Revolut is rebuilding its revenue mix before anyone sees the S-1 🤑🏦; OpenAI is paying for YC’s next batch in tokens it prints itself 🫣💸

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

SpaceX IPO: Why the Biggest Listing in History Might Be Uninvestable at $1.75 Trillion 🪐 [The S-1 reveals a $7 billion Starlink profit machine subsidizing $30B in annual AI cash burn, while Elon Musk holds 85% of the vote with no sunset, no independent board, and no path to remove him]

Ex-OpenAI’s Aschenbrenner Bet $5.5B on AI Chips. Now He’s Betting $8.5B Against Them 💸 [Leopold Aschenbrenner’s AI hedge fund Situational Awareness went from pure AI long to 62% short semiconductors in one quarter. Here’s what changed and why the thesis still holds]

Coatue’s May 2026 Report: The $12 Trillion AI Bet and Who Ends Up on the Wrong Side 📊 [Coatue’s latest public markets report reveals the most extreme winner/loser split in tech stock history, a $12 trillion AI capex wave, and one brutal framework that predicts exactly who wins]

Anthropic Just Told AI Founders Exactly What to Build in 2026 🦄 [1 million conversations. 9 consumer AI domains. A full founder playbook - plus where Anthropic’s own products will and won’t compete]

ChatGPT’s new personal finance feature is OpenAI’s bid to kill the fintech app economy 🤖📲 [what it’s all about, which fintechs should worry the most, how it connects to OpenAI’s Super App Play & what’s next + bonus deep dives into Anthropic & how it’s becoming Wall Street’s OS, their SME OS play, and what AI startup founders should build in 2026]

Google Universal Cart and the Universal Commerce Protocol are Google’s bid to become the operating system of e-commerce ⚙️🛍️ [what Google Universal Cart is all about, why it matters & how it can transform e-commerce forever + bonus deep dives into Google’s UCP, how it just won Agentic Commerce & why AmEx skipped the protocol race altogether inside]

The Complete Claude /goal Guide for AI Agents 🤖 [What Claude /goal actually is, why most invocations fail, and how to write production-grade goal conditions for financial research, backtesting, and live market monitoring]

How to Build an AI Agent from Scratch (With Working Code) 🤖 [The design framework, working code, and hard-won lessons that take you from “I want to build an AI Agent” to a working one - in under 60 minutes]

Claude Cowork Commands, Scheduled Tasks & Automation Workflows: The Operator’s Playbook 🤖 [Every real slash command, the exact prompts that run deal flow and investor updates on autopilot, and the failure modes that will cost you hours if you don’t know them first]

The System for Never Hitting Claude’s Limits 🤖 [Most users burn the majority of their token allocation on architecture mistakes, not actual work. Here’s the operational framework that fixes it]

As for today, here are the 2 incredible FinTech stories that are transforming the world of financial technology as we know it. This was yet another insane week in the financial technology space, so make sure to check all the above stories.

Revolut is rebuilding its revenue mix before anyone sees the S-1 🤑🏦

Following the money 💸 FinTech giant and Europe’s most valuable private company Revolut, doesn’t have a banking problem. It has a revenue-quality problem, and two moves in the past week show it knows exactly how to fix it.

Let’s take a look.

More on this 👉 The London fintech is launching a private banking arm targeting clients with £500,000 or more in deposits, with services rolling out later this year. The FCA just granted its trading subsidiary permission to offer leveraged products, managed portfolios, and investment advisory.

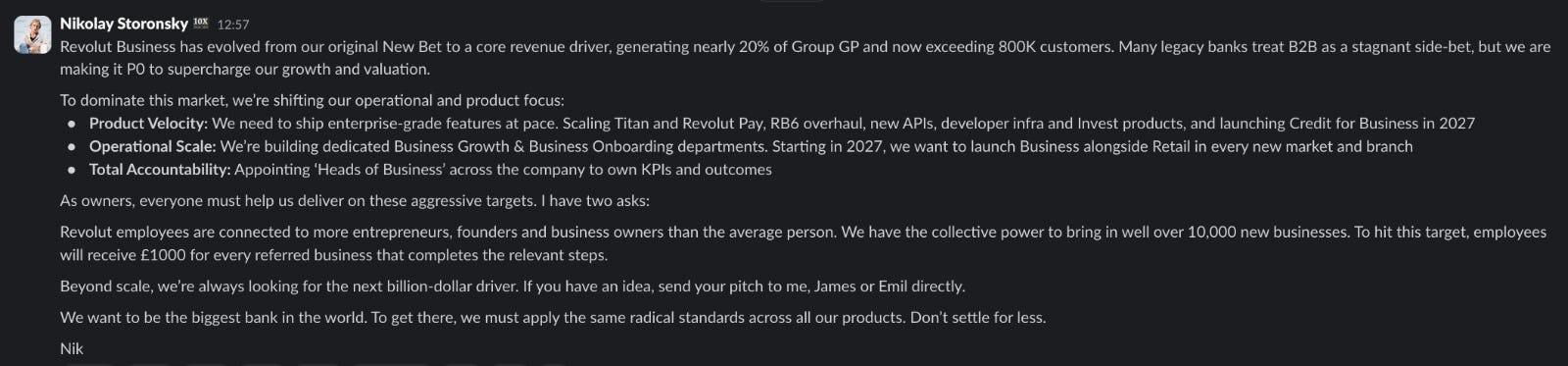

Meanwhile, a leaked internal memo from CEO Nik Storonsky on May 15 designated Revolut Business as the company’s top strategic priority, backing it with dedicated growth teams, a £1,000-per-head employee referral bonus for new business accounts, and a commitment to bundle business banking into every new market starting 2027. Not too shabby!

Zoom out 🔎 Read these two developments together. Revolut posted £4.5 billion in revenue last year and £1.7 billion in pre-tax profit. Impressive numbers, but 76% of revenue comes from fees on cards, FX, subscriptions, and crypto trading. Public markets will discount that mix. It’s volatile, competition-exposed, and hard to model forward. Private banking (AUM-based fees, advisory, lending spreads) and sticky B2B relationships (£940 estimated ARR per business customer, 800,000 accounts and climbing) are the antidote.

The private banking play targets a specific gap. Coutts now requires roughly £3 million minimums. Revolut already has millions of UK users in the £500,000-to-£3 million range who are barely monetized. Hiring ex-HSBC private bankers to pair with a digital-first platform is the right hybrid model for mass-affluent clients who want service without the theater.

We can note that wealth already generated £663 million last year. Even modest early traction, say 5,000 clients at £1.5 million average AUM, adds £5-8 billion in managed assets and tens of millions in high-margin recurring revenue.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, there are several things to watch. First and foremost, the IPO isn’t coming before 2028, and the $200 billion valuation target demands a story that looks more like JPMorgan than Robinhood. Thus, every quarter between now and then (if/when possible), track two numbers: AUM growth in the new wealth segment and B2B’s share of gross profit (already approaching 20%). If both inflect upward, Revolut gets its multiple re-rating before it ever files. If the white-glove service falls flat or credit underwriting stumbles in new markets, the narrative unravels fast. All in all, we can definitely agree that the strategy is correct here. Execution is the only remaining question, and it’s not a small one. But so far, Revolut hasn’t had any problems executing…

ICYMI: Inside Revolut’s PRAGMA: The Foundation Model Trained on 40 Billion Banking Events 🧠 [Architecture, performance benchmarks vs. Stripe, Mastercard, and Visa, regulatory risks, and why PRAGMA may be the most consequential AI bet in consumer finance]

Revolut is the most profitable FinTech on Earth, and it hasn’t even started lending yet 🤯📈 [unpacking the fee-income fortress that makes Revolut structurally different from every competitor, the lending optionality coiled inside that balance sheet, the regulatory dominoes now falling in sequence, and whether $75B is expensive or whether the market is about to find out it was way too cheap + more bonus reads on Revolut, how it’s leveraging AI & bonus deep dives into the latest financials of Nubank, SoFi, Robinhood, and Coinbase inside]

OpenAI is paying for YC’s next batch in tokens it prints itself 🫣💸

The news 🗞️ OpenAI co-founder & CEO Sam Altman just found a way to turn inference compute into venture capital.

Let’s unpack this.

More on this 👉 OpenAI is now offering every startup in YC’s Spring 2026 batch - roughly 169 companies - $2 million in API credits through an uncapped SAFE. That’s ~$338 million at retail prices, paid in a currency OpenAI manufactures at a fraction of face value as marginal inference costs keep falling.

In return, OpenAI gets equity that converts at the next priced round, plus something worth more than any cap table line: deep visibility into what the sharpest AI-native founders are actually building, at cohort scale, in real time.

And that’s hard to put a price tag on.

Zoom out 🔎 Of course, the playbook isn’t new. Yuri Milner’s 2011 blanket bet on YC through SV Angel was the template - $150K cash per company, broad exposure, no picking. Altman, who was at YC when that deal went down, is running the same play with a critical twist: he’s paying in his own product. Every “dollar” of credits consumed flows back as usage data, training signal, and switching costs. The founders get transformative compute runway. OpenAI gets lock-in dressed up as patronage 😎

Altman’s framing - “tokenmaxxing” over headcount - tells you exactly where he wants these companies to land architecturally: inference-heavy, deeply coupled to OpenAI’s stack, expensive to migrate. For teams already planning to burn through trillions of tokens, the dilution math on an uncapped SAFE looks tolerable.

For those building thin orchestration layers on top of foundation models, taking this deal is handing your playbook to the one company best positioned to replicate it inside ChatGPT.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, here’s what you should watch. First, competitive response: if Anthropic or Google counter with credits-for-equity programs (or credits with no equity attached), the subsidy war gets interesting fast. Second, post-credit behavior: when the $2M runs dry, do these startups stay on OpenAI or scatter to multi-model architectures? That answer will tell you whether this was customer acquisition or ecosystem capture. Third, product overlap: track OpenAI’s feature launches over the next 18 months against what gains traction in this batch. If the pattern rhymes with Amazon Marketplace or Apple’s App Store history, founders will notice, and the next cohort won’t sign as easily.

ICYMI: ChatGPT’s new personal finance feature is OpenAI’s bid to kill the fintech app economy 🤖📲 [what it’s all about, which fintechs should worry the most, how it connects to OpenAI’s Super App Play & what’s next + bonus deep dives into Anthropic & how it’s becoming Wall Street’s OS, their SME OS play, and what AI startup founders should build in 2026]

🧠 What else I’m watching

More Bank AI Layoffs 🏦 Standard Chartered plans to cut 7,800 back-office jobs - 15% of its 52,000 support roles - over four years, targeting Chennai, Bengaluru, Kuala Lumpur, and Warsaw. CEO Bill Winters frames the move as replacing lower-value tasks with AI-driven automation, not cost-cutting, while some staff will be reskilled. The bank is investing in AI to streamline operations, positioning the technology as a key enabler for efficiency and transformation in its workforce strategy. Yet another reminder to productize yourself 😉 ICYMI:

Fintech AI Skills Drive 📈 Zopa and ClearScore launched Jobs2030, a coalition upskilling 100,000 fintech and banking professionals in AI by 2030, with 22 members already on board. The free initiative, built around technology, content, training, hiring, and advocacy, offers five courses and 12 modules by year-end, tailored to compliance, engineering, operations, and product roles. Training on Zenarate integrates with LLMs like Gemini and ChatGPT, combining AI coaching, simulations, and real-world scenarios. Backed by Innovate Finance, The City of London Corporation, and venture firms, the program aims to deliver practical AI skills and foster better customer outcomes through industry-led expertise. ICYMI:

AI Streamlines Vendor Risks 🤖 Deutsche Bank’s TPRM AI accelerates third-party vendor risk assessments, cutting document review time from 30 minutes to under two minutes for up to five files. Developed in-house, the system uses sequential AI agents to retrieve control questions, draft responses, and propose outcomes with 90% accuracy, followed by human validation. This cloud-based solution scales with demand, reducing onboarding timelines and costs while maintaining regulatory compliance. ICYMI:

💸 Following the Money

Mercury, a provider of banking services for entrepreneurs and the tech industry, has raised $200M in a Series D at a $5.2B valuation.

Stablecoin-powered digital banking and investment platform Fasset has raised $51M in Series B funding.

National Australia Bank has acquired account-to-account payments platform Banked. Financial terms were not disclosed.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

can't believe this is free... thanks again Linas!

Awesome read! Thanks for sharing this.

QQ - so what's the ultimate goal for Revolut?