Revolut’s $115B secondary share sale mints Europe’s first centicorn 🇪🇺🦄; Vinyl raised $20M to replace the fax machines that track every public share 📠💸

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Everything Anthropic Shipped in 2026: Every Claude Model, Agent, & Tool - And How to Actually Use Them 🤖 [29 Claude launches in 5 months. Most users missed half of them. Here’s every model, agent, and tool - with the playbook for each one]

Loop Engineering: How to Design AI Loops That Build, Ship, and Improve While You Sleep 🔁 [From a three-line bash script to multi-day Claude Fable 5 autonomy — everything founders, builders, and investors need to stop prompting agents and start designing the systems that prompt them]

The Complete Guide to Claude Dynamic Workflows 🤖 [From first principles to production: every workflow pattern, cost trap, and real-world use cases founders, builders, and investors need to master Anthropic’s most powerful Claude Code feature yet]

You’re Prompting Claude Fable 5 & Mythos 5 Wrong. You Have 10 Days to Fix That 🤖 [The complete Fable 5 playbook for founders, builders, & investors — 12 prompting patterns, the orchestrator architecture, effort economics, and everything you need built before free plan ends 22 June]

The Claude Finance Playbook: How CFOs Use AI to Build Models, Forecast Cash, and Close Books Faster 📊 [A practical guide to setting up Claude for real finance work, with battle-tested prompts optimized for Claude Opus 4.7]

Ex-OpenAI’s Aschenbrenner Bet $5.5B on AI Chips. Now He’s Betting $8.5B Against Them 💸 [Leopold Aschenbrenner’s AI hedge fund Situational Awareness went from pure AI long to 62% short semiconductors in one quarter. Here’s what changed and why the thesis still holds]

Visa and Mastercard’s Agentic AI payment platforms have a volume problem 🤖📊 [what it’s all about, why it matters & why payment titans have a volume problem here + bonus reads into other Visa & Mastercard’s agentic AI moves, & how Google wants to be the OS for all commerce inside]

OpenAI filed for its IPO because Anthropic filed first 🤑📈 [why listing after Anthropic could be critical, and why all eyes should actually be on SpaceX here + a closer look at the most dangerous IPO wave since 1999 & how OpenAI turned Codex into a Wall Street analyst inside]

Revolut’s secret ECB restrictions didn’t hurt the valuation. They will hurt the IPO 👀🔔 [what happened, why it didn’t hurt the valuation, but could hurt the IPO + bonus dive into Revolut’s latest financials, & deep dive into their AI model for money inside]

Coatue’s May 2026 Report: The $12 Trillion AI Bet and Who Ends Up on the Wrong Side 📊 [Coatue’s latest public markets report reveals the most extreme winner/loser split in tech stock history, a $12 trillion AI capex wave, and one brutal framework that predicts exactly who wins]

Anthropic Just Told AI Founders Exactly What to Build in 2026 🦄 [1 million conversations. 9 consumer AI domains. A full founder playbook - plus where Anthropic’s own products will and won’t compete]

The Top 100 AI & Tech Investors of 2026 💸 [The venture capitalists behind Anthropic, OpenAI, SpaceX, Stripe, and Revolut - who they are, what they’re backing now, and exactly how to reach them]

As for today, here are the 2 fascinating FinTech stories that are transforming the world of financial technology as we know it. This was yet another wild week in the financial technology space, so make sure to check all the above stories.

Revolut’s $115 billion secondary share sale mints Europe’s first centicorn 🇪🇺🦄

Following the money 💸 FinTech giant Revolut is about to become Europe’s first centicorn, and Klarna shareholders might want to look away.

The London-based fintech is preparing a secondary share sale at a valuation of up to $115 billion, a 53% leap from the $75 billion it commanded just in November 2025. Investor demand is already strong enough to push the deal well past its initial $750 million target. Wild, but not too surprising… 😳

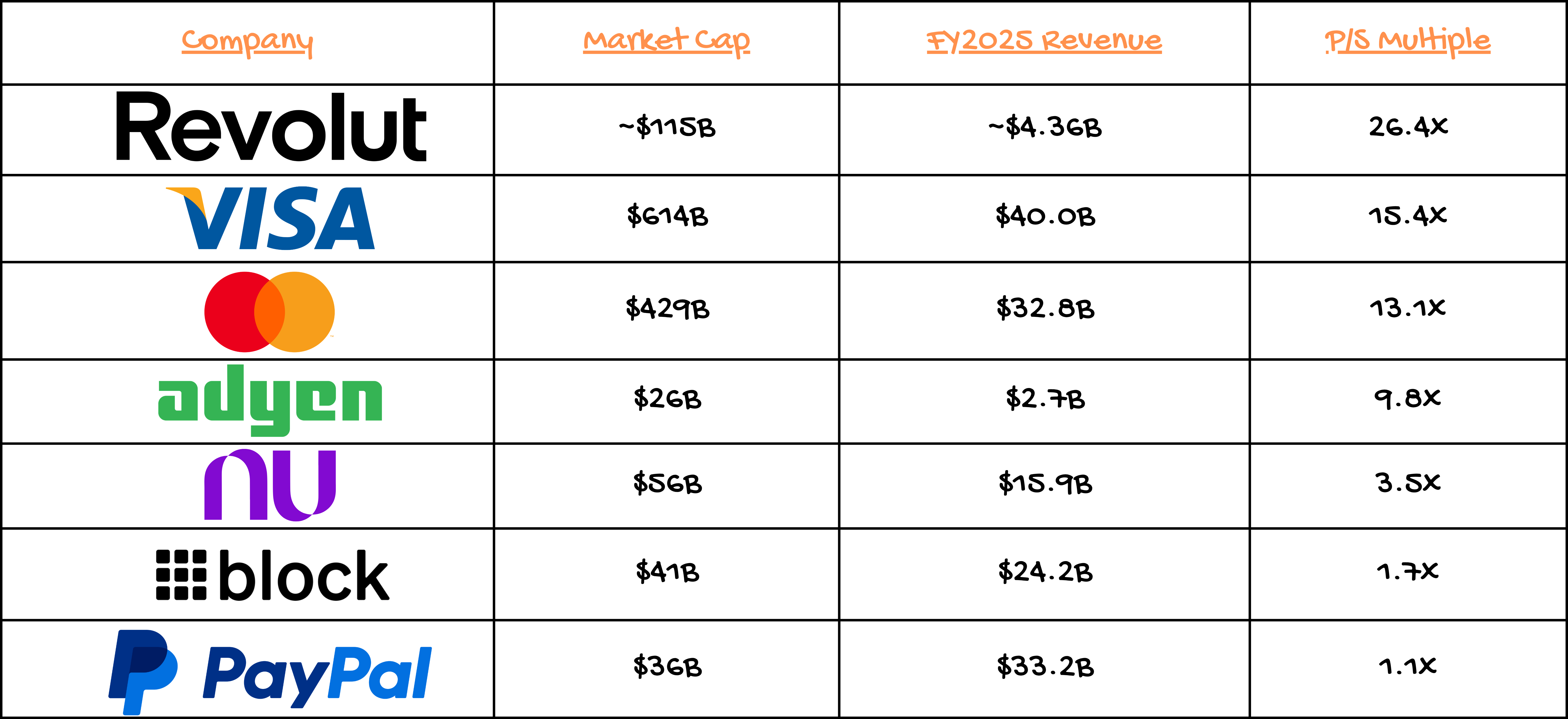

On the surface, the numbers tell a clean & impressive growth story: $6 billion in revenue, $2.3 billion in pre-tax profit, and a trajectory that would make Revolut the most valuable private fintech on the planet.

But underneath the centicorn milestone sits a messier picture involving a co-founder’s sudden departure, a high-stakes U.S. bank charter application, and the uncomfortable reality that the last European fintech IPO of this magnitude ended in a bloodbath.

Let’s take a closer look at this, understand why it matters, and what to watch next.

More on this 👉 The sale is set to launch June 15, led by Glade Brook, an existing backer also behind Stripe and Ramp. Firms are already lining up for $100 million-plus tickets, and demand is strong enough to double the offering to $2 billion. Closing is expected in July or August.

The financials clearly earn the enthusiasm.

→ Revenue grew 46% to $6 billion.

→ Pre-tax profit rose 57% to $2.3 billion.

→ At $115 billion, that’s roughly 19x revenue and 50x pre-tax earnings.

ICYMI: Revolut is the most profitable FinTech on Earth, and it hasn’t even started lending yet 🤯📈 [unpacking the fee-income fortress that makes Revolut structurally different from every competitor, the lending optionality coiled inside that balance sheet, the regulatory dominoes now falling in sequence, and whether $75B is expensive or whether the market is about to find out it was way too cheap + more bonus reads on Revolut, how it’s leveraging AI & bonus deep dives into the latest financials of Nubank, SoFi, Robinhood, and Coinbase inside]

To put this into perspective, Nubank trades around 3.5x; PayPal at just 1.1x.

The premium is obvious here, but so is the performance underneath it.

Zoom out 🔎 The timing, though, is complicated.

First and foremost, CTO and co-founder Vlad Yatsenko stepped down last week. This might have been inevitable, but still raises some questions. Then, we must remember that Revolut filed for a U.S. bank charter in March and installed a new U.S. CEO - a play that could double the addressable market or turn into a years-long regulatory grind. Oh, and Storonsky has said no IPO before 2028, meaning secondary buyers are committing to at least a two-year hold with no public exit.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, the first thing to watch is whether this secondary pushes past $2 billion. If it does, Revolut is building something quietly radical: a private-market liquidity machine that lets it function like a public company without listing. Employees get cash. Investors get price discovery. Management avoids the quarterly scrutiny that’s punishing Klarna, down more than 61% since its U.S. listing last year. Win-win!

On the other hand, the model has a shelf life. The cap table now includes T. Rowe Price, Fidelity, and Baillie Gifford, public-market investors with fund mandates and finite hold horizons. They didn’t write checks at $75 billion to sit in a private company indefinitely. Their presence is the clearest signal that an IPO is 18 to 24 months out, whatever Storonsky says about 2028. The U.S. bank charter is the swing variable. If Revolut gets it, the addressable market roughly doubles and $115 billion starts looking cheap. If the application stalls (and losing your technical co-founder during the most regulated phase of your expansion is not really cosmetic), the company remains a European fintech priced like a global one. Thus, for anyone writing a nine-figure check next month, the bet is that $115B is a discount to the IPO price, not a peak. After Klarna, that bet deserves more scrutiny than the demand suggests it’s getting.

ICYMI: Inside Revolut’s PRAGMA: The Foundation Model Trained on 40 Billion Banking Events 🧠 [Architecture, performance benchmarks vs. Stripe, Mastercard, and Visa, regulatory risks, and why PRAGMA may be the most consequential AI bet in consumer finance]

Monzo’s 2026 financials: the £1.7 billion revenue machine that still has to prove it can escape the UK’s Orbit 🏦🇬🇧 [breaking down the unit economics that matter, the Revolut comparison investors keep getting wrong, the governance drama, IPO chances & what’s next for Monzo + bonus deep dive into Revolut’s latest financials & their foundational AI model for money inside]

Starling Bank’s 2026 financials: 2.5x Monzo’s profit on half the revenue, and a £70M SaaS pipeline that changes the IPO math 📈🧠 [unpacking the most important financial facts & figures, how it stacks against Monzo & Revolut, & why Starling’s balance sheet is a fortress + bonus deep dives into the latest financials of Monzo & Revolut inside]

Vinyl raised $20M to replace the fax machines that track every public share 📠💸

Following the money 💸 The legal record of who owns what on Wall Street still runs on mainframes, batch processing, and fax machines. On June 9, Jump Capital bet $20 million that it doesn’t have to.

Let’s take a quick look at this.

More on this 👉 Vinyl Equity, a Chicago-based, SEC-registered transfer agent founded in 2022 by Rob Schoder (ex-AngelList) and Poornaprajna Udupi, closed its Series A with MUFG Innovation Partners joining and Index Ventures, Spark, Infinity Ventures, and Cambrian Fintech all re-upping after a roughly $12 million seed in April 2025.

The company is rebuilding shareholder recordkeeping as cloud-native, API-first software.

The incumbents here (Computershare, Equiniti/AST, Broadridge) impose costs that are specific and measurable: restricted share transfers drag on for weeks, quarterly DWAC fees reach $25,000, and routine shareholder inquiries get routed to outside counsel billing up to $1,500 an hour. Vinyl clears restricted shares in minutes, eliminates the medallion signature guarantee requirement, and connects directly to equity plan administrators so vested shares issue without manual reconciliation.

Traction is early but tangible: 40,000+ transactions, 65,000+ registered holders, and Neptune Insurance retaining Vinyl as agent through its NYSE listing. The market is worth roughly $14.8 billion today and is projected to nearly double by 2034. Not too shabby!

Zoom out 🔎 The signal in this round is all about MUFG. A megabank doesn’t invest in back-office infrastructure on a whim. Recent SEC guidance now permits transfer agents to maintain their master ledger on-chain, making the agent of record the natural bridge if public equities tokenize.

Mainframes can’t make that leap. Vinyl was architected assuming they wouldn’t have to.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, the bear case is obvious here: if tokenization stalls, Vinyl is a faster, cheaper transfer agent in a fee-compressed niche. A solid business, but maybe not a venture-returner on $30M+ in funding. The bull case is that the ownership ledger becomes the API layer for programmable corporate actions, and whoever controls it controls everything downstream. That said, watch IPO mandates over the next twelve months. Incumbents will defend on bundled pricing rather than better product, and issuer conservatism is the real barrier here, as nobody gets fired for picking Computershare. Finally, the effect most people will miss is that cheaper transfer agency marginally lowers the cost of staying public, a small tailwind that a somewhat sluggish (but very exciting!) IPO pipeline genuinely needs.

ICYMI: OpenAI filed for its IPO because Anthropic filed first 🤑📈 [why listing after Anthropic could be critical, and why all eyes should actually be on SpaceX here + a closer look at the most dangerous IPO wave since 1999 & how OpenAI turned Codex into a Wall Street analyst inside]

🧠 What else I’m watching

BBVA AWS AI Boost ⚡ BBVA has partnered with AWS to deploy an MLOps framework within its ADA platform, automating AI model development, testing, and deployment. The architecture, supporting 6,500+ users including 1,000 data scientists, has cut development times by 20–75% and operational costs by 40–55% in pilot projects like personalized recommendations. It also automates validation and maintains audit trails for secure, scalable AI solutions. ICYMI:

Monzo Inclusive Credit Card 💳 Monzo and Fair4All Finance are piloting a new Flex Build credit card, allowing UK customers with low or limited credit scores to access up to £250 via a small deposit. Users pay 0% interest if balances are settled monthly, with missed repayments triggering spending freezes. On-time payments unlock higher limits and deposit returns. Fair4All Finance provides a £7 million lending guarantee, sharing risk with Monzo. The partnership aims to improve financial inclusion, helping customers build credit histories and transition to mainstream borrowing options. ICYMI: Monzo’s 2026 financials: the £1.7 billion revenue machine that still has to prove it can escape the UK’s Orbit 🏦🇬🇧 [breaking down the unit economics that matter, the Revolut comparison investors keep getting wrong, the governance drama, IPO chances & what’s next for Monzo + bonus deep dive into Revolut’s latest financials & their foundational AI model for money inside]

ING AI Mortgage Speed 🏠 ING is scaling its agentic AI assistant to accelerate mortgage decisions in the Netherlands, following a March pilot. The AI analyzes applications, explains outcomes, and suggests next steps, while ING staff retain final decision-making authority. The gradual rollout aims to create a faster, more consistent mortgage experience. ICYMI:

💸 Following the Money

AI-native banking platform Titan secures $3M in new funding.

Elon Musk’s rocket builder SpaceX is set to allocate up to a quarter of its $75B float to retail investors.

Lloyds and Nationwide-backed AI fintech Aveni raises £12M. ICYMI:

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Isn't Revolut overvalued?

great read as always - thanks Linas, it's my favourite Sunday piece!