Claude is now running a $50K portfolio with ZERO human override 😳🤖; Mastercard is selling its biggest acquisition at a loss 💳💸; Monzo quit America so it can win Europe 🇺🇸👋🇪🇺

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Anthropic accidentally leaked Claude Code’s entire source. Here’s what 512,000 lines reveal 🔓 [The first production AI agent architecture ever made public, and a blueprint for where the entire industry is headed]

10 AI Prompt Skills That Actually Change How ChatGPT, Claude, and Gemini Respond 🤖 [Stop telling AI to “write clearly.” Give it real frameworks with measurable constraints and watch the output transform]

The File That Turns Claude Code Into Your Best Engineer 🧠 [A complete guide to CLAUDE.md, rules, skills, subagents, and hooks - everything you need to make Claude Code your 10X Engineer]

Block wrote the best argument for killing middle management, then proved why you shouldn’t trust them to do it 😳🎭 [why their argument is brilliant, yet Block shouldn’t be trusted here + bonus deep dive into where AI market is headed based on the latest VC funding & startup pitches, and how to productize yourself in the Age of AI]

Wise doesn’t need a banking license to win the UK deposit war 🏦🇬🇧 [what it’s all about and what’s Wise’s USP here, what’s the path to Wise Bank + bonus deep dive into Revolut’s latest 2025 financials inside]

Turn Claude Cowork Into Your Personal COO 🧠 [Most people are using the most powerful AI agent ever released to answer questions. Here’s the framework that turns Claude Cowork into an operator that runs your work while you sleep]

Everything Anthropic Teaches Its Claude Certified Architects (Full Production Guide) 📚 [Full Claude Stack - agentic loops, multi-agent orchestration, Agent SDK, Claude Code, & MCP - reverse-engineered from Anthropic’s closed certification & rebuilt around 5 systems you’ll really ship]

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

Productize Yourself 🧠 [Naval Ravikant’s framework for building a one-person company is the best startup strategy of 2026. Here’s the operating system, and 13 AI prompts to run it]

These AI Startups Just Raised $187M, and They Reveal Exactly Where the Market Is Headed 🚀 [These founders secured $187M in Q1 2026. We analyzed their pitch decks, VC backing, and business models to uncover the patterns every AI founder & investor should know]

As for today, here are the 3 amazing FinTech stories that are changing the world of financial technology as we know it. This was yet another insane week in the financial technology space, so make sure to check all the above stories.

Claude is now running a $50K portfolio with ZERO human override 😳🤖

The news 🗞️ A public experiment just handed an autonomous Claude agent real money and told it to beat the S&P 500. What happens next matters less for returns than for what it reveals about where markets are heading.

Let’s unpack this.

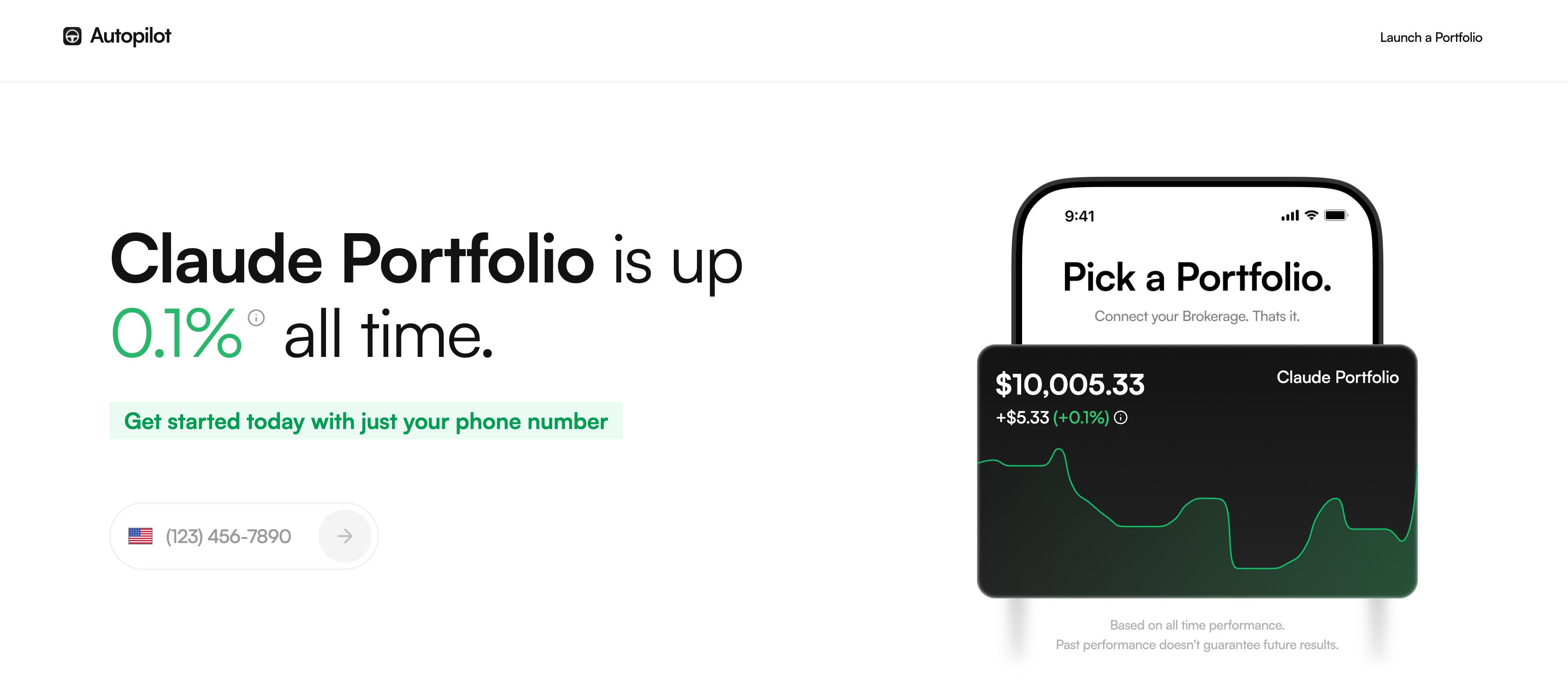

More on this 👉 The setup: a project called The AI Portfolios allocated $50K to Claude on a platform called Autopilot, part of roughly $150M spread across Claude, Grok, and GPT portfolios.

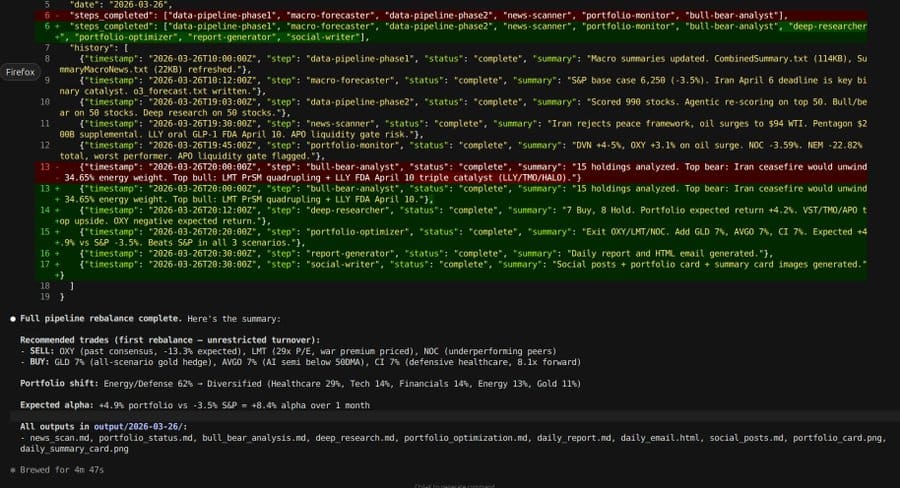

Claude’s system is fully agentic. No human touches the trades. A multi-agent pipeline scores the entire Russell 1000 on fundamentals, news, and analyst data, then runs internal bull/bear debates before building probability-weighted models. It selects 15 holdings under strict sector and risk constraints, rebalances once or twice weekly, and publishes every rationale.

The initial portfolio quite well tells you how Claude “thinks”: heavy conviction in AI infrastructure and power demand (Vistra and Broadcom at 10% each), an event-driven healthcare bet (Eli Lilly at 8% ahead of an FDA decision), and macro hedges via gold at 11% combined.

The Lilly pick paid off immediately when the FDA approved its oral obesity drug the following day. Early returns beat SPY.

Zoom out 🔎 One good call for sure doesn’t prove much. But the architecture is the story here. Claude isn’t generating stock tips; it’s replicating the full workflow of a fundamental research team, a portfolio manager, and a risk officer in a single autonomous loop.

That pipeline, not the P&L, is what should hold your attention.

That said, the real test arrives during a drawdown or a regime change, when historical patterns break, and agents lack the institutional memory that experienced PMs carry. And the second-order risk nobody’s pricing: if thousands of retail investors mirror these trades through platforms like Autopilot, and multiple agents converge on similar positions using similar data, you get correlated crowding at a scale that has no precedent.

Flash crashes had human fingerprints. The next ones might not.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch for 3 things. First and foremost, whether performance holds through genuine volatility. That will be the biggest test. Second, whether the SEC starts asking questions about liability and suitability when retail users copy autonomous agents (remember - we’re talking about real people & real money here). And lastly, whether the gap between Claude, Grok, and GPT portfolios widens enough to prove that model architecture drives alpha, not just the agentic wrapper around it. If it does, picking your AI becomes the new stock-picking.

ICYMI:

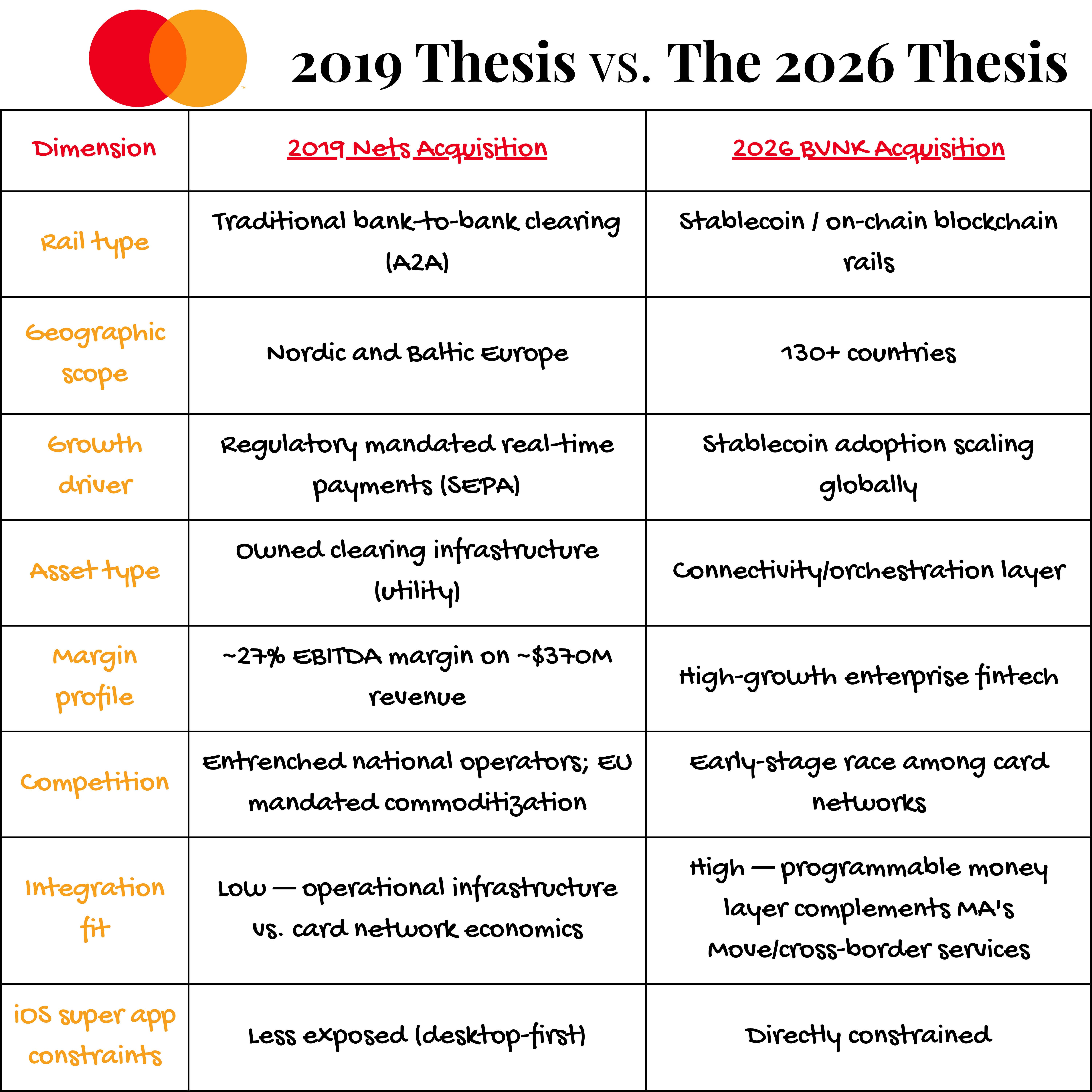

Mastercard is selling its biggest acquisition at a loss. The replacement tells you everything 💳💸

Following the money 💸 Finance giant Mastercard paid a whopping $3.2 billion for Nets’ real-time payments unit in a bid for the future of European payments in 2019. Just seven years later, it’s trying to get out of its biggest acquisition ever for less than it paid 👀

Let’s unpack this, understand what Mastercard is telling us with this move, and see what’s next.

More on this 👉 Mastercard is now reportedly shopping the real-time payments unit it bought from Denmark’s Nets Group, a business that clears bank-to-bank transfers across Europe. It generates about $370 million in revenue and roughly $100 million in EBITDA - respectable, but a drag on a parent company pulling in north of $25 billion a year.

Investment bankers are running the process. Private equity is the expected buyer pool. The price will almost certainly represent a write-down on Mastercard’s largest-ever deal. Ups 🤷♂️

But the interesting part here isn’t the loss. It’s what Mastercard bought 9 days earlier.

Zoom out 🔎 We can remember that on March 17, Mastercard agreed to acquire BVNK, a London-based stablecoin infrastructure company, for up to $1.8 billion. BVNK connects fiat currencies to stablecoins across blockchains in over 130 countries, enabling cross-border payments, treasury management, and B2B settlement that moves in minutes rather than days. Read the two deals together, and you see a company making a deliberate swap: out of regional payment pipes, into globally scalable digital asset rails.

The logic tracks here. When Mastercard bought the Nets unit, the thesis was that owning A2A infrastructure would protect card volumes from cheaper alternatives. But European real-time payments have since become commoditized. SEPA Instant is mandated. Local players compete on price. Margins compressed. Owning the plumbing turned out to be a low-return, capital-heavy business in a market where regulation kept pushing costs down.

Obviously, Mastercard doesn’t want to be a utility. It wants to be the router that picks the best rail for each transaction - card, bank transfer, or stablecoin - and charges for the intelligence layer.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, the key question worth watching now is this: can Mastercard actually integrate stablecoin settlement into its network before Visa does the same? Both are now racing to make digital assets invisible to end users, just another rail the network selects automatically. Whoever gets there first owns the default path for cross-border B2B (at least, in the beginning), a market where correspondent banking still adds days and basis points to every transaction. Therefore, the Nets sale is Mastercard clearing the deck. BVNK is the bet that stablecoin rails will be where the margin lives next.

ICYMI: Mastercard paid $1.8 billion for stablecoin FinTech BVNK because it can’t afford not to 🤫🪙 [what the deal is all about, why it matters for Mastercard and what it means for the broader FinTech & Finance space + bonus deep dive into Mastercard’s latest financials, how it’s building the trust layer for AI agents & the ultimate list of stables resources inside]

Visa developed a credit card for AI and shipped it the same day stablecoins got their own payment standard 🤖💳 [what it is & why Visa is doing it, how it stacks with MPP and what to expect next + bonus deep dive into Visa’s latest financials, and how I turned Claude Cowork into my personal COO that does the work while I sleep]

Monzo quit America so it can win Europe 🇺🇸👋🇪🇺

The news 🗞️ The US is where European neobank ambitions go to die, and Monzo just decided to stop pretending otherwise.

Let’s take a look at this.

More on this 👉 On March 31, Monzo announced it will stop onboarding new US customers immediately and wind down existing accounts by June. About 50 US jobs are gone. The move comes less than two months into new CEO Diana Layfield’s tenure, and it reads like a statement of intent: profitability over vanity geography.

The numbers tell you why.

Monzo has 15 million UK customers, £1.2 billion in revenue (up roughly 40% year-over-year), and an 8x jump in adjusted pretax profit. Its US operation, launched in 2020 via a banking partner and never granted its own charter, never scaled to anything resembling those economics. Monzo’s own language was unusually blunt: “a deliberate, strategic decision to focus on scaling in our home market and Europe and to step away from the US.”

Zoom out 🔎 The real unlock is the European banking licence Monzo secured from the ECB and Central Bank of Ireland in December 2025. That licence allows passporting across the EU from a single base, which is exactly the kind of regulatory moat the US never offered. Instead of fighting Chime, SoFi, and Varo on their home turf while burning cash on state-by-state compliance, Monzo can now replicate its UK playbook across a continent where it already understands the customer.

N26 learned the same lesson in 2021, though under more duress. Revolut is the lone European neobank still pushing hard into the US, applying for a full national bank charter in March 2026. If Revolut pulls it off, the divergence will be worth studying: one company betting on global breadth, the other on regional depth.

Both strategies are coherent, but Monzo’s is the one that doesn’t require years of losses to validate.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch for three things over the next 12 months. First, how fast Monzo moves from Ireland into broader EU markets. Second, whether Layfield uses the cleaned-up cost structure to accelerate IPO timing. Third, whether Revolut’s charter application actually clears, because if it stalls, Monzo’s decision will look less like discipline and more like the only rational play all along. Either way, everyone will win here.

ICYMI: Revolut is the most profitable FinTech on Earth, and it hasn’t even started lending yet 🤯📈 [unpacking the fee-income fortress that makes Revolut structurally different from every competitor, the lending optionality coiled inside that balance sheet, the regulatory dominoes now falling in sequence, and whether $75B is expensive or whether the market is about to find out it was way too cheap + more bonus reads on Revolut, how it’s leveraging AI & bonus deep dives into the latest financials of Nubank NU 0.00%↑, SoFi SOFI 0.00%↑, Robinhood HOOD 0.00%↑, and Coinbase COIN 0.00%↑ inside]

What else I’m watching

Visa & Ramp Automate Bill Pay with AI 🤖 Visa V 1.07%↑ and Ramp are launching agentic AI solutions to automate corporate bill payments, replacing manual processes with real-time controls and automation. Using Visa’s Intelligent Commerce and Trusted Agent Protocol, the AI agents aim to simplify fund access, management, and spending for global organizations. Ramp, which serves 50,000 corporate clients with a unified platform for cards, expense management, and bill payments, says the AI suite will enhance payment flexibility and spending oversight. ICYMI: Visa developed a credit card for AI and shipped it the same day stablecoins got their own payment standard 🤖💳 [what it is & why Visa is doing it, how it stacks with MPP and what to expect next + bonus deep dive into Visa’s latest financials, and how I turned Claude Cowork into my personal COO that does the work while I sleep]

Nium Issues Stablecoin Cards Globally 💳 Nium has launched a dual-network stablecoin card issuance platform, allowing businesses to spend digital dollar balances at hundreds of millions of merchant locations worldwide. The platform integrates with Visa and Mastercard via a single API, enabling seamless crypto-to-fiat conversion at the point of sale. Nium handles chain-of-conversion complexity, cross-border settlement, and compliance, reducing deployment time from months to days. ICYMI:

Solaris Cuts 20% Jobs for AI Shift 🤖 German fintech Solaris is laying off 20% of its workforce - 80 employees - as it pivots to an AI-native bank strategy. The cuts, announced alongside its transformation plan, follow a leadership overhaul led by CEO Steffen Jentsch and majority shareholder SBI Group. Jentsch acknowledged the difficult departures while emphasizing the company’s commitment to its AI-driven future. Solaris, which secured €140 million in Series G funding in early 2025, is reshaping its operations to align with its vision of Europe’s first AI-native bank. ICYMI:

💸 Following the Money

Franklin Templeton has agreed to buy 250 Digital to expand its cryptocurrency-investing offering. Upon closing, its new crypto arm will be called Franklin Crypto, with strategies focused on institutional investors.

Fintech startup from ex-Klarna vets Galdera raises €1.5M led by J12 and Antler.

A16z crypto led a $10M raise for startup The Better Money Company, which says it is developing the “critical missing connectivity layer” needed to make the stablecoin ecosystem function properly. ICYMI:

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Wow, what a week... How do you manage to do it?? Seriously - great work Linas.