Silicon Valley Bank becomes First Citizens 🏦; Apple Pay Later is finally live 🍎💳; Revealed: once flirting with unicorns, Railsr was sold at a 99.8% discount 🤯

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Biometric payments is a $6T opportunity, & JPMorgan is going after it 😳 [why it matters + a bonus into why JPM is the Microsoft of Banking]

FinTech M&A is still alive as Mastercard and Visa eye $1 billion deal for Brazil's Pismo 🤑

Impact-as-a-Service 👀 [this one is very interesting!]

As for today, here are the 3 FinTech stories that were literally changing the world as we know it. This week was yet another super hot week in FinTech, so make sure to check all the above stories.

Silicon Valley Bank becomes First Citizens 🏦

SVB 👉 First Citizens 🏦 First Citizens Bank, one of the largest regional banks in the US, has acquired large pieces of Silicon Valley Bank more than 2 weeks after the lender’s collapse sent the whole banking system shaking, WSJ reported.

Get up to speed: The rise and fall of Silicon Valley Bank 🏦

More on this 👉 Founded in 1898, First Citizens was the 30th-largest US bank last year. The SVB acquisition will put the lender in the top 25 US banks in terms of assets. Here’s the deal in a nutshell:

First Citizens is acquiring all of Silicon Valley Bank’s deposits, loans, and branches. All of them will open this week under the new ownership.

The purchase includes $56.5 billion in deposits and about $72 billion of SVB’s loans at a discount of $16.5 billion. Some $90 billion of SVB’s securities will remain in receivership.

The FDIC agreed to share any of First Citizens’ losses or potential gains on SVB’s commercial loans.

On top of the loss-sharing agreement, the FDIC will help finance the deal with a 5-year, $35 billion loan. The agency also is providing a $70 billion line of credit to help cover potential deposit flight.

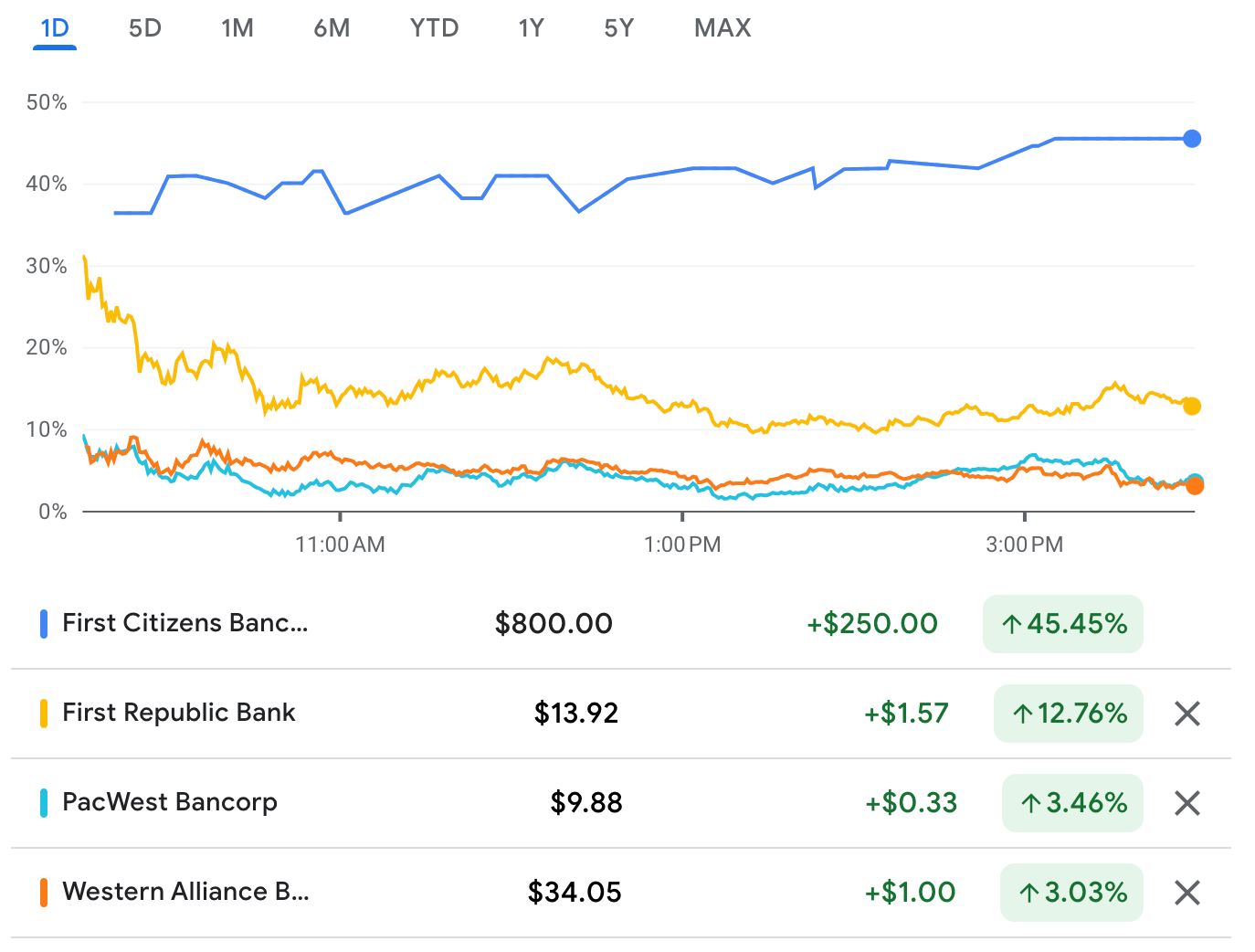

Positive vibes 📈 The markets celebrated the move big time. Shares of First Citizens surged more than 40% shortly after the opening of trading Monday. Shares of other regional banks including First Republic Bank, PacWest Bancorp, and Western Alliance Bancorp were also higher.

This development is important for two main reasons and two levels - micro and macro.

Building up 👛 On a micro level, we must note that this is First Citizens’ 38th acquisition.

This goes on to show that most banks we are familiar with today are actually 10s or 100s of banks rolled up as one. Also, it probably explains why and how the bank managed to survive and thrive for more than a century.

Expect to see more consolidation if the macro environment doesn’t improve.

Macro 📊 The macro side of things is obviously much more important here. What it shows is the willingness and efforts by the regulators to clean up all the mess after two of the largest bank failures in history that happened in the same week (this is SVB and Signature). This milestone comes at a time when investors are on edge about the health of the global financial system.

More importantly, while it might have started in the US, this is a global phenomenon. Just one week ago, swiss officials engineered a takeover of the troubled Credit Suisse Group by its rival UBS.

Reread: Shotgun wedding: UBS buys Credit Suisse for $3.2 billion 🤯

✈️ THE TAKEAWAY

What’s next? 🤔 The FDIC estimated the failure of SVB will cost a federal insurance fund it oversees about $20 billion, or roughly 10% of the bank’s assets before its failure. Probably a small price to pay for the health of the global financial system. Zooming out, we must note that SVB’s implosion marks the biggest test to date of the post-financial-crisis regulatory architecture designed to force banks to curtail risk and monitor it more closely. While the contagion has been stopped (at least for now), it’s yet to be seen how strong the system really is.

Apple Pay Later is finally live 🍎💳

The launch 🚀 Apple AAPL 1.61%↑ has finally launched Apple Pay Later - its Buy Now, Pay Later (BNPL) service - in the US, enabling users to split purchases into 4 equal payments.

More on this 👉 First announced last June, Apple Pay Later is now open to select users in a pre-release version, with a full rollout set for the coming months. Here’s it in a nutshell:

Users apply for loans of $50 to $1000, which can be used for online and in-app purchases made on iPhone and iPad with merchants that accept Apple Pay. A soft credit pull is done during the application process with no impact on the user's credit.

Repayments are made in 4 equal installments, spread over 6 weeks with no interest and no fees. Users track, manage, and repay their Apple Pay Later loans in one location in Apple Wallet.

While Apple is working with Goldman Sachs GS 1.12%↑ and Mastercard MA 0.70%↑ on the service, it has set up a wholly-owned subsidiary, Apple Financing, to offer loans directly.

Apple is also handling credit checks for the service in-house. Last year, it acquired the UK credit bureau Credit Kudos, which uses open banking technology to deliver finely-tuned credit scores.

Why it matters? 🤔 This move could not only be the next big thing for Apple and a serious contender in the burgeoning BNPL market. More importantly, it’s a Step 0 to the Apple Bank. Here’s the takeaway + a deep dive into Apple Bank's strategy:

✈️ THE TAKEAWAY

The last mover advantage 👏 Apple Pay is estimated to have more than 500M users globally. Being in so many people’s pockets, it doesn’t make sense NOT to follow where the money is. And currently, lots of money is (still) flowing into BNPL as people simply like the proposition better (vs. credit cards). The Apple strategy here is super simple - it’s all about the numbers. Apple currently earns a % of every Apple Pay purchase, so the more users buy, the more money it makes. BNPL service (although free in essence) could lead Apple users to make more big-ticket purchases hassle-free and within the same ecosystem. Think about iPhones, PCs, and upcoming VR/AR headsets and (maybe) even Apple Car 🚘 Having said that, irrespective of how you look at it, it’s not good news for standalone BNPL businesses. Looking further, given that Apple will be actually financing this from their own balance sheet, that’s basically step 0 to the Apple Bank. And that could be massive and change FinTech as we know it 🤯

Bonus: Welcome to Apple Bank - your everyday Banking from Apple, NOT a Bank 🍎🏦 [+3 bonus reads]

Apple takes another step towards becoming a bank 🍏🏦

Reread again why BNPL will continue to grow:

Revealed: once flirting with unicorns, Railsr was sold at a 99.8% discount 🤯

Fresh news🔥 I have earlier covered that UK’s Railsr, once a very promising embedded finance platform, was on the brink of collapse yet managed to reach a rescue deal with a consortium of investors led by D Squared Capital. The terms of the deal were undisclosed.

It seems that we now have some spicy news.

More on this 👉 Sifted has just reported that according to the new documents that were recently revealed, the Railsr deal was worth just £413,904 😬 That’s an eye-watering 99.8% discount on the $250M valuation Railsr was assigned when it completed a down-round in October last year, as per Sifted. Damn 😳

✈️ THE TAKEAWAY

That’s bad 😳 If this information is accurate, it’s very very bad. It yet again shows that despite all the potential and growth opportunities, Railsr was a very poorly run company that neither did manage risk properly, but it seemingly ignored regulator compliance too. Disappointing. Hopefully, it serves as a valuable lesson to everyone else in the market.

Remember: Railsr is going off track and to the wall 🛤 🧱

🔎 What else I’m watching

Industry moves 💼 Zero Hash, a crypto infrastructure provider that helps companies integrate crypto, has appointed longtime crypto leader Cyril Mathew as its new President and COO as the company looks to expand and grow internationally, CoinDesk reported. A former big-tech developer, Cyril has led teams in business development at Coinbase as well as Meta Platforms (formerly Facebook) and Uber. Most recently, he was the global head of business development and partnerships at payments processor Stripe. As someone who knows Cyril personally, this is a massive win for Zero Hash - congrats 👏

More cuts ✂️ Prolific Web3 investor Animoca Brands has cut the target for its web3 fund. Again. That's according to a Reuters report citing people familiar with the matter that said it's now targeting $800M for its metaverse fund — a 20% cut from its previous $1 billion. We can remember that in November founder Yat Siu told Nikkei that Animoca would target $2 billion for the fund, which plans to target mid- to late-stage startups in Web3. Winter is really here ❄️

Crypto heaven?🇫🇷 The US-based fast-food chain Burger King has begun accepting crypto payments at one of its Paris locations, thanks to Alchemy Pay and Binance Pay. The service will use the Instapower power bank top-up service. Users and customers of the French capital’s fast-food chain will be able to pay with cryptocurrency through power bank devices. Instapower’s new solution is currently used in Asia, while Europe only now seems to be beginning to embrace the idea, the partnership with Burger King in Paris being one example. It seems that Paris is crypto’s newest hotspot 😳

💸 Following the Money

Raisin, a fintech offering a savings marketplace across Europe, has raised €60M in a Series E funding round. The new round represents Raisin's first return to fundraising for four years after it landed €142M in 2019.

Cross-border payments company Thunes has raised $30M in an ongoing investment round. In a filing with Singapore's Accounting and Corporate Regulation Authority, the firm said that one of its engaged investors, Marshall Wace had so far committed $30 million in the round.

Wannabe web3 middleware platform Particle Network raised $7M to create services to support Web3 developers.

👋 That’s it for today! Thank you for reading and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up: