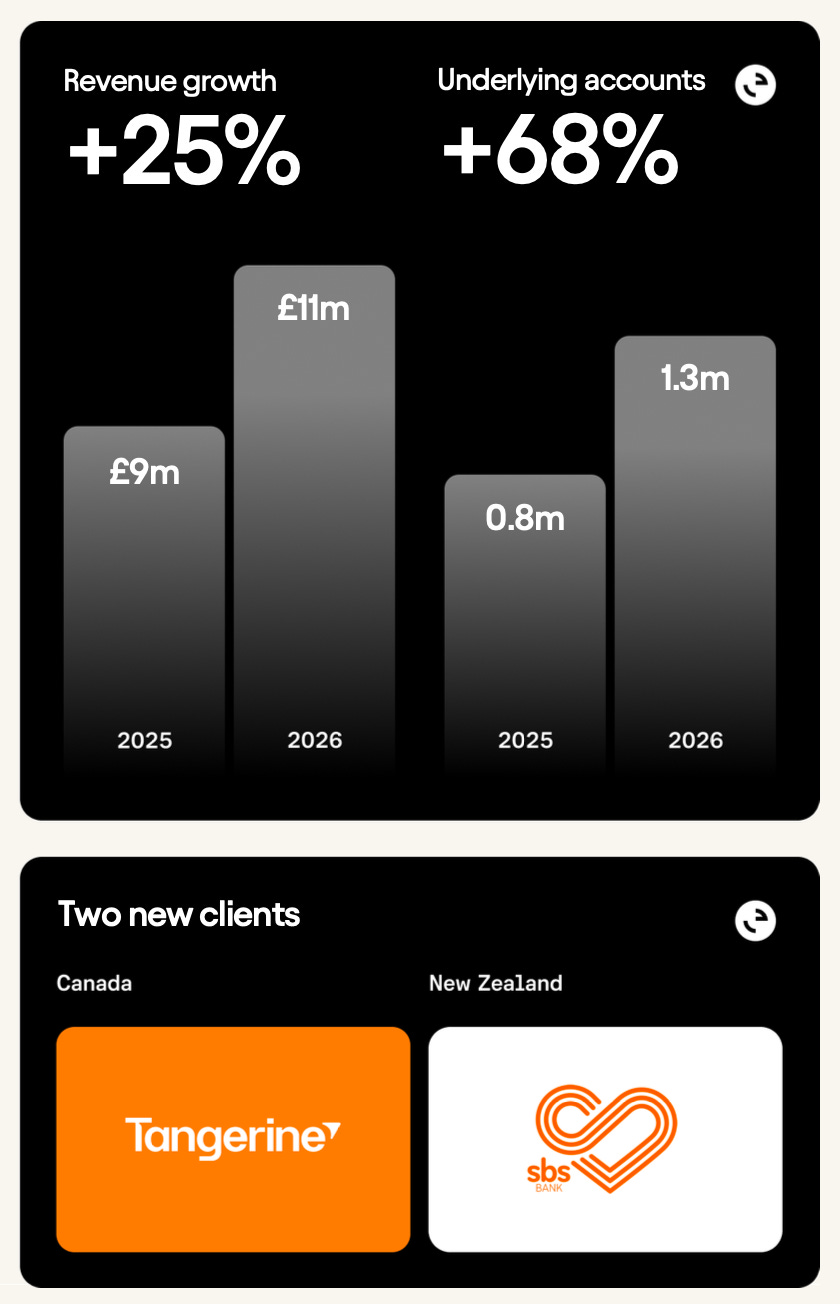

Engine, Starling’s SaaS banking-as-a-service arm, generated just £10.9M in revenue last year. Rounding error. Except it now has £70M in committed annual recurring revenue, four live clients across five countries, and a single partnership (Tangerine, a Scotiabank subsidiary) that alone will migrate over 2 million accounts onto the platform over the next decade. If Engine scales to £100M in ARR, a 10x revenue multiple on that segment alone could add £1B or more to Starling’s IPO valuation, nearly matching its entire equity book value today. Not too shabby!

That makes Starling two businesses stitched together inside one balance sheet: a high-margin UK bank with a £525M capital surplus, and a nascent fintech infrastructure company with global reach and zero balance-sheet consumption. The market will eventually have to price both. It hasn’t done so yet.

So let’s dive deeper here and unpack the full financial picture: the Monzo and Revolut comparisons in detail, why Starling’s balance sheet is a fortress (and why Monzo’s lending book tells a very different credit story), how Engine’s pipeline and committed ARR stack up against the valuation math, what the FCA restrictions still in place mean for the growth re-acceleration thesis, and the specific entry price at which the risk/reward turns decisively in Starling’s favour ahead of a likely 2027–2028 IPO.