Here’s your gentle reminder that the Future of Finance is Embedded 🔗; Macro conditions & improving regulatory clarity are accelerating FinTech M&As 💸

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Top 100 VCs in the US & 70+ Investors and Funds Investing in Female Founders 🚀 [use this to find investors who align with your mission 🎯]

Tesla could become the most powerful AI company in the world. Here’s how it will disrupt Finance & FinTech forever 🚘💸

The foray into wealth is finally here: Monzo launches investments 💸 [a deeper dive unpacking this pivotal move for Monzo + more bonus reads]

The death of Binance US might not be exaggerated after all… 👀

The state of European FinTech in 2023 🇪🇺💰 [key takeaways from the fresh report + priceless resources to execute your strategy]

As for today, here are the 2 fascinating FinTech stories that were transforming the world of finance as we know it. This week was just wild in the financial technology space, so make sure to check all the above stories.

Here’s your gentle reminder that the Future of Finance is Embedded 🔗

The news 🗞️ Despite a very tough FinTech funding environment, French banking-as-a-service (BaaS) platform Swan has secured a €37 million equity raise in a funding round led by Lakestar.

This new funding round follows Swan’s €16M Series A led by Accel in 2021 and a €5M Seed round in 2020.

This piece of news isn’t about Swan per se. It’s about the future of finance, which is embedded.

Let’s take a look.

More on this 👉 Founded in 2019, Swan is an embedded finance platform that provides a complete toolkit to begin offering banking services such as issuing wallets, cards, and international bank account numbers with a simple API and a few lines of code.

Its co-founder & CEO Nico Benady previously co-founded two other payments startups, Limonetik and Antelop.

The USP 🥊 Swan company now has over 100 customers with product coverage across 30 European countries and has processed over €7 billion worth of transactions.

It already works with large, multi-national organizations such as Carrefour, which completed a successful cashback project in the past year and will deepen its enterprise capabilities by launching new product lines tailored for larger organizations.

Zoom out 🔎 But this isn’t about Swan. This serves as another good reminder that the future of finance is embedded.

Let’s do a brief recap of the key drivers here and what are the implications for the future.

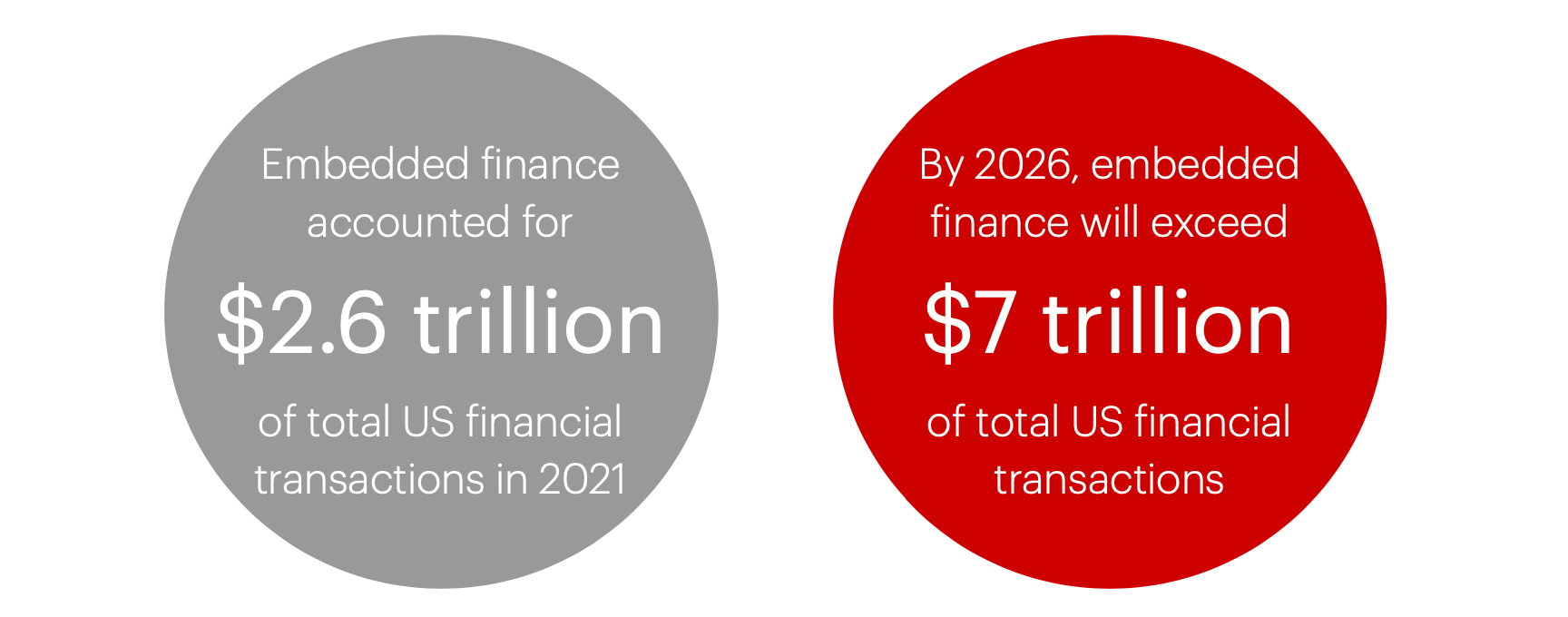

If you’re an active reader of my newsletter, you know that embedded finance is emerging as a massive disruptor of the financial services industry.

By integrating (aka embedding) financial services into non-financial platforms and applications, embedded finance delivers unparalleled convenience, personalization, and accessibility of banking, payments, insurance, and other offerings. All within your beloved app or service.

Therefore, it is believed that this model will explode over the next decade. Some estimates put the value of embedded finance reaching over $7 trillion by 2030. And that’s only in the US:

So what’s driving this? There are 3 main accelerants:

Consumer demand for frictionless financial experiences. People now expect to seamlessly access lending, insurance, and payments without leaving their preferred apps and websites.

Business benefits of revenue diversification and loyalty. Non-financial companies from retailers (a case in point could be Carrefour) to mobility providers (Uber does this well) can tap into the embedded finance “secret sauce” to generate new revenue streams, boost customer lifetime value, and differentiate their platforms.

Accelerating pace of financial APIs and cloud technologies. The enabling infrastructure to rapidly embed modular financial services into digital experiences is falling into place.

As a result, embedded finance has permeated our everyday lives, often without us realizing it. Today, any company has the power to become a FinTech company.

And that’s exactly how FinTech is eating the world.

✈️ THE TAKEAWAY

Looking ahead 👀 Given the trends and value to be unlocked is clear, we must also understand the future implication. And they are twofold. When it comes to banks or FinServ incumbents, they must reinvent themselves to remain relevant, either by moving up the value chain or leveraging partnerships to participate in the new embedded ecosystems. Looking at the big picture, SMEs are the ones that stand to gain tremendously from embedded finance. Especially business financial services like payroll APIs, invoicing, AR/AP automation, and lending. By integrating these offerings into their management platforms, small businesses can save time, smooth operations, and fuel growth. Hence, while regulatory compliance will continue to evolve around embedded finance and the broader FinTech space, its explosive growth is now inevitable. And as consumers, we’ll soon forget what it was like to access financial services through any channel but our favorite apps and sites. Because the future of finance is frictionless, invisible, and everywhere.

ICYMI: Embedded finance is a $242B opportunity in APAC by 2025 😳 [+5 more reads]

Who does this well? Definitely Adyen & AmEx:

Adyen just became a bank in the UK 🇬🇧🏦 [+ a deep dive into the FinTech giant]

American Express is doing a fantastic job with Embedded Finance 👏 [& how it’s building B2B payments powerhouse]

Also, ICYMI: FinTech M&A doesn’t stop: FIS buys embedded finance startup Bond 🤯

Macro conditions & improving regulatory clarity are accelerating FinTech M&As 💸

The deals 🤝 As expected, the FinTech industry is seeing an acceleration in mergers and acquisitions (M&As). This week again we had two interesting M&As during the same day.

Let’s take a closer look at them and what they mean.

More on this 👉 In the prepaid payments sector, Netherlands-based Recharge expanded its global leadership through the acquisition of Startselect, a digital gift card and gaming company. This strengthens Recharge's diversified product portfolio and extends its network of digital marketplaces.

Recharge aims to complete 2-3 more acquisitions by the end of 2024 to consolidate the digital prepaid card market. I bet they are not the only ones given the potential is massive here…

In the crypto accounting vertical, US-based Bitwave acquired Gilded to enhance its enterprise solutions for crypto payments, invoicing, tax tracking, and bookkeeping. The deal comes amid new US accounting rules for digital assets from the Financial Accounting Standards Board. Bitwave views crypto payments as the future given instant settlement and low fees. Pss, stablecoins, anyone?

ICYMI: Game-changer: Visa just expanded stablecoin settlement capabilities 😳 [a closer look at this pivotal move + more bonus reads]

The improved regulatory clarity is expected to spur the adoption of digital asset solutions. Given the current funding environment and macro conditions, this should also lead to more M&As in the space.

✈️ THE TAKEAWAY

What’s next? 🤔 These deals yet again highlight the accelerating consolidation in the broader FinTech space as companies capitalize on macro conditions and regulatory improvements to augment capabilities and competitive positioning through M&As. Key drivers here are obviously the pursuit of scale, product expansion into new markets, and staying ahead of impending regulatory-driven market shifts. On top of that, some verticals (especially in crypto & Web3) have just too many players doing the same thing, so further consolidation is just a matter of time.

The critical point here is to get the M&A right. And it’s all about the numbers. Use these to not miss a thing:

🔎 What else I’m watching

JPM’s token 👀 Banking heavyweight JPMorgan Chase JPM 0.00%↑ is looking into the use of a blockchain-based digital deposit token as a way of making cross-border payments and settlement faster, according to Blomberg. The bank has already built most of the infrastructure needed for the project but will not create the actual token unless it gets the go-ahead from US regulators, says Bloomberg, citing a source. JPMorgan has been using a digital token, called JPM Coin, for several years, enabling corporate clients to move funds in dollars and euros from their different accounts within the bank. However, the new offering could be used to send money to clients of other banks, says Bloomberg. It could also be used to settle trades of tokenized securities. ICYMI: JPMorgan increases stake in Brazil’s C6 as it aims to tap into one of the world’s largest retail banking markets 🏦 [+ lots and lots of bonus dives into JPM]

Square says SORRY 👀 Block’s merchant business Square apologized to its customers this week after a lengthy outage last week left its seller clients unable to process consumer payments. During an outage, Square sellers were unable to access their accounts or process payments while the outage occurred, the company said in posts on social media website X, formerly known as Twitter. Some Square merchants expressed frustration over the company’s handling of the situation and that they learned of the outage on X. “We apologize for letting you down and for the length of time it took for us to get our systems back up and running,” Square said in a post on its website. “We know this situation was made more difficult by our communication frequency and the delayed support response some of you experienced.” Square, you can do better. ICYMI: Square suffers a major outage 🫣

Wix + Stripe📱Israel-based Wix WIX 0.00%↑ has partnered with Stripe to launch Tap to Pay on Android and simplify in-person commerce for US-based merchants. This development aims to simplify in-person commercial transactions for merchants based in the United States, and it builds upon the previous launch of 'Tap to Pay on iPhone. Wix now allows its merchants to securely accept contactless payments directly through their Android devices, eliminating the need for additional hardware. ICYMI: Wix continues pushing for unified commerce 👛

💸 Following the Money

Indian B2B SaaS fintech Perfios has secured $229M in Series D funding from private equity investor Kedaara Capital. Headquartered in Bangalore, Perfios works with over 1000 financial institutions, helping them with their origination, onboarding, decisioning, underwriting, and monitoring processes.

B2B BNPL service for suppliers Treyd drummed up a $12M Series A extension to bring its total round to $25M.

France-based Treasury Management fintech Fipto has raised EUR 15M in a seed funding round led by Serena and Motier Ventures. The Fipto platform is designed to facilitate corporate treasury management and international payments, encompassing both fiat and digital currencies through the utilization of blockchain technology.

👋 That’s it for today! Thank you for reading and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up: