The 2035 Global Intelligence Crisis 🌍🧠

The most dangerous AI prediction isn't the one that went viral 🧨

👋 Hey, Linas here! Welcome to another special issue of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & the most important money movements, it’s the only newsletter you need for all things when Finance meets Tech. If you’re reading this for the first time, it’s a brilliant opportunity to join a community of 370k+ FinTech leaders:

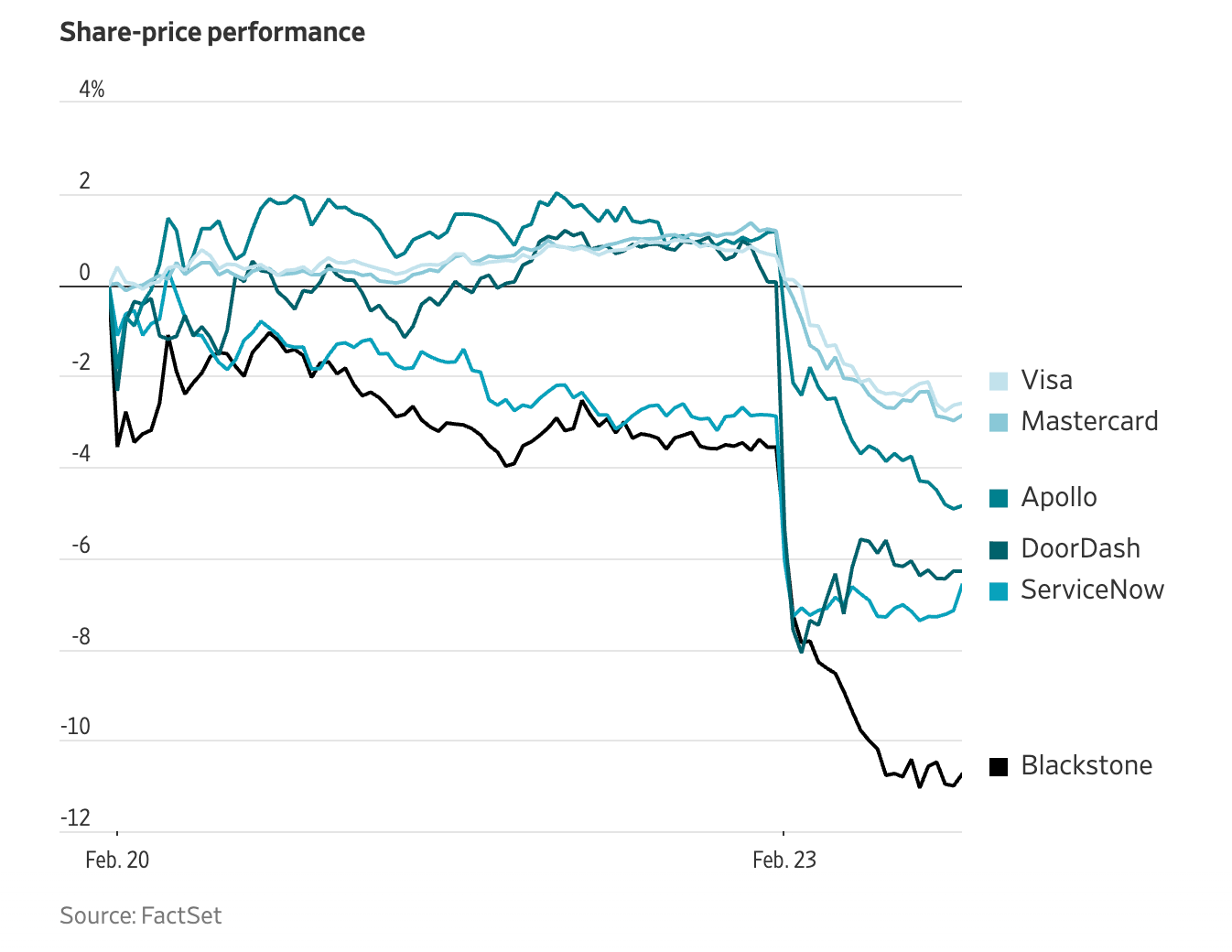

A piece of speculative fiction published on Substack on February 22 moved the Dow 821 points. DoorDash fell 6.6%. IBM dropped nearly 13%. KKR lost 9%. Legendary Michael Burry shared it with the comment, “And you think I’m bearish.” 16 million people read it on X. Bloomberg, WSJ, Fortune, CNN, and at least a dozen other outlets covered it by the end of the day.

Citrini Research’s “The 2028 Global Intelligence Crisis” is written as a memo from June 2028, looking back at how AI broke the American economy. Companies replace white-collar workers with AI agents, those workers stop spending, the consumer economy withers, private credit defaults cascade through insurance balance sheets, and the S&P 500 falls 38% from its highs. The authors call it the “Intelligence Displacement Spiral,” a feedback loop with no natural brake.

The piece earned its audience. But the scenario it describes requires economic transformation at 10-12x the pace of any historical precedent, while every natural countervailing force fails simultaneously.

The two-year timeline is not a minor modeling choice. It is the difference between a crisis and a transition. And the transition scenario, the one where GDP keeps growing while the median worker quietly loses ground for a decade, is both far more likely and far harder to prepare for.

The viral version of AI risk is crowding out the version that actually demands attention.

What the Piece Gets Right

Let’s start off with what deserves credit, because several things do.

“Ghost GDP” is a genuinely useful concept. A GPU cluster in North Dakota producing the output previously attributed to 10,000 workers in Manhattan generates GDP without generating the restaurant visits, apartment leases, and income tax revenue those workers produced. Output that shows up in national accounts but never circulates through households. The framing captures something real about the risk of AI-driven productivity gains concentrating at the top of the income distribution, while the metrics everyone watches keep looking fine.

The observation that companies most threatened by AI become its most aggressive adopters is sharp too. If your competitor is cutting headcount with AI and undercutting your prices, you adopt AI too, whether it works well or not. The cycle is self-reinforcing even before the technology matures.

The financial plumbing section is arguably the piece’s strongest analytical contribution. PE-backed software LBOs defaulting, cascading through life insurer balance sheets, exposing Bermuda reinsurance structures: each link in the chain is plausible and well-researched. The structural opacity the piece describes, with PE-owned insurers holding PE-originated credit through offshore reinsurance vehicles, is real and already attracting regulatory attention from the NAIC and state insurance regulators. The scenario is directionally correct, and this is where financial risk could be hiding.

The seat-based revenue reflexivity is a second-order effect most analyses miss. If your SaaS product is priced per seat and your customers are cutting headcount, your revenue declines even if no customers cancel. You don’t need wholesale replacement of the product to get margin compression. You just need your customers to need fewer humans. More about this here:

And the procurement dynamic is already real. The Citrini piece describes a Fortune 500 procurement manager telling a vendor he’d been talking to OpenAI about replacing them with AI tools (that’s exactly what OpenAI wants in the end; more on this below). The vendor renewed at a 30% discount. That anecdote rings true not because the AI replacement is imminent, but because the threat of it is sufficient to shift bargaining power. Even vaporware exerts pricing pressure if the buyer believes it might work 🤷♂️

The Speed Problem

Every financial domino in the piece requires the same thing: that all of this happens within two years. From the opening paragraph, the piece sets its clock: “Two years. That’s all it took.” The scenario needs mass white-collar layoffs, an S&P peak, and 38% decline, agentic commerce displacing major consumer intermediaries, stablecoin settlement routing around card interchange at scale, private credit defaults cascading into insurance sector distress, a housing downturn concentrated in tech hubs, and a policy apparatus too paralyzed to respond. All by mid-2028.

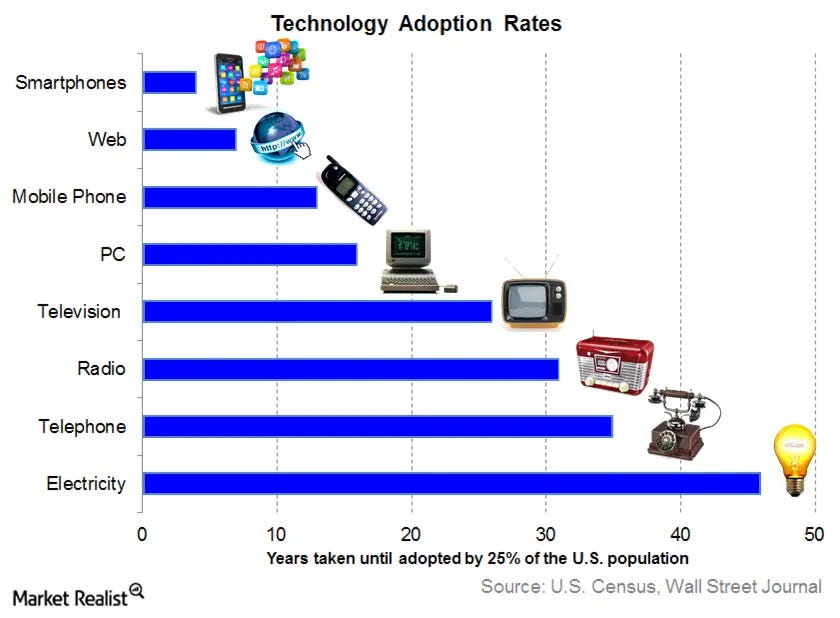

There is no precedent for this speed of structural transformation. None.

E-commerce took from 1995 to 2010 to reach 5% of U.S. retail sales. Fifteen years from commercial availability to a 5% share. It took until 2019 to reach 11%. The smartphone, perhaps the fastest consumer technology adoption in history, took roughly 5 years from the iPhone’s 2007 launch to reach majority market penetration. And the smartphone required no changes to corporate IT infrastructure, procurement cycles, or regulatory frameworks.

The authors are aware of this objection. They preempt it by arguing that AI is fundamentally different from prior technologies because it improves at the tasks humans would redeploy to. The point has force. But it confuses the rate of AI capability improvement with the rate of economic and institutional (& even consumer) adoption, which are different things entirely.

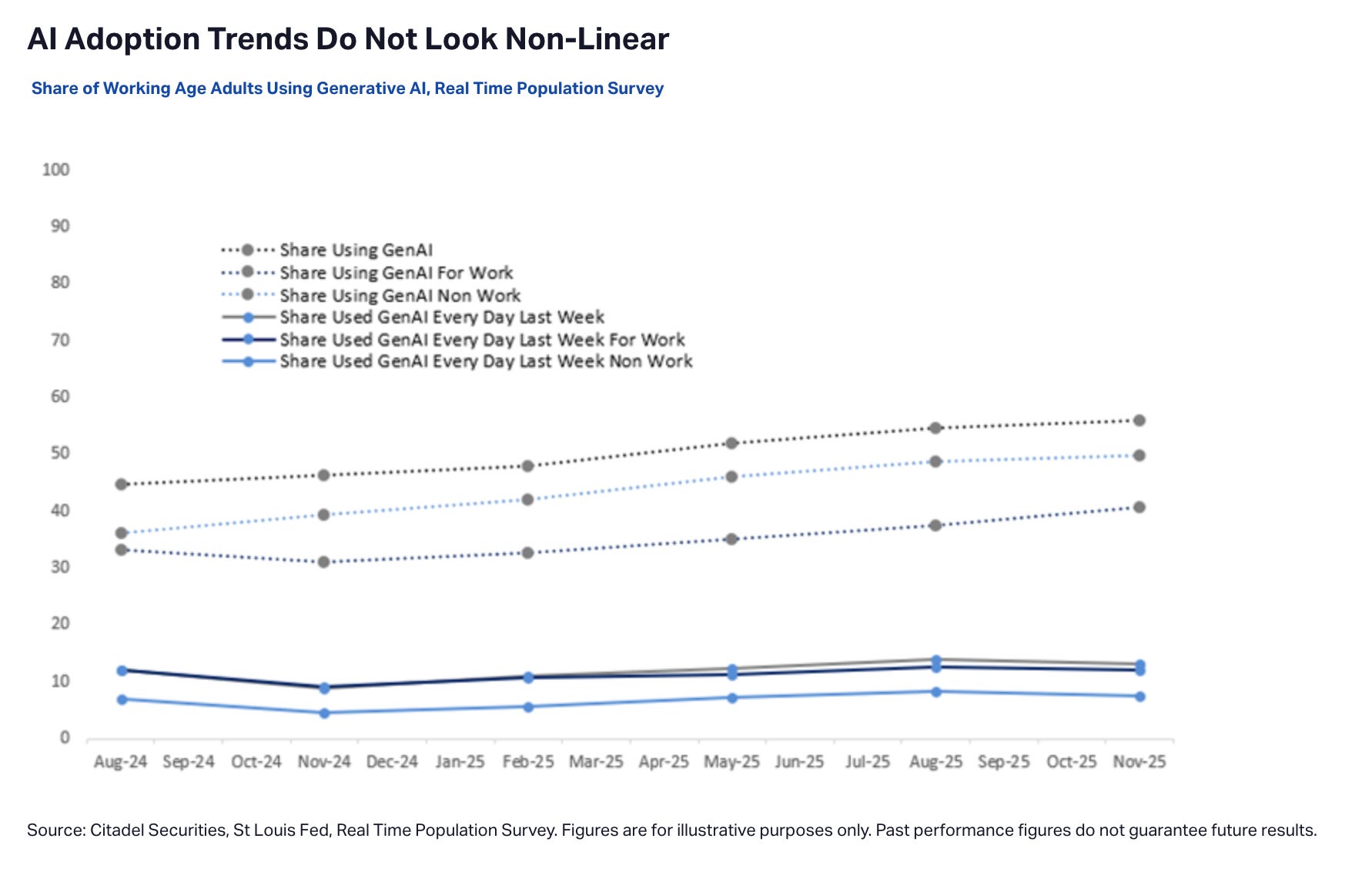

Citadel Securities published a rebuttal that drives this distinction home with data.

→ The St. Louis Fed’s Real-Time Population Survey tracks how intensely Americans use AI for work. If AI displacement were imminent, the data would show an inflection upward in daily use. Instead, it shows unexpectedly stable curves.

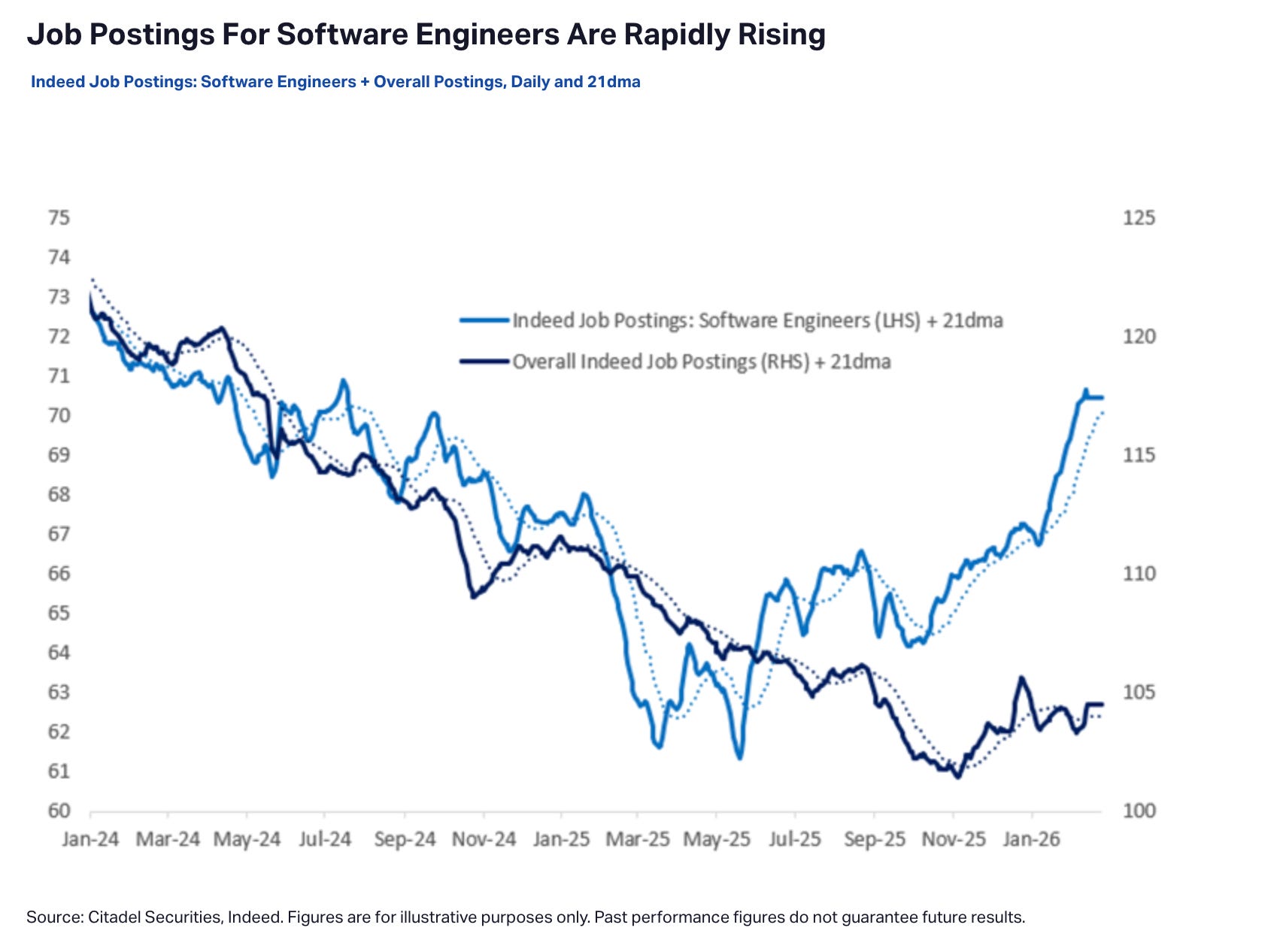

→ Job postings for software engineers are up 11% year-over-year.

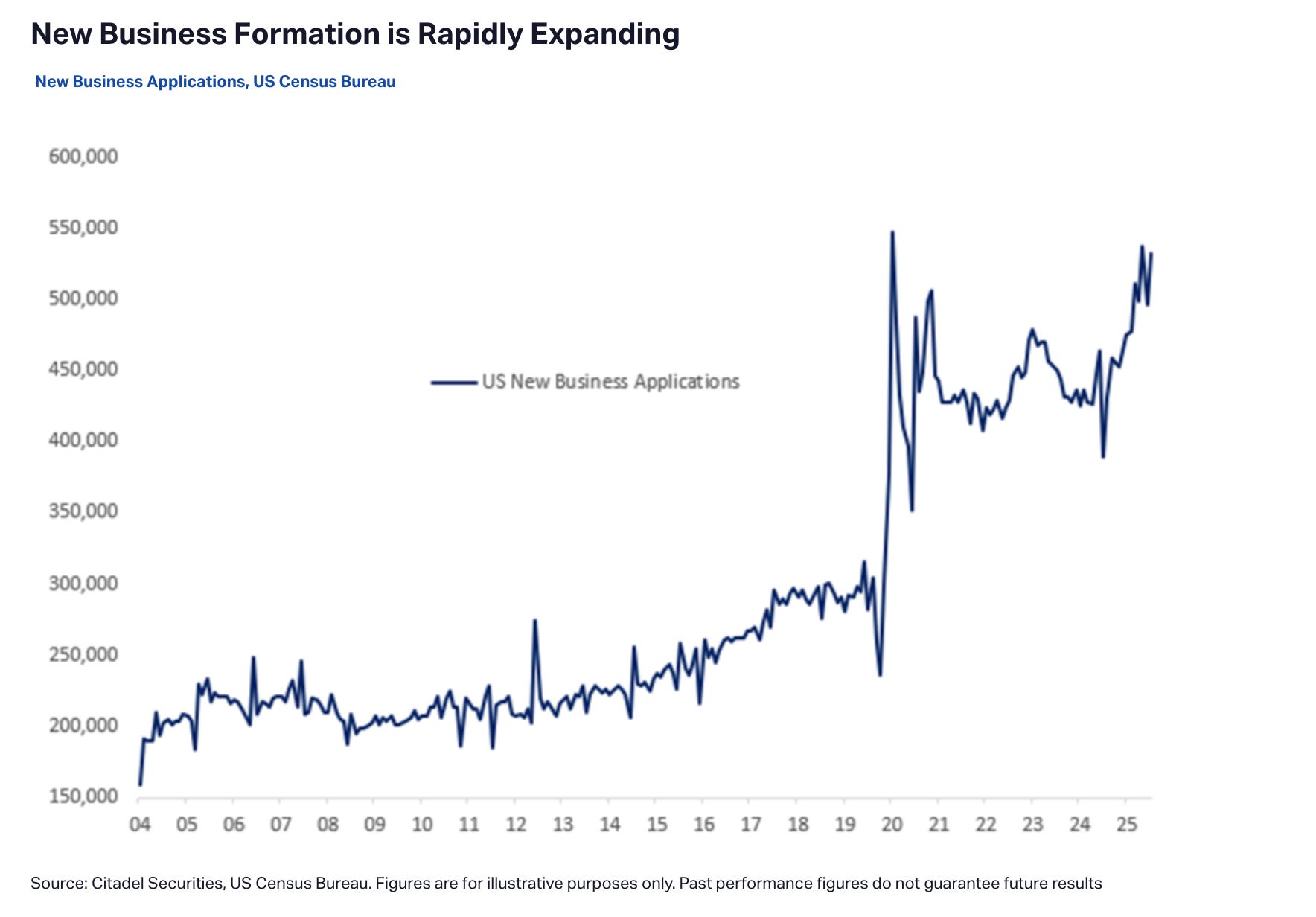

→ New business formation is expanding rapidly. The macro picture in February 2026 looks nothing like the preconditions for the crisis described.

More importantly, enterprise software adoption moves at the speed of budget cycles, legal review, integration timelines, and institutional risk tolerance. The piece acknowledges that “fiscal years mostly line up with calendar years, so 2026 enterprise spend had been budgeted in Q4 2025.” It then needs companies to observe, evaluate, and act on agentic AI within a single budget cycle.

Some will. Most won’t. The gap between “a competent developer can replicate a mid-market SaaS product in weeks” and “a Fortune 500 CIO decides to cancel a mission-critical vendor contract and rebuild in-house” is enormous. It involves legal risk, security review, compliance, integration with existing systems, ongoing maintenance liability, and the career risk of the executive who signs off.

As Citadel’s Frank Flight put it: recursive technology does not equal recursive adoption. Even if algorithms improve at exponential rates, economic deployment remains bounded by physical capital, energy availability, regulatory approvals, and organizational change.

The Brakes That Exist

The centerpiece of the analytical framework is the “feedback loop with no natural brake.” AI gets cheaper, companies cut workers, workers spend less, margins compress, and companies buy more AI. The authors contrast this with normal recessions, where cyclical mechanisms contain the seeds of their own recovery.

The argument is internally elegant. It is also wrong about having no brakes. There are at least three.

The first is demand-driven. The authors’ counter is that AI spending is OpEx substitution, not CapEx expansion: a company shifts from $100M on employees and $10M on AI to $70M on employees and $20M on AI. The AI budget grows, but total spending falls. The problem with this framing is that it only works at the individual firm level. At the macro level, if consumer spending is collapsing and revenue is falling, the total budget available for any spending shrinks. A company whose revenue has dropped 20% because its customers have been laid off does not maintain its AI budget at $20M. It cuts everything. The deflationary spiral, if it materializes, is not selective about which line items it compresses.

The second is the government. The piece describes a political apparatus that is “confused,” mired in partisan bickering, and too slow to respond. This is a political prediction dressed as an economic argument, and a conveniently pessimistic one. The United States deployed roughly $5 trillion in fiscal stimulus during COVID-19 within months of the crisis emerging. The CARES Act was passed in March 2020. Enhanced unemployment benefits, stimulus checks, and PPP loans followed quickly. A 10.2% unemployment rate concentrated among white-collar professionals in major metros, the exact demographic that drives media coverage and political engagement, is precisely the kind of crisis that generates political will. The piece describes both the political motivation for intervention and the absence of intervention. It cannot have both.

The third is new economic activity. The piece models AI exclusively as labor substitution: the same economy minus humans. It never accounts for what abundant intelligence might create. Not in the speculative, hand-wavy sense of “new jobs we can’t imagine,” but in the concrete sense of what happens when the cost of producing software, analysis, and creative work falls by an order of magnitude. When the cost of a factor of production collapses, demand for the activities that factor enables expands. Cheaper software means more software gets built. Cheaper analysis means more decisions are informed by analysis. The piece treats AI as a fixed-pie redistributor. The history of technology tells a different story.

Citadel’s rebuttal invoked a useful historical parallel. In 1930, Keynes predicted that productivity growth would reduce the workweek to 15 hours by the early twenty-first century. He was right about productivity growth and profoundly wrong about its consequences. Rather than working dramatically less, societies consumed dramatically more. Preferences shifted toward higher-quality goods, new services, and forms of expenditure that did not exist in 1930. Keynes underestimated the elasticity of human wants. The Citrini piece may be making the same mistake a century later.

The Sectoral Weak Points

The piece’s treatment of specific industries is where the analytical cracks are perhaps the widest.

The DoorDash DASH 0.00%↑ argument confuses the technical barrier to entry with the actual moat. The piece claims coding agents collapsed the barrier to launching a delivery app and that competitors offered drivers 90-95% of the delivery fee. But the technical barrier, building the app, was never the moat. The moat is the two-sided marketplace: density of restaurants, density of drivers, and density of consumers, all in the same geography, generating enough order volume to make the unit economics work. You can build a DoorDash, Uber UBER 0.00%↑, Bolt clone in weeks. You cannot build a two-sided marketplace with sufficient density in weeks. In logistics, the moat is physical networks of drivers, kitchens, and last-mile execution, not software.

The stablecoin payments scenario is the most falsifiable claim in the piece. It describes AI agents settling consumer transactions via USDC on Solana or Ethereum L2s at a fraction of a penny versus the traditional 2.5% card fee. For this to matter at the described scale within 12-18 months, you need nearly all merchants accepting stablecoin settlement, the majority of consumers funding stablecoin wallets, regulatory frameworks permitting autonomous agent-initiated financial transactions across the globe, and trust infrastructure for AI agents to hold and transfer monetary value on behalf of consumers. None of this exists yet. Building it requires regulatory clarity that does not exist, consumer trust that has not been really established, and merchant adoption that has no precedent at the speed described. U.S. consumers also actively want the features that card rails provide: chargebacks for fraud, purchase insurance, extended warranties, and 1-5% cash-back rewards.

Stablecoins offer none of these reliably. The idea that agents will route a meaningful share of consumer transactions through stablecoin rails within 18 months is not a conservative extrapolation from current trends.

The travel intermediation argument has similar problems. Modern aggregators like Skyscanner, Kayak, and Google Flights already employ AI for dynamic pricing and itinerary optimization. They integrate deeply with airlines and hotels via APIs, securing bulk deals and opaque fares unavailable to ad-hoc agents. An AI agent “finding a cheaper deal” would query these same platforms, routing business back to them. Travel’s friction is not just search. It is refunds, changes, insurance, and human judgment on disruptions. Reports from multiple sources show agentic systems achieving longer autonomous runs in some coding tasks but requiring human verification in a majority of decisions for reliability. High-stakes travel bookings involve the kinds of edge cases that agents handle poorly without oversight.

The Math That Doesn’t Add Up

The spending math the piece builds on is oversimplified in ways that favor its conclusion. The authors claim white-collar workers “represented 50% of employment and drove roughly 75% of discretionary consumer spending.” The 50% figure is roughly consistent with BLS data. The 75% figure is not sourced and conflates two different things: white-collar employment and high-income spending.

The piece later states that “the top 10% of earners account for more than 50% of all consumer spending.” This is approximately consistent with Federal Reserve data. But it then treats “white-collar workers” and “top income deciles” as the same population. They are not. A white-collar worker earning $55,000 as an administrative coordinator is not in the top 10% of earners. The overlap is real but not total. The distinction matters because the piece’s financial contagion mechanism depends on the highest-earning cohort being the same cohort that gets displaced. In practice, the first wave of AI-driven displacement is more likely to affect mid-level knowledge workers, not the senior professionals and executives who drive the top-decile spending figures.

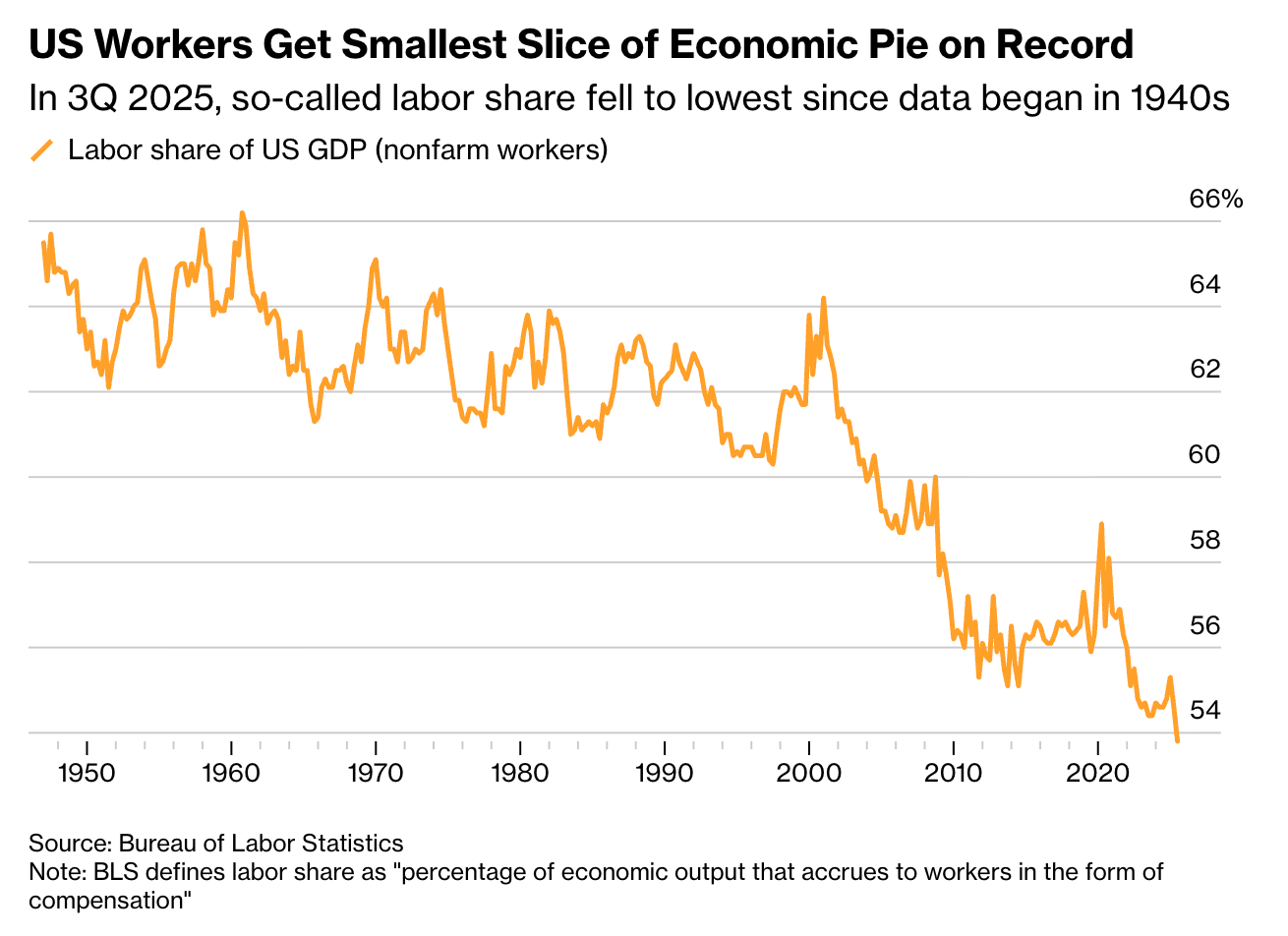

The projected drop in labor’s share of GDP, from 56% to 46% in four years, deserves scrutiny too. BLS data shows the prior 10-percentage-point decline in labor share took approximately 50 years. The scenario requires the pace of erosion to accelerate by roughly 12x. Even accepting that AI is a step-change in the rate of labor substitution, a 12x acceleration in a macroeconomic indicator that reflects the combined behavior of millions of firms and hundreds of millions of workers is an extraordinary claim. The piece presents it in a single sentence without defending it.

The Prediction That Should Keep You Up at Night

Here is the uncomfortable truth: the Citrini piece is wrong about 2028, but it may be directionally right about 2035. And the version of AI risk that plays out over a decade is harder to prepare for than the version that arrives as a crisis.

A crisis triggers a response. COVID-19 produced $5 trillion in fiscal stimulus within months. The 2008 financial crisis produced Dodd-Frank within two years. Crises are legible. They concentrate political attention. They create the conditions for their own resolution.

A slow grind does not trigger a response. If GDP keeps growing at 2-3% while the median worker quietly loses ground, the political system has no crisis to respond to. If the S&P keeps rising because corporate margins are expanding through labor substitution while household income stagnates, the metrics that everyone watches keep looking fine. If unemployment ticks up 1-2 points over five years instead of spiking to 10% in two, it stays below the threshold that generates political will.

The real risk from AI-driven labor displacement is thus not a deflationary spiral that crashes the S&P 38% in two years. It is a decade-long transition where productivity gains flow primarily to capital while labor’s share of income continues its long decline. Where GDP and profits rise, but households, cut out of the loop, lose purchasing power so gradually that it never registers as an emergency. Where new business formation accelerates, but the new businesses employ fewer people at lower wages. Where the economy adapts, but the adaptation looks like a permanent shift in who captures the gains from growth.

The BLS data on labor share already tells this story in slow motion. Labor’s share of GDP declined from roughly 64% in 1974 to 56% in 2024. A 50-year grind lower that happened slowly enough that it never produced a political crisis sufficient to reverse it. AI could accelerate that trend without producing the kind of dramatic rupture that forces institutional response.

SaaS pricing pressure is a real and present example. The procurement anecdote in the Citrini piece, the 30% discount extracted by threatening AI replacement, is more representative of the likely near-term dynamic than wholesale contract cancellation. But a 30% discount across the software industry, sustained over several years, still produces meaningful revenue compression, job losses at software companies, and reduced consumer spending by the workers displaced. It just happens slowly enough that no single quarter triggers an alarm.

The private credit-insurance nexus is a genuine risk worth monitoring, not because it will produce a systemic crisis by 2028, but because the structural opacity it contains (PE-owned insurers holding PE-originated credit through offshore reinsurance vehicles) creates the conditions for losses to accumulate unobserved until they are too large to manage gracefully. The lesson of 2008 is not that financial crises arrive on schedule. It is that they arrive after risks have been building in places where nobody was looking.

What to Watch

The Citrini piece will be tested by reality, slowly and unevenly. Three signals matter most.

First, SaaS renewal rates over the next four quarters. If enterprise customers begin using AI alternatives as real bargaining power in negotiations, and if that pressure translates into measurable revenue compression at mid-market software companies, the directional argument gains force even if the timeline is wrong by years. Watch the earnings calls and reports of companies like ServiceNow NOW 0.00%↑, Zendesk, and HubSpot HUBS 0.00%↑. The language will shift from “AI as a growth driver” to “AI-related pricing pressure” before the revenue numbers move.

Second, white-collar hiring data. If the BLS begins showing sustained declines in professional and business services employment while overall employment holds steady, the distributional concern moves from theory to fact. The monthly jobs report won’t capture this cleanly. Look at the BLS Quarterly Census of Employment and Wages for industry-level granularity, and watch Indeed and LinkedIn posting data for forward-looking signals.

Third, the composition of new business formation. The U.S. Census Bureau data on new business applications is running at elevated levels. If new businesses are forming but employing fewer people per firm than historical averages, the expansion in business creation is masking a contraction in the labor intensity of the economy. More businesses, fewer jobs per business, same or lower total employment.

Concluding Thoughts

The Citrini piece triggered a sell-off because the anxiety it organized was already there, waiting for a narrative.

That anxiety is not irrational. AI will ultimately displace some or parts of most white-collar work, compress margins in intermediation businesses, and shift the distribution of economic gains toward capital. But the form the disruption takes matters as much as the direction.

A two-year crisis produces an emergency response. A ten-year transition produces resignation. The version of AI risk that goes viral is the one with the dramatic timeline and the 38% crash.

The version that should concern investors, policymakers, and workers is the one that never triggers a crisis at all.

And that’s not it. In case you missed it, check out these resources as well:

And that’s a wrap.

In 2023, I started sharing resources to help you become a more successful entrepreneur, investor, or business leader. I hope you will find this new piece valuable too.

Keep dreaming & keep building.

If you found this useful, share it with others and spread the word:

Disclaimer: This newsletter is provided for informational purposes only and should not be relied upon as investment, financial, legal, or tax advice. Nothing in this publication constitutes a recommendation to buy, sell, or hold any security, nor does it constitute an offer or solicitation of an offer to buy or sell any security or financial instrument. The author may hold positions in securities mentioned in this newsletter and is under no obligation to disclose such positions or to notify readers of any changes to them. All opinions expressed are the author’s own and are subject to change without notice. This content may reference third-party sources, publicly available filings, and market data; while efforts have been made to ensure accuracy, the author makes no representations or warranties as to the completeness or reliability of such information. Past performance of any investment, strategy, or index discussed is not indicative of future results. You should conduct your own research and consult with a qualified financial adviser before making any investment decisions.

Love your take on this Linas! It is scary that the slow burn is the harder one to respond to versus a 2 year crisis picture.

This is great - informative, clear and objective. Thank you for sharing this! That said, what we, the regular people, should do then? 🤔