𝕏 Money just launched with 6% APY and a Visa Card. Stripe, Apple Pay, and your bank have a problem 😳💳; SoFi’s Q1 2026: the Everything App is becoming an everything earner 📱💸

FinTech is Eating the World, 30 June

Hey Everyone,

Good morning & happy Tuesday! Today, we’re diving into 𝕏 Money, which just launched with 6% APY (what it’s all about, how it ties with 𝕏 Super App play & why Stripe, Apple Pay, and your bank have a problem + bonus deep dive into SpaceX, which is an all ecompassing Elon’s ecosystem & The Founder’s Playbook for Winning in the AI Age inside), and SoFi, the Everything App that’s finally becoming an everything earner (deep dive into SoFi’s Q1 2026, breaking the most importat financial facts & figures to see if it’s worth your time and money + bonus deep dives into Robinhood & Coinbase inside). So let’s just jump straight into the good stuff 🌶️

𝕏 Money just launched with 6% APY and a Visa Card. Stripe, Apple Pay, and your bank have a problem 😳💳

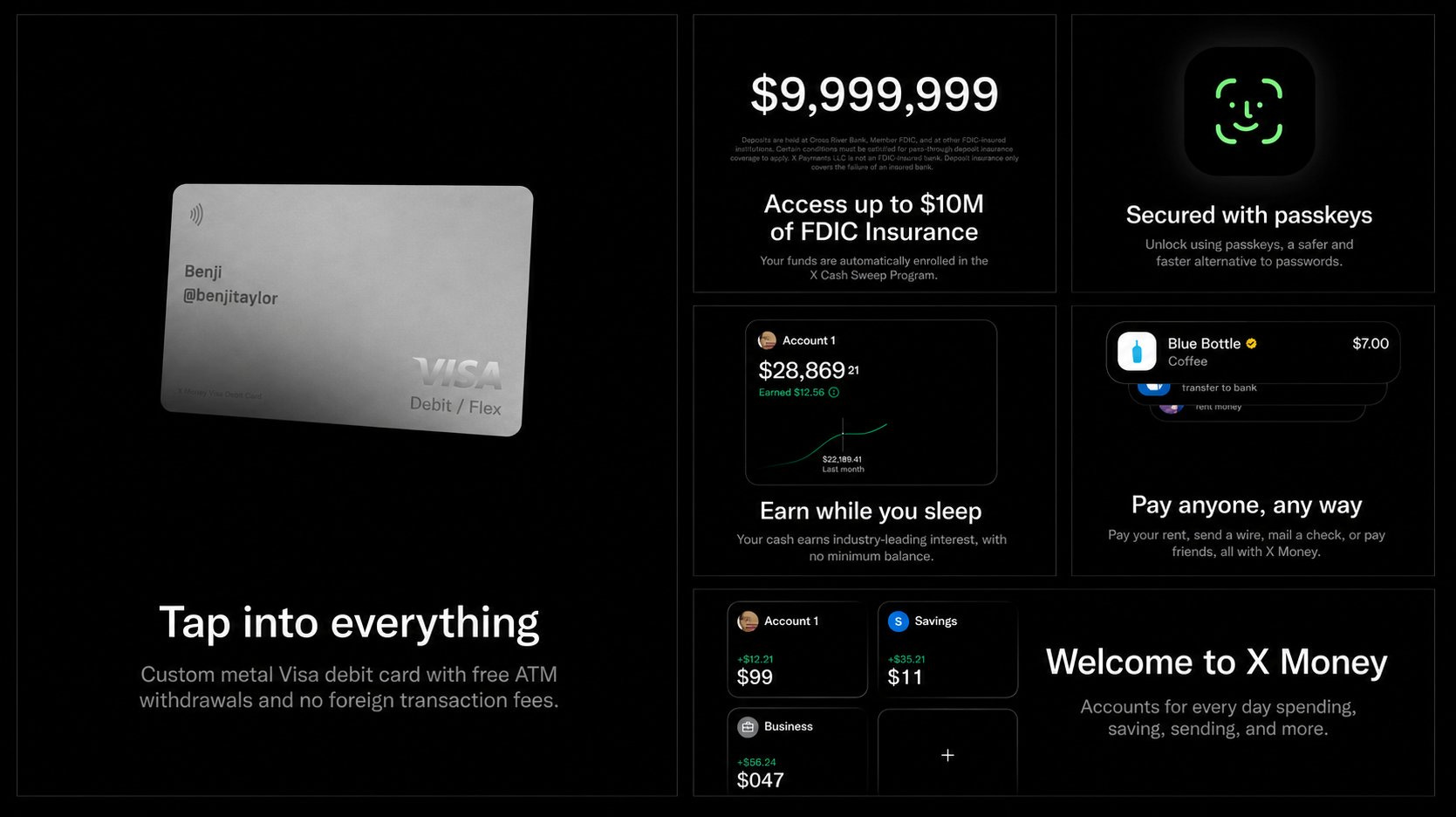

The BIG News 🔥 Elon Musk just turned 600 million timelines into bank branches, and the economics make more sense than they look at first glance.

𝕏 Money went live late last week with a 6% APY on cash balances, a metal Visa debit card, instant peer-to-peer transfers, and FDIC insurance up to $10 million.

The yield alone beats every high-yield savings account in the U.S. But the yield is the distraction, not the strategy.

What happens when a platform with 600 million users and near-zero customer acquisition costs decides it doesn’t need to profit from your deposits the way JPMorgan or Goldman does?

Stripe can’t match those economics. Neither can any neobank on the market.

Let’s take a closer look at this, break down the economics behind the 6%, and what 𝕏 Money’s launch means for Visa, Stripe, Apple Pay, and every bank in America.