Monzo’s 2026 financials: the £1.7B revenue machine that still has to prove it can escape the UK’s Orbit 🏦🇬🇧; Catena Labs wants a bank charter for AI Agents, and the OCC said “We’ll Listen” 🏦🤖

FinTech is Eating the World, 26 May

Hey Everyone,

Good morning & happy Tuesday! Today we’re diving deep into British neobanking gem Monzo, which just published its 2026 annual report (breaking down the unit economics that matter, the Revolut comparison investors keep getting wrong, the governance drama, IPO chances & what’s next for Monzo + bonus deep dive into Revolut’s latest financials & their foundational AI model for money inside), and Catena Labs that wants a bank charter for AI Agents (what they are trying to do, why it’s worth paying attention & how Catena stacks agents other players in agentic finance space + bonus deep dive into Google’s bid to become the OS for all e-commerce, Circle’s Agent Stack play, and a full guide on how to build an AI Agent from sractch inside). So let’s jump straight into the interesting stuff 🌶️

Monzo’s 2026 financials: the £1.7 billion revenue machine that still has to prove it can escape the UK’s Orbit 🏦🇬🇧

Following the money 💸 Monzo Bank makes more money per customer than Revolut. That sentence would have been unthinkable two years ago. But recently dropped 2026 annual report confirmed it: Monzo now generates £167 in revenue per active personal customer, while Revolut generates £66. The gap is the difference between a primary bank 🏦 and a multi-currency spending card 💳, and it’s the number that will anchor every IPO conversation Monzo has this year.

The headline figures are definitely strong.

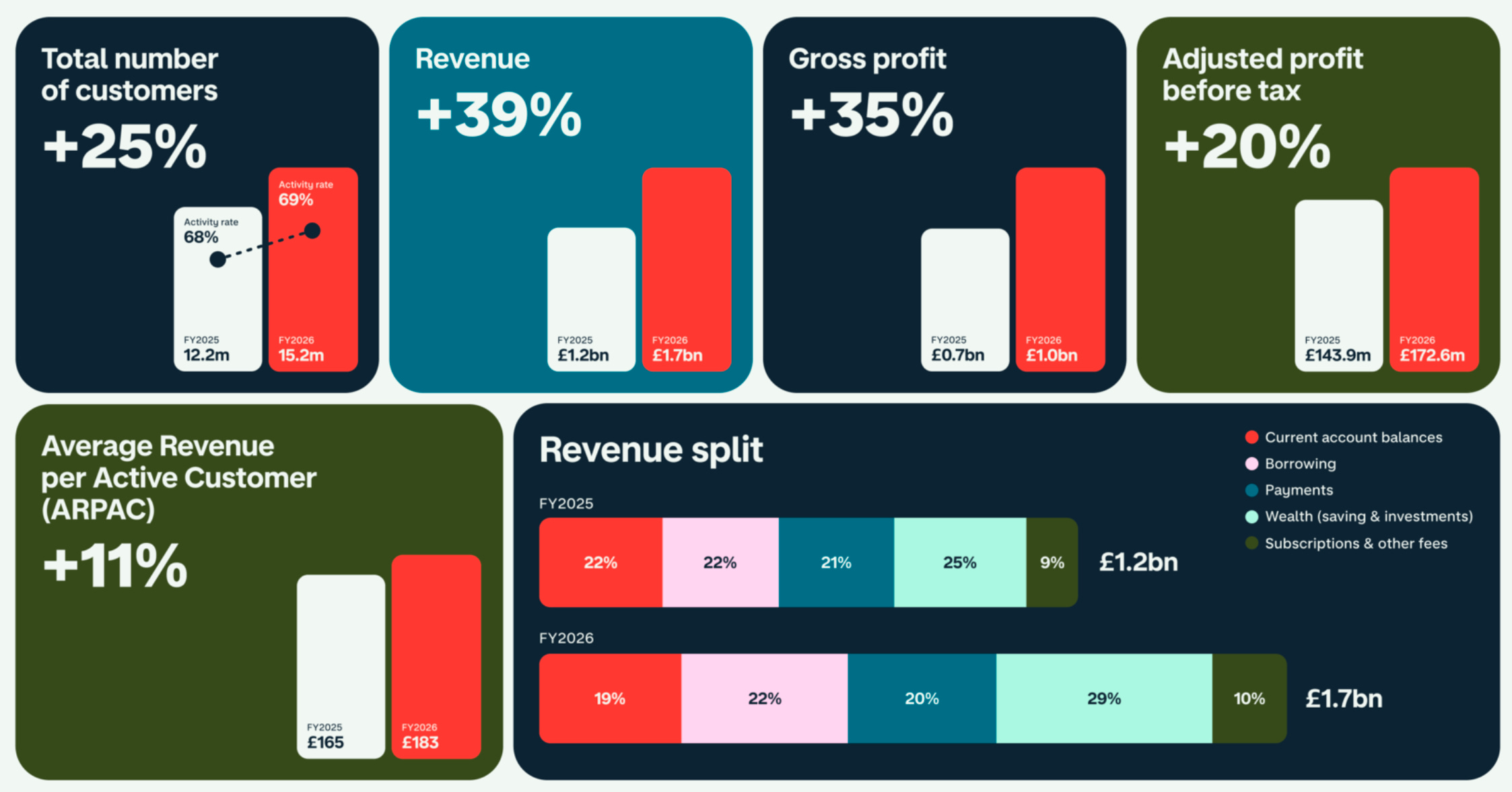

Revenue surged 39% year-on-year to £1.71B.

Gross profit broke £1B for the first time.

Statutory pre-tax profit hit £87.3M (up 44%), or £172.6M adjusted for an FCA fine and restructuring charges. Three consecutive years in the black.

A customer base of 15.2M, with one in five UK adults now banking with Monzo.

Deposits up 55% to £25.7B. Four revenue streams each clearing £300M, up from one a year ago.

By every growth metric, this is a neobank that has crossed into proper banking territory.

Yet, the investment case isn’t about what Monzo has done. It’s about what happens next, and that’s where the picture gets complicated.

The board pushed out its previous CEO partly over frustration with the company’s UK concentration. His replacement, Diana Layfield, exited the US within weeks of taking charge and is betting the company’s next phase on European markets where Revolut already has a decade-long head start and millions of entrenched customers. Monzo’s statutory profit margin is 5.1%. Revolut’s is 38%. The CET1 ratio fell from 56% to 33% in a single year. And Layfield has told the FT she’s “not in a hurry” to IPO, which is either confidence or a warning that the timeline is longer than the market expects.

So let’s dive deeper and break down the unit economics that matter, the Revolut comparison investors keep getting wrong, the governance drama behind the CEO transition, and where the valuation range of £6-10 billion starts to look either like a bargain or a stretch. The answer depends on a single question: can Monzo replicate in Dublin and Barcelona what it built organically in London?