Stripe turned its workforce into AI Product Lab 🤖🧪; Anthropic just entered RegTech: Claude wants to be the Compliance Layer 😳🤖; Circle Agent Stack is actually Circle's escape plan 💸🪙

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Anthropic Just Told AI Founders Exactly What to Build in 2026 🦄 [1 million conversations. 9 consumer AI domains. A full founder playbook - plus where Anthropic’s own products will and won’t compete]

Claude Opus 4.7: The Complete Prompting Playbook 🧠 [How to unlock the full intelligence of Anthropic’s most capable generally available model - with 10 ready-to-use Mega Prompts engineered for the way builders and investors actually work]

He Got Fired From OpenAI at 22. Then He Turned $225M Into $5.5B by Betting on the AI Infrastructure No One Else Was Watching 💸 [Inside Leopold Aschenbrenner’s Situational Awareness Fund: the AGI investment thesis, the full portfolio breakdown, and the framework any investor, entrepreneur, or operator can steal right now]

The Complete Claude /goal Guide for AI Agents 🤖 [What Claude /goal actually is, why most invocations fail, and how to write production-grade goal conditions for financial research, backtesting, and live market monitoring]

Circle is building a monopoly in plain sight, but the toll is set by the Fed 🤷♂️🏦 [breaking down Circle’s latest Q1 2026 financials, understanding the real economics beneath the headline growth, & figuring out whether Circle deserves a spot in your portfolio + bonus dive into Circle’s Agentic AI bet, which is a clear escape plan]

Coinbase’s Q1 2026: the House always wins, until the Casino empties 🤷♂️🎰 [deep dive into Coinbase’s Q1 2026, breaking down the key financial facts & figures, what they mean, what’s next & whether it’s worth your time and money now + bonus deep dive into the latest financials of it’s close partner Circle inside]

How to Build an AI Agent from Scratch (With Working Code) 🤖 [The design framework, working code, and hard-won lessons that take you from “I want to build an AI Agent” to a working one - in under 60 minutes]

Inside Revolut’s PRAGMA: The Foundation Model Trained on 40 Billion Banking Events 🧠 [Architecture, performance benchmarks vs. Stripe, Mastercard, and Visa, regulatory risks, and why PRAGMA may be the most consequential AI bet in consumer finance]

Claude Cowork Commands, Scheduled Tasks & Automation Workflows: The Operator’s Playbook 🤖 [Every real slash command, the exact prompts that run deal flow and investor updates on autopilot, and the failure modes that will cost you hours if you don’t know them first]

The System for Never Hitting Claude’s Limits 🤖 [Most users burn the majority of their token allocation on architecture mistakes, not actual work. Here’s the operational framework that fixes it]

As for today, here are the 3 fascinating FinTech stories that are changing the world of financial technology as we know it. This was yet another wild week in the financial technology space, so make sure to check all the above stories.

Stripe turned its own workforce into an AI Product Lab 🤖🧪

Following the trends 🧑💻 Most companies hand employees a ChatGPT license and call it a transformation. FinTech giant Stripe is now embedding full-time AI practitioners inside its marketing org, one for every 20 people, with a mandate to rewire how each person works from the ground up.

The bet here is definitely not on better tools. It’s on permanently changing human behavior at enterprise scale, and doing it through a model borrowed from one of the most controversial companies in tech. Stripe is now treating its own workforce as a controlled experiment in human-AI collaboration, and the data coming out of that experiment feeds directly into the agentic commerce infrastructure it’s selling to everyone else.

It’s basically a flywheel hiding in a job posting ⚙️

Let’s take a closer look at this, understand what it’s truly all about, why it matters, and why everyone in FinTech, finance, and tech should be paying very close attention.

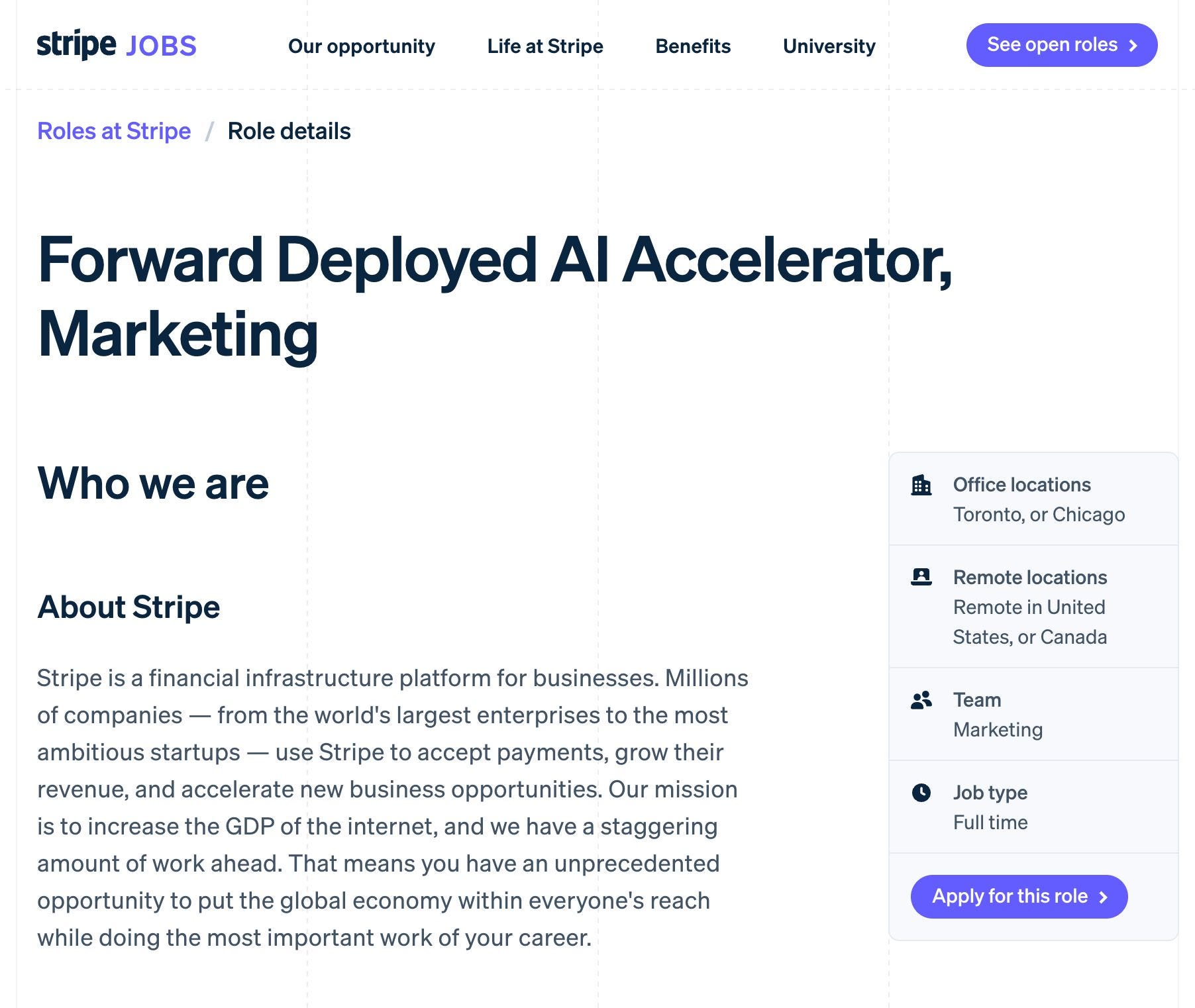

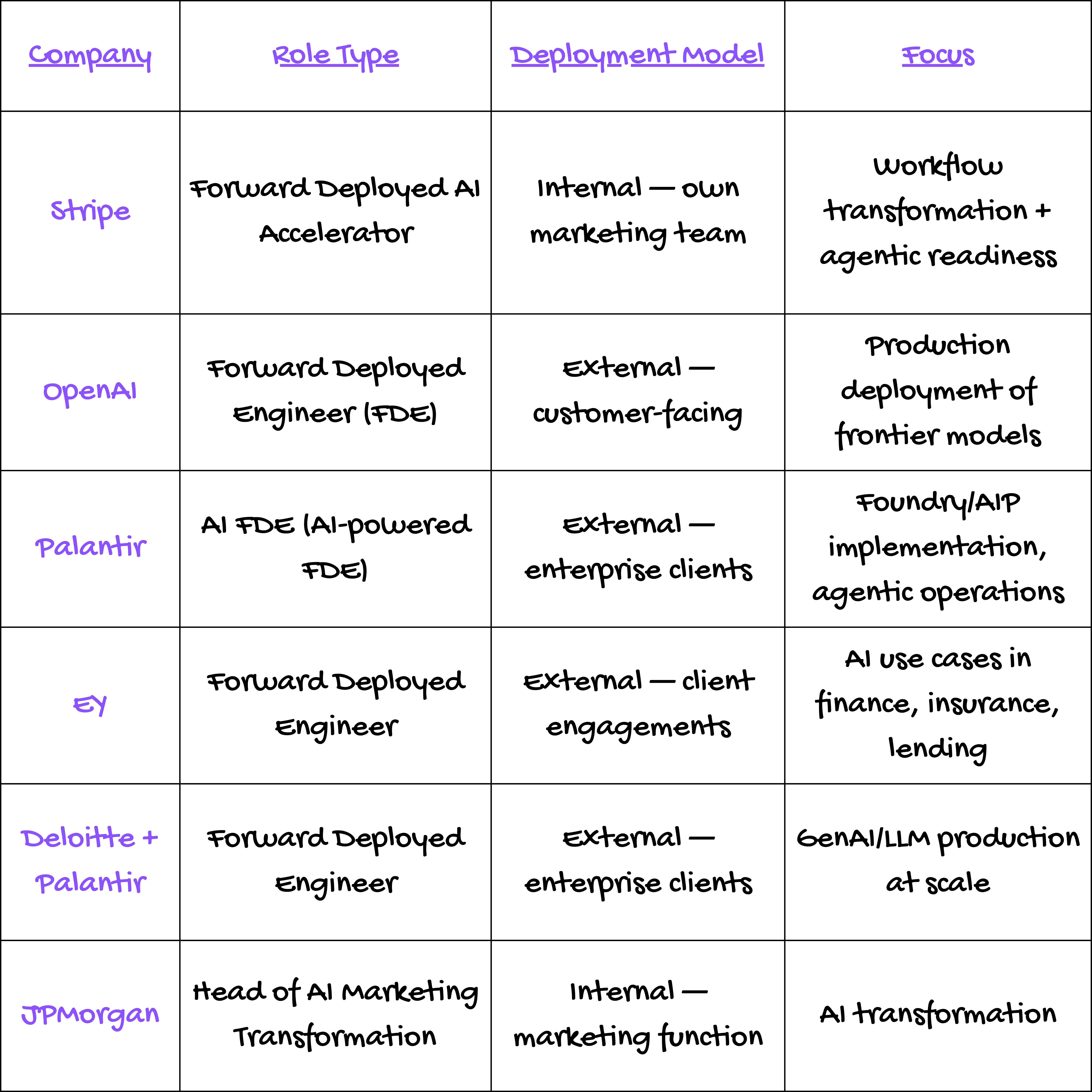

More on this 👉 The role is called “Forward Deployed AI Accelerator,” borrowed from Palantir’s playbook of embedding engineers inside client organizations to close the gap between software and operations.

Interestingly, Stripe flipped the model inward. Each FDA maps a marketer’s actual workflows, builds custom agents and automations for their specific responsibilities, then coaches them through a structured maturity model: awareness, first win, regular use, full transformation, self-sufficiency.

What’s important to stress here is that success isn’t measured in adoption dashboards. It’s measured in workflows that permanently start with an AI tool. The endgame spelled out in the job spec is super clear: preparing teams to design and oversee autonomous multi-agent systems, not just write better prompts.

Basically, run something similar to Claude Managed Agents inside the org.

Zoom out 🔎 Now, look at the bigger picture and read this alongside Stripe Sessions 2026, where the company shipped 288 products aimed at making AI agents first-class economic actors.

→ Link’s agent wallet covers 250 million users.

→ The Machine Payments Protocol lets agents pay for API calls autonomously.

All while Stripe processed $1.9 trillion in payment volume last year at a whopping $159 billion valuation.

ICYMI: Stripe is building Visa for Machines 🤖💳 [two most important product launches from Stripe Sessions 2026, & how the fintech giant is building the full financial stack for autonomous AI + bonus deep dives into Stripe & how Google just won Agentic Commerce]

Most importantly, the connection between the internal and external plays is the part that most people seem to miss here. Every workflow the FDA team transforms inside Stripe generates real telemetry on how humans and AI agents collaborate in high-stakes enterprise contexts. That operational knowledge thus feeds directly into the agentic infrastructure Stripe sells.

The org itself then becomes a proving ground for the products. Brilliant play 👏

Meanwhile, the protocol wars Stripe was supposed to fight are already over. Seven months after co-building the Agentic Commerce Protocol with OpenAI, Stripe walked across the aisle and joined Google’s Universal Commerce Protocol Tech Council alongside Amazon, Microsoft, Meta, and Salesforce.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch two things from here. First and foremost, whether Google embeds UCP primitives directly into Gemini’s agent infrastructure, giving it a structural advantage over every other AI assistant in commerce. If that happens, Google doesn’t just own the standard. It owns the best implementation of the standard. Second, whether Stripe’s FDA model spreads beyond marketing into risk, compliance, and merchant operations by year-end. Ramp is already running a version for its largest customers. Zooming out, the deeper question now is whether the telemetry from internal transformation creates a durable product advantage, or whether the model quietly dies once the initial cohort reaches self-sufficiency. If agents mature fast enough, the humans who trained alongside them become the most valuable operators in fintech. If they don’t, Stripe just built an expensive coaching program. The early signal from a 70% reduction in content review cycle time suggests the former. But conversion, not adoption, remains the test that matters for everything Stripe is building, inside and out.

ICYMI:

Anthropic is coming for RegTech: Claude won’t sell compliance software - it wants to be the Compliance Layer 😳🤖

The news 🗞️ Dun & Bradstreet just handed Claude the keys to 580 million business entities. And no, that’s not a data partnership. That’s Anthropic positioning itself as the operating system for regulated finance.

The D&B integration is the clearest signal yet that Anthropic is building a vertically integrated compliance infrastructure layer, with KYC/KYB, credit risk, and supplier due diligence running natively inside Claude rather than through the patchwork of middleware vendors that banks and fintechs rely on today.

Let’s break down exactly how the integration works, what it means for RegTech startups competing in the same space, where the competitive pressure lands for OpenAI and Google, and what regulatory response could accelerate or stall the whole thesis.

More on this 👉 Yesterday, D&B announced it would pipe its Commercial Graph directly into Claude through Anthropic’s Model Context Protocol. MCP is the quiet piece that matters here: it’s a standardized connector that gives AI agents auditable, permissioned access to external data while preserving lineage.

Think of it less as an API and more as a governed nervous system for agentic workflows. The integration means Claude can now resolve entities against D&B’s D-U-N-S Number, traverse ownership structures, cross-reference risk signals, and produce regulator-ready documentation. KYC/KYB workflows that took compliance teams days can now be assembled in minutes inside Claude. Let that sink in.

Zoom out 🔎 The timing was surgical here. We must remember that just recently Anthropic dropped ten financial-services agent templates, including a KYC screener that assembles entity files, reviews source documents, and packages escalation reports. D&B showed up as the named data backbone.

Anthropic also announced MCP connectors for Moody’s (credit ratings on 600M+ companies), Verisk (insurance data), and IBISWorld. Add in the $1.5 billion joint venture with Blackstone, Goldman Sachs, and others to embed Claude directly into portfolio companies, and the pattern is clear: Anthropic is building a vertically integrated compliance stack, sold not as software but as infrastructure.

As D&B’s GM of Risk Alex Zuck put it, Claude isn’t just getting more data. It’s getting “the verified context and decision logic required to act.” That distinction between data-as-input and data-as-reasoning is what makes this more than a press release.

Future outlook 🔮 That said, here’s what the RegTech world should be paying attention to.

First and foremost, a large share of compliance middleware exists because KYC/KYB is painful: stitching together vendor portals, normalizing data formats, routing cases through approval chains. If Claude can do that natively, grounded in the same D&B data these platforms already resell, the value proposition of pure-play orchestration vendors erodes fast. The survivors will hence be those with proprietary regulatory logic, jurisdiction-specific interpretation, or deep workflow customization that a general-purpose agent can’t replicate out of the box.

The second-order effect is competitive pressure on other foundation model providers. OpenAI, Google, and xAI now face a gap in regulated verticals. Anthropic’s constitutional AI framework and explainability focus were always a better fit for compliance use cases; locking in D&B and Moody’s as native data partners converts that philosophical advantage into a structural moat.

Matching it therefore requires not just data deals but the governed access layer that MCP provides.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch two things over the next 12 months. First, whether banks actually run production KYC through Claude or treat it as a pilot curiosity. Second, how regulators respond. They’ve been asking for explainability and audit trails in AI-assisted decisions already. Anthropic just gave them exactly that, which could accelerate formal guidance on agentic compliance. If regulators bless the pattern, the adoption curve steepens dramatically. If they balk at autonomous entity verification, even with human-in-the-loop, the whole thesis slows down (maybe even quite dramatically). Either way, the era of selling compliance data in static reports is ending. The money moves to whoever controls the intelligence layer where decisions actually get made. And for now, that layer seems to be ClaudeOS.

ICYMI: Anthropic stopped selling AI to Wall Street and started becoming Wall Street’s Operating System 🏦🧠 [what the 10 finance AI agents actually do, why FactSet dropped 8.1% the same day, what the FIS infrastructure deal and $1.5B Blackstone/Goldman JV mean for distribution & what to expect next + bonus Guide on Claude Managed Agents, Claude Code Routines, & How to Build Your First AI Agent from Sratch inside]

Anthropic’s Claude for Small Business is not just an AI chatbot. It’s a bid to own the whole SMB back office 🤖📊 [what Claude for Small Business really is, why it matters, & what it means for investors, founders, and SaaS companies + bonus dive into how I turned Claude Cowork into my Personal COO, and Anthropic that just told AI founders exactly what to build in 2026]

Circle Agent Stack is an escape plan disguised as a product launch 💸🪙

The news 🗞️ 99% of Circle’s $1.68 billion in 2024 revenue came from just one source: interest on the reserves backing USDC. A single percentage-point rate cut costs them $441 million. Let that sink in 😳

That’s not a business model - it’s basically a weather bet. Yesterday, Circle showed us what the escape plan looks like.

Let’s unpack this.

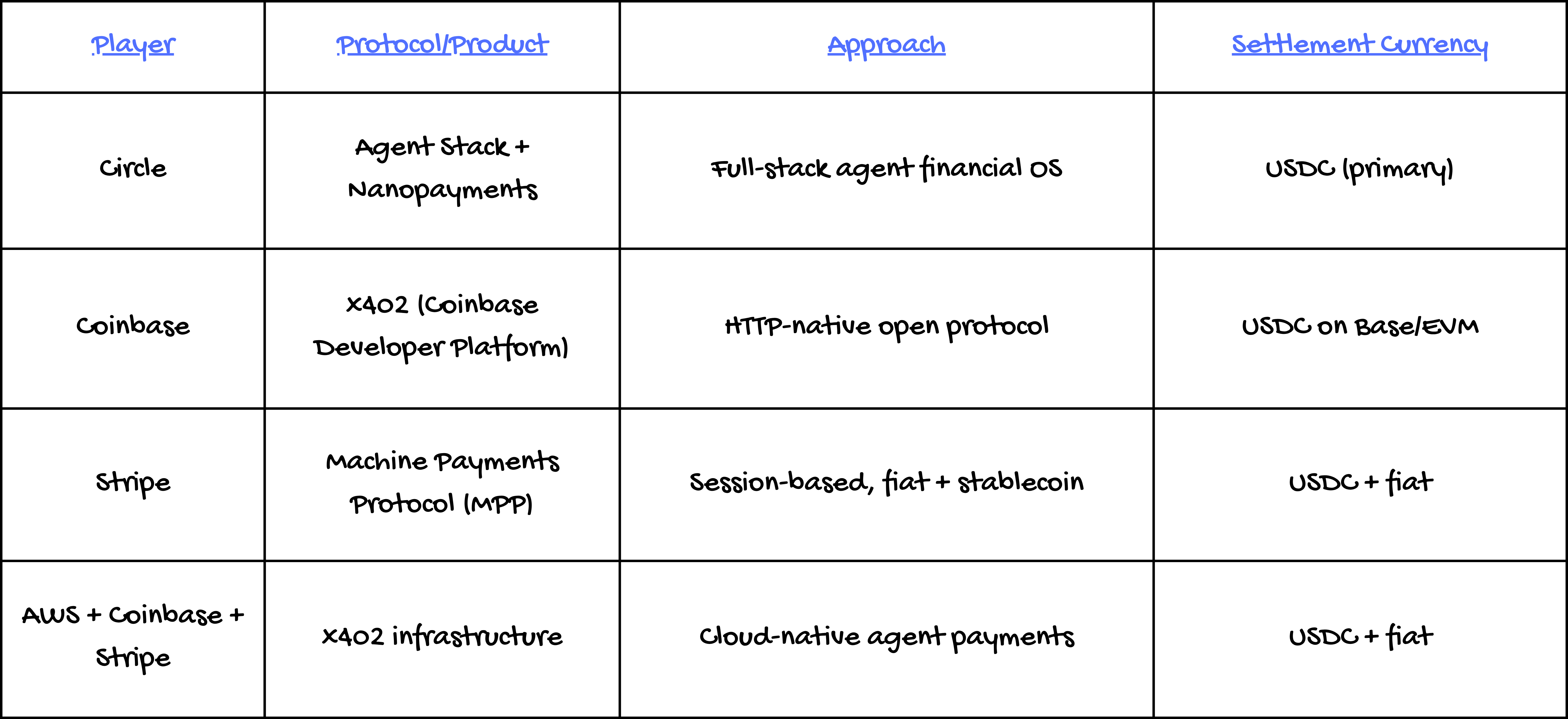

More on this 👉 On May 11, Circle launched Agent Stack, a five-piece toolkit that lets AI agents hold wallets, discover services, and transact in USDC autonomously.

Agent Wallets enforce spending rules before transactions execute.

An Agent Marketplace exposes 500+ service endpoints for programmatic discovery and payment.

A CLI gives developers deterministic control over wallets, payments, and policies.

Nanopayments, powered by Circle Gateway, enable gas-free USDC transfers down to $0.000001 by batching thousands of off-chain authorizations into single on-chain settlements.

And Circle Skills hand AI coding agents the structured context to build on all of it without fumbling USDC’s six-decimal precision.

The timing is very deliberate here. The x402 protocol, the emerging HTTP-native payment standard now governed under the Linux Foundation with Coinbase, AWS, Google, Stripe, Visa, and Anthropic as members, processed $24.24 million in the prior 30 days. USDC settled 99.8% of that volume.

In other words, the market picked USDC as the currency of agent commerce before Circle even shipped the infrastructure. So Circle is now building the plumbing around a choice already made.

But the strategic logic runs deeper than AI hype.

Remember that Circle paid Coinbase and other distribution partners $1.01 billion in 2024. In Q1 2025, Coinbase earned $300 million from its USDC revenue-sharing deal while Circle netted $230 million. Agent Stack is permissionless. Every developer who builds directly on it creates USDC demand that flows through Circle’s own rails, not Coinbase’s.

The agentic economy, where software agents interact programmatically rather than through consumer exchanges, is structurally less dependent on Coinbase’s distribution. That’s not a coincidence - it’s the point, and that’s exactly why Circle is making this bet.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, we must note that the current agentic payment volume is $50 million across 40,000 on-chain agents, which is 0.0001% of stablecoin annual settlement. Circle is spending $570-585 million on platform buildout in 2026 against a market that McKinsey projects at $1 trillion in US agentic commerce by 2030, but that barely exists today. If Stripe’s Machine Payments Protocol captures developers through its $1.9 trillion in existing payment relationships and routes them toward fiat settlement, USDC’s 99.8% share of agent payments could prove temporary. Therefore, when looking ahead, watch two things. First, whether Arc mainnet (Circle’s own L1 with USDC as gas) launches with enough institutional adoption to make the agent-wallet-to-settlement pipeline fully captive. Second, whether the Coinbase revenue-sharing renegotiation in 2026 reflects a Circle that finally has distribution leverage of its own. Most importantly, Agent Stack isn’t a product launch. It’s Circle’s bid to stop being a fund and start being a platform, before the rate cycle makes the decision for them.

ICYMI: Circle is building a monopoly in plain sight, but the toll is set by the Fed 🤷♂️🏦 [breaking down Circle’s latest Q1 2026 financials, understanding the real economics beneath the headline growth, & figuring out whether Circle deserves a spot in your portfolio + bonus dive into Circle’s Agentic AI bet, which is a clear escape plan]

🧠 What else I’m watching

Alipay Enables AI Shopping Delegation 🛒 Alipay has expanded its AI Pay feature, now allowing users to delegate purchases to AI agents. Launched last year, AI Pay has surpassed 100M users and processed over 120M transactions in a single week. Integrated with Alibaba’s Taobao, users can authorize an AI assistant to make purchases on their behalf: after voice commands, Alipay AI Pay generates a one-time delegation for the specific purchase, verifies the user’s identity, and lets the AI monitor prices and complete the order. Alipay plans to extend this capability to recurring scenarios like commuting, utility payments, and repeat orders, further automating everyday transactions. ICYMI:

Google Integrates BNPL for AI Shopping 🛒 Google is adding Affirm and Klarna Buy Now Pay Later (BNPL) options to Google Pay for users shopping in the Gemini app or Google Search, including AI mode. Shoppers will see Affirm and Klarna buttons at checkout, enabling installment payments. Built on Google’s Universal Commerce Protocol, the integration supports AI-driven shopping experiences. ICYMI: The Android of Commerce - How Google Is Building the Interface Between AI & Money 🤖💸 [why recently introduced WebMCP is a game-changer, how it stacks perfectly into Google’s Android of Commerce playbook, things worth watching, what’s next for FinTechs/Banks/Payments companies, etc. + bonus deep dives into Google’s UCP, how I built an AI OS to run startup with Claude, and how AI is eating software today]

FinBox’s Atlas Speeds Up Loans with AI 🏦 FinBox has launched Atlas, an AI-native lending platform that slashes loan processing from three weeks to 24 hours. Replacing manual workflows with AI agents, Atlas handles borrower onboarding, document validation, and decision-making. Early results show 85% application completion rates (most in under 10 minutes) and 95%+ first-time-right rates, with turnaround times cut from 21 days to one day and file send-backs reduced by 60%. Atlas Flow uses conversational interfaces across WhatsApp, voice, and video, while Atlas Origin autonomously processes documents, flagging discrepancies in real time. Five financial institutions are already implementing Atlas, with modules for credit appraisal and fraud detection in development. ICYMI:

💸 Following the Money

Prediction market Kalshi has seen its valuation double to $22B in five months off the back of a $1B Series F funding round.

Squads raises $18M to build a stablecoin operating system. ICYMI:

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Interesting how fintech is increasingly becoming an AI-infrastructure story rather than standalone product innovation. The real differentiation now seems to be shifting toward distribution, proprietary data, and regulatory positioning. Curious to see where durable moats form as AI tooling gets more commoditized.

👌👌👌 perfect