Ramp just gave accountants Free AI to get at their clients 🤖📊; Anthropic made the EU come asking for Claude Mythos 😳🇪🇺; Stripe, Visa, Mastercard, & Coinbase could launch a stablecoin 😳🪙

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Everything Anthropic Shipped in 2026: Every Claude Model, Agent, & Tool - And How to Actually Use Them 🤖 [29 Claude launches in 5 months. Most users missed half of them. Here’s every model, agent, and tool - with the playbook for each one]

The Complete Guide to Claude Dynamic Workflows 🤖 [From first principles to production: every workflow pattern, cost trap, and real-world use cases founders, builders, and investors need to master Anthropic’s most powerful Claude Code feature yet]

Claude Opus 4.8: The Complete Prompting Playbook for 2026 🧠 [How to get the best results from Anthropic’s most powerful model every single time, including the new Dynamic Workflows feature]

The Claude Finance Playbook: How CFOs Use AI to Build Models, Forecast Cash, and Close Books Faster 📊 [A practical guide to setting up Claude for real finance work, with battle-tested prompts optimized for Claude Opus 4.7]

Ex-OpenAI’s Aschenbrenner Bet $5.5B on AI Chips. Now He’s Betting $8.5B Against Them 💸 [Leopold Aschenbrenner’s AI hedge fund Situational Awareness went from pure AI long to 62% short semiconductors in one quarter. Here’s what changed and why the thesis still holds]

Robinhood’s Q1 2026: the best brokerage, the wrong price 🤷♂️💸 [breaking down the most important facts & figures from Robinhood’s Q1 2026 to see whether Robinhood is worth your time & money + bonus deep dive into the latest financials of its bigget competitor Coinbase, and why Robinhood’s Agentic AI play is exactly what Anthropic recently told AI founders to build in 2026]

OpenAI’s Codex just became a Wall Street analyst, and the moat belongs to FactSet & Moody’s 🤖📊 [what OpenAI exactly shipped and why it matters, how this hands the durable moat to companies most people aren’t even watching, and the 4 shifts we’d bet on over the next 2 years + bonus deep dives into OpenAI’s Super App strategy & how Anthropic just told AI founders exactly what to build in 2026 inside]

Anthropic has lapped OpenAI just in time to lead the most dangerous IPO wave since 1999 😳🔔 [why it matters & why it’s critical that the Claude maker IPOes before OpenAI & why you should in fact watch SpaceX the closes here + bonus dive into everything Anthropic shipped in 2026 so far & how to actually use it]

Coatue’s May 2026 Report: The $12 Trillion AI Bet and Who Ends Up on the Wrong Side 📊 [Coatue’s latest public markets report reveals the most extreme winner/loser split in tech stock history, a $12 trillion AI capex wave, and one brutal framework that predicts exactly who wins]

Anthropic Just Told AI Founders Exactly What to Build in 2026 🦄 [1 million conversations. 9 consumer AI domains. A full founder playbook - plus where Anthropic’s own products will and won’t compete]

As for today, here are the 3 incredible FinTech stories that are transforming the world of financial technology as we know it. This was yet another solid week in the financial technology space, so make sure to check all the above stories.

Ramp just gave accountants Free AI to get at their clients 🤖📊

The news 🗞️ FinTech giant Ramp just launched Ramp Stack, and the most telling fact here is the price. It’s free through August, and that should tell you the software was never the point.

Let’s take a closer look at this.

More on this 👉 On June 3, Ramp launched Stack, an AI system aimed not at the in-house finance teams it has served for six years but at the accounting firms that serve everyone else.

Agents Ramp calls Coworkers run the mechanical work of the monthly close across a firm’s whole book of clients: reconciliations, journal entries, transaction coding, variance analysis. Firms describe a client’s process in plain English, Stack encodes it as reusable Skills, and nothing posts to QuickBooks without human sign-off.

Design partners report closes 50% to 60% faster and reconciliations up to 9x faster, with one firm’s March close dropping to about 20 minutes. Not too shabby! On an independent benchmark of 200-plus accounting tasks graded by working accountants, Stack hit a 65.8% success rate and beat every general-purpose model tested. Nice!

Zoom out 🔎 The accounting work is real, but it isn’t where Ramp makes money. The asset is the data. Ramp already runs spend, accounts payable, and banking data for tens of thousands of businesses, so its agents work on the live numbers instead of reaching through connectors the way Pilot, Zeni, or Intuit’s own QuickBooks agents have to.

The firms are thus the channel. More than 4,500 already use Ramp, 92 of the top 100 CPA firms have clients on the platform, and firms decide which financial stack their clients adopt. Make a firm faster and more dependent on Ramp’s rails, and you pull its downstream clients onto the cards and bill-pay where Ramp’s revenue actually lives. Win-win. Thus, free through August is the giveaway, because the monetization sits downstream.

We also have to talk about the timing here, because it explains the rest.

Ramp is reportedly raising about $750M at a $40B-plus valuation, near 40 times revenue, with IPO-readiness targeted for late 2026. A multiple like that needs a bigger market than corporate-card spend, and the $150B accounting industry is one Ramp had never sold a product into. The staffing crisis also hands it a willing audience: more than 300,000 accountants have left the field and degrees sit at a 20-year low, so firms are turning away clients they can’t staff.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, the collision to watch here is Intuit. QuickBooks is both the launch integration and a competitor building its own agents, which makes them partners today and rivals tomorrow. The squeeze lands hardest on pure-play AI accounting startups like Basis, fresh off a $100M raise at $1.15B, who own no source data and must knock on doors Ramp walked through years ago. The second-order effect most will miss is what Stack does to private equity’s accounting roll-up: it offers firms the centralized delivery of a consolidator without selling, which could cool a wave that has absorbed roughly $50B in six years. That said, I’d watch two things - whether free converts to paid, and whether the native-data edge survives once Xero and NetSuite arrive.

ICYMI:

Anthropic made the EU come asking for Claude Mythos 😳🇪🇺

The news 🗞️ The bloc that writes the rulebook for American tech just flew to San Francisco to ask a private company for a favor. And it’s not a small one…

Let’s unpack this.

More on this 👉 Anthropic told the European Commission over the weekend that it would let ENISA, the bloc’s cybersecurity agency, into Project Glasswing - the restricted program where a handful of organizations test Mythos before any broad release. ENISA confirms the offer but says conditions aren’t settled.

The move makes the EU the first entrant outside the US and UK, joining a club that until now meant Microsoft, Apple, JPMorgan, CrowdStrike, several US government departments, and the UK’s AI Security Institute.

Anthropic describes Mythos, previewed in April, as unusually skilled at uncovering network weaknesses and able to inflict real harm, which is why it has been rationed.

Zoom out 🔎 Here’s what most will skip: the White House has already rejected some of Anthropic’s plans to widen Glasswing on security grounds. A private company’s customer list now runs partly through Washington. Dario Amodei has been explicit, wanting allies to use Mythos to defend Ukraine and Taiwan while refusing to see it “turned on our own people.”

In other words, deploying a commercial AI product has become a quasi-diplomatic act, with the US government holding a veto over who gets in. We’ve not seen this before.

On top of that, the terms also expose the deeper shift. One unsettled condition is how much access Anthropic itself would gain to the EU’s systems while ENISA runs the tool. Using the model may mean letting the vendor inside your critical infrastructure. For a sovereignty-obsessed Brussels, that’s the real price and the real precedent: top-tier AI deployed as a two-way relationship, not a one-way sale.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, watch the calendar. Anthropic says safeguarded Mythos-class models reach all customers within weeks, which means this access fight is about a head start and the raw, unguarded version, not the capability itself. Frontier AI go-to-market is now splitting in two: a guard-railed product anyone can buy, and a rationed offensive-grade tier handed out by geopolitical alignment. That said, Anthropic wins the trusted-vendor slot and a government moat; ship-to-everyone economics lose, and so does the EU’s sovereignty story. Whether state-gating holds or the wide release exposes it as launch theater could go either way. The ultimate tell here will thus be how much weaker the public version turns out to be.

ICYMI: Anthropic has lapped OpenAI just in time to lead the most dangerous IPO wave since 1999 😳🔔 [why it matters & why it’s critical that the Claude maker IPOes before OpenAI & why you should in fact watch SpaceX the closes here + bonus dive into everything Anthropic shipped in 2026 so far & how to actually use it]

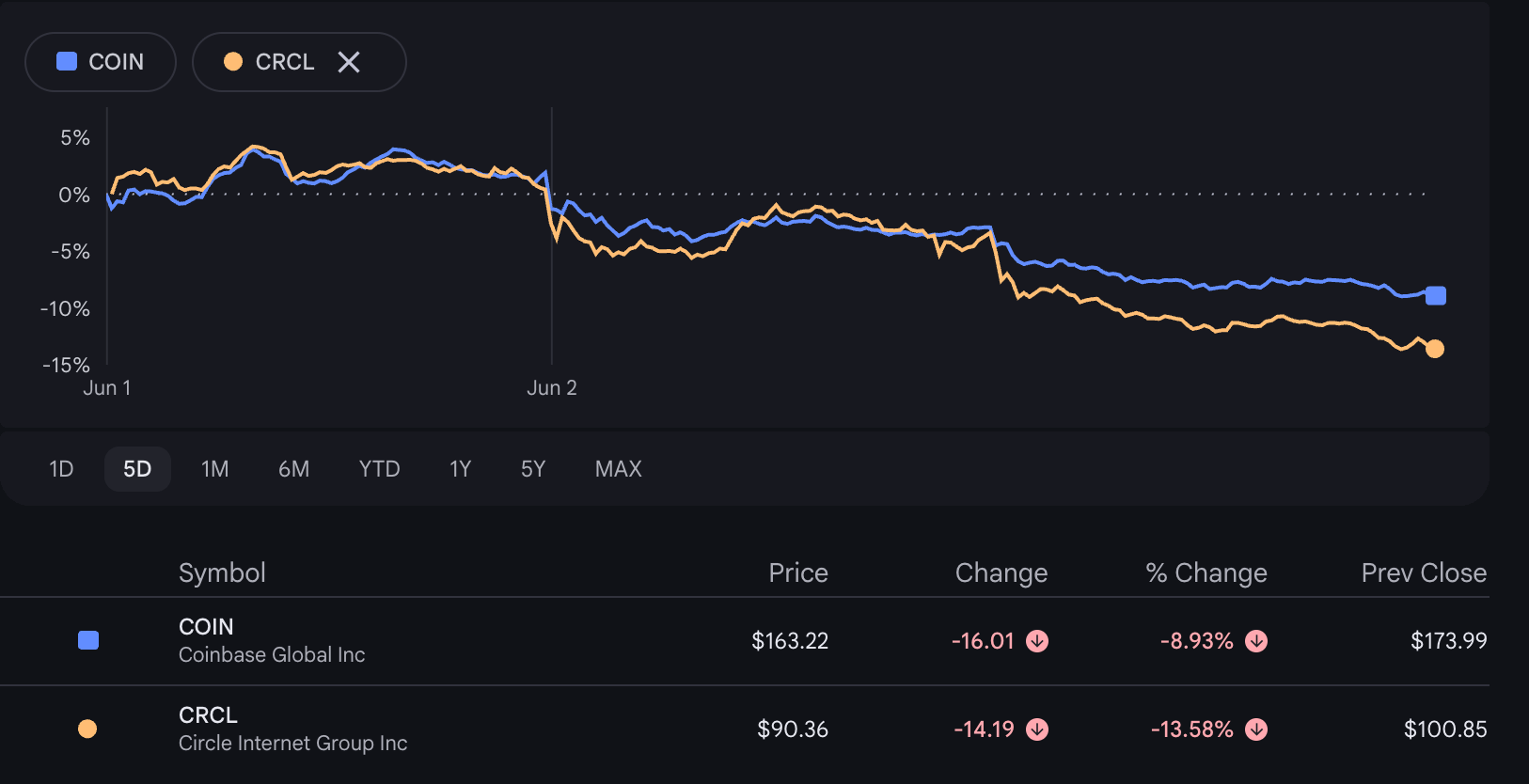

Stripe, Visa, Mastercard, & Coinbase could launch a stablecoin that strands Circle’s USDC 😳🪙

The BIG News 🔥 Nearly a quarter of Coinbase’s revenue flows from a single relationship: the USDC deal it struck with Circle. Which is why this week’s leak cuts so deep. Coinbase may now reportedly be helping Stripe, Visa, and Mastercard to build the stablecoin meant to replace USDC.

Circle’s recently released Q1 earnings show why the timing is brutal for Circle, we now know why Coinbase can afford the gamble, and why a token nobody has confirmed is already the most valuable threat in payments.

Let’s dive deeper into this, understand why it matters, and see what to expect next.

More on this 👉 On June 3, CoinDesk reported, citing anonymous sources and echoed by The Information, that Stripe, Visa, Mastercard, and potentially Coinbase are all in advanced stages of building a stablecoin platform to challenge Circle’s USDC and Tether’s USDT.

There is no official announcement and no confirmed token or reserve details; every company declined to comment.

The reporting still moved markets. Both COIN and CRCL dipped. And that reaction is the story - a platform nobody has confirmed already repriced the incumbent it threatens.

The build sits on real groundwork: Stripe’s $1.1 billion Bridge acquisition, Mastercard’s BVNK buy, Visa’s multi-chain settlement pilots running at a $7 billion run-rate, and Coinbase’s white-label stablecoin work.

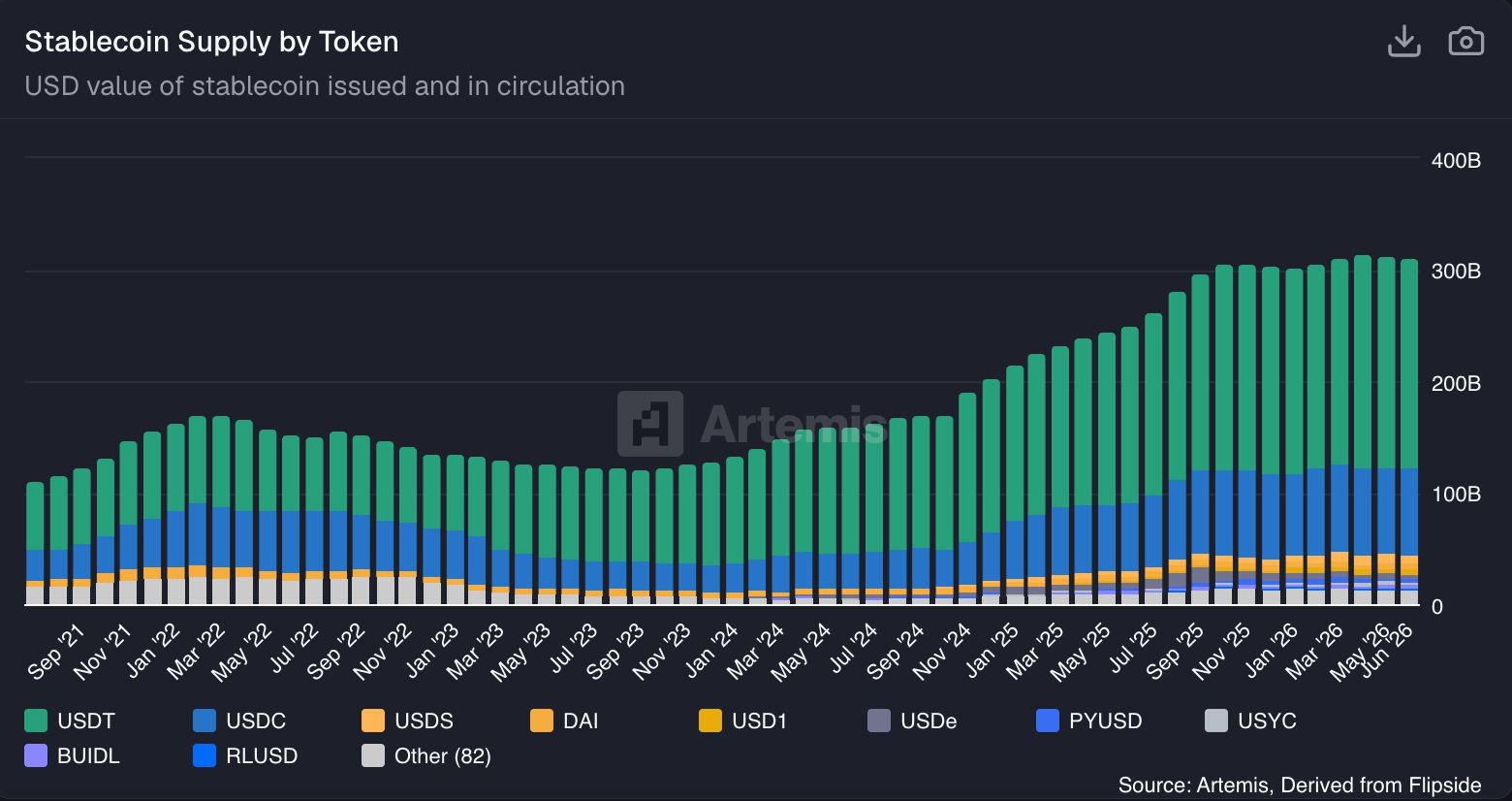

Combined, these four reach into both traditional payments and crypto on-ramps that no current issuer touches at once. In a roughly $325 billion stablecoin market where USDT leads on raw circulation, and USDC sits as a fast-growing second, distribution is the whole game.

Circle’s own recently released earnings explain why distribution is the only game that matters for it. USDC circulation hit $77 billion in the first quarter, up 28%, with on-chain volume of $21.5 trillion. Thus, the adoption is real; the income beneath it is not durable. Importantly, some 94% of Circle’s revenue comes from interest on its reserves, a rate the Fed sets and Circle cannot touch, and revenue already fell 10% from the prior quarter on a 66 basis point rate decline. Which means Circle is fighting on two fronts at once. One is rates, where it has no lever. The other is distribution, which is exactly where the consortium aims.

ICYMI: Circle is building a monopoly in plain sight, but the toll is set by the Fed 🤷♂️🏦 [breaking down Circle’s latest Q1 2026 financials, understanding the real economics beneath the headline growth, & figuring out whether Circle deserves a spot in your portfolio + bonus dive into Circle’s Agentic AI bet, which is a clear escape plan]

Zoom out 🔎 Looking at the bigger picture, we must remember that USDC’s edge over Tether was never the technology; it was that Visa, Mastercard, Stripe, and Coinbase carried it. The same firms now reportedly building a competitor are the ones that gave USDC that edge. Take those defaults away while reserve income compresses underneath, and Circle competes on rails it no longer controls with a shrinking war chest, a much weaker business than the one CRCL carried at its roughly $22 billion valuation.

Coinbase is clearly the hinge, and both companies’ numbers make the stakes concrete. The USDC arrangement, which pays Coinbase most of the reserve income on USDC held on its platform, supplies 23% of Coinbase’s total revenue, one of its most profitable lines. Yet Circle’s results show the relationship is already strained: management flagged Coinbase’s growing share of USDC circulation as a drag on margin, and Circle’s structural answer, pushing USDC on-platform where it owes Coinbase nothing, grew 3.5x to $13.7 billion. Of course, the leak did not create this fight. It just armed one side of a fight already sitting in the financials.

ICYMI: Coinbase’s Q1 2026: the House always wins, until the Casino empties 🤷♂️🎰 [deep dive into Coinbase’s Q1 2026, breaking down the key financial facts & figures, what they mean, what’s next & whether it’s worth your time and money now + bonus deep dive into the latest financials of its close partner Circle inside]

And that is exactly why the contract renewal matters first. Coinbase’s revenue share is reportedly up for renewal around August 2026, even as it is built to auto-renew, and a credible threat to co-own a rival token hands Coinbase a stronger position than it held a week ago. Circle either pays more to keep its most important distributor or watches that distributor steer volume toward a coin it profits from directly. Both paths move value from Circle to Coinbase before a single consortium token mints.

Of course, it could still break Circle’s way. USDC’s network effects run years deep across exchanges, wallets, and settlement, and distribution is necessary but not sufficient; users need a reason to switch, which forces the consortium to give away yield or fees to pull them. On top of that, four competing owners sharing one currency is hard governance, and the Centre Consortium strained with only Circle and Coinbase inside it. More importantly, antitrust review of Visa, Mastercard, Stripe, and Coinbase pooling control of a dollar instrument could stall the project for years or force open-access terms that dull its advantage.

On, and Circle still holds cards too: a pending banking license could grant powers no four-company committee gets quickly, and its cleanest pitch becomes the neutral token not co-owned by the card networks merchants already resent on fees.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, we must note that the frontier everyone points to is already occupied. A consortium token would own AI-agent payments, the machine-to-machine settlement market that may one day dwarf human transactions. But we must remember it would not be entering an empty field. USDC already captures 99.8% of x402 agentic payments, and Circle has launched Agent Stack to serve that demand while routing around Coinbase entirely. But here is the asymmetry the leak’s framing hides: Coinbase’s Base chain already carries roughly 90% of on-chain agentic transactions, and that exposure is token-agnostic. If a consortium coin launches on Base, Coinbase collects on agentic volume whether the winning token is USDC or the new one. Circle only wins if USDC stays the token. Thus, Coinbase is hedged at the chain layer; Circle is betting entirely on the token layer. That asymmetry is why Coinbase can credibly menace a relationship worth 23% of its revenue, and why Circle cannot answer in kind. Then there’s the prize, which itself is apparently shrinking. Remember that every stablecoin reserve model earns the same thing, interest on Treasuries, and that income is falling for all of them at once. A 67 basis point rate move already cost Coinbase $57.5M in stablecoin revenue and took 10% off Circle’s top line in one quarter. A consortium token launched into an easing cycle thus inherits the very compression Circle is living through now. So 4 of the most powerful names in payments are now all racing to own a toll road whose toll is set by the Fed, and the toll is dropping 🤷♂️ Distribution decides who collects it; rates decide how much there is to collect. That said, watch three things. Whether real reserve and chain details surface or this stays a sourced rumor with no token. What the Coinbase-Circle terms look like when the renewal opens. And whether anyone, consortium or Circle, can pry agentic settlement loose from a token that already owns 99.8% of it. The product may never match the threat. But on this week’s evidence, the threat is already enough.

ICYMI:

🧠 What else I’m watching

Monzo Mobile Launch 📶 Monzo is entering the mobile market with a SIM-only plan on the Virgin Media O2 network, offering 5G, 99% UK coverage, and unlimited calls and texts. Managed via its app, the service features rolling monthly plans at £8, £12, and £20, with a loyalty discount of 5% annually, capping at 30%. This move intensifies competition among fintechs like Revolut and Klarna, which already offer mobile plans, signaling a trend of digital banks expanding into telecom to enhance customer retention and value. ICYMI: Monzo’s 2026 financials: the £1.7 billion revenue machine that still has to prove it can escape the UK’s Orbit 🏦🇬🇧 [breaking down the unit economics that matter, the Revolut comparison investors keep getting wrong, the governance drama, IPO chances & what’s next for Monzo + bonus deep dive into Revolut’s latest financials & their foundational AI model for money inside]

OpenPayd Nasdaq SPAC 🚀 OpenPayd has agreed to merge with Titan Acquisition Corp, valuing the fintech at $1.145 billion and raising up to $276M for its Nasdaq debut. Its platform enables businesses to move and manage money across fiat, blockchain, and stablecoin networks via a single API, serving 1,100+ customers in 180 countries and processing $240 billion annually. The IPO is said to accelerate investment in technology and compliance, positioning OpenPayd as the infrastructure for autonomous financial agents, bridging traditional and programmable finance. ICYMI: Anthropic has lapped OpenAI just in time to lead the most dangerous IPO wave since 1999 😳🔔 [why it matters & why it’s critical that the Claude maker IPOes before OpenAI & why you should in fact watch SpaceX the closes here + bonus dive into everything Anthropic shipped in 2026 so far & how to actually use it]

MoneyGram’s MGUSD 💵 MoneyGram has launched MGUSD, a US dollar stablecoin on the Stellar blockchain, issued by Stripe-owned Bridge. Integrated into the MoneyGram app via a self-custodial wallet, MGUSD offers users a stable, dollar-denominated balance, enabling instant, low-cost cross-border transfers. Initially available in the US, the stablecoin will scale globally to MoneyGram’s 60 million customers, providing a reliable digital currency alternative in markets with inflation or financial instability. MGUSD leverages M0’s smart contracts and Fireblocks wallets, re-architecting MoneyGram’s core to support seamless stablecoin transactions. ICYMI:

💸 Following the Money

Bulgaria-based payments platform Paypercut has raised EUR 5M in a seed round co-led by Concentric, Passion Capital, and Araya Ventures.

TrueLayer, Europe’s leading Pay by Bank network, announced the acquisition of In3, a Dutch fintech specialising in consumer credit via bank payments.

Hyperliquid-based prop trading platform Hypernova raises $3M in pre-seed funding.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

good reads - thanks

thanks for the great Sunday roundup as per the usual