The real moat in AI Agents isn’t the model. It’s the insurance policy 🤖🛡️; Stripe just turned HTTP 402 into a cash register for AI Agents 🤖💳; Grab bought Stash for $0.63 on the dollar 🤷♂️📈

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

The First One-Person Unicorn and the Race to Own the AI Agent Layer 🤖🦄 [how a solo founder built the fastest-growing open-source project in history, and what comes next for OpenClaw, OpenAI, & the AI OS race]

What to Build in 2026 🚀 [The startup ideas every top VC is funding right now, the pitch decks that worked, and how to build them]

The Android of Commerce - How Google Is Building the Interface Between AI & Money 🤖💸 [why recently introduced WebMCP is a game-changer, how it stacks perfectly into Google’s Android of Commerce playbook, things worth watching, what’s next for FinTechs/Banks/Payments companies, etc. + bonus deep dives into Google’s UCP, how I built an AI OS to run startup with Claude, and how AI is eating software today]

AI Just Killed the User Interface 🧠🖥️ [Anthropic AI launched an app layer inside Claude, & it changed the role of SaaS entirely]

The Agentic Singularity 🤖🌀 [Deconstructing OpenAI’s operating system strategy and the eclipse of the application era]

Turn Claude From a Chatbot Into a Thinking Partner 🧠 [Most people prompt Claude like it’s Google. Here’s the framework Anthropic actually recommends]

Coinbase in 2025: crypto’s toll booth operator is building a highway, but the traffic is cyclical 📈📉 [deep dive into their latest financials, breaking down the most important facts & figures, understanding what they mean, and whether COIN 0.00%↑ is worth your time and money in 2026 and beyond + bonus dive into their biggest competitor Robinhood inside]

Turn Claude Sonnet 4.6 Into Financial Analyst That Never Sleeps 📊 [Most analysts are leaving 90% of Claude on the table. Here’s the framework that turns the world’s best-value AI into a senior financial analyst]

Top 10 AI Startups to Watch in 2026 🤖🦄 [Strategies, stories, and GTM blueprints from the fastest-growing AI companies that have collectively raised $500M+]

As for today, here are the 3 fascinating FinTech stories that are changing the world of financial technology as we know it. This was yet another solid week in the financial technology space, so make sure to check all the above stories.

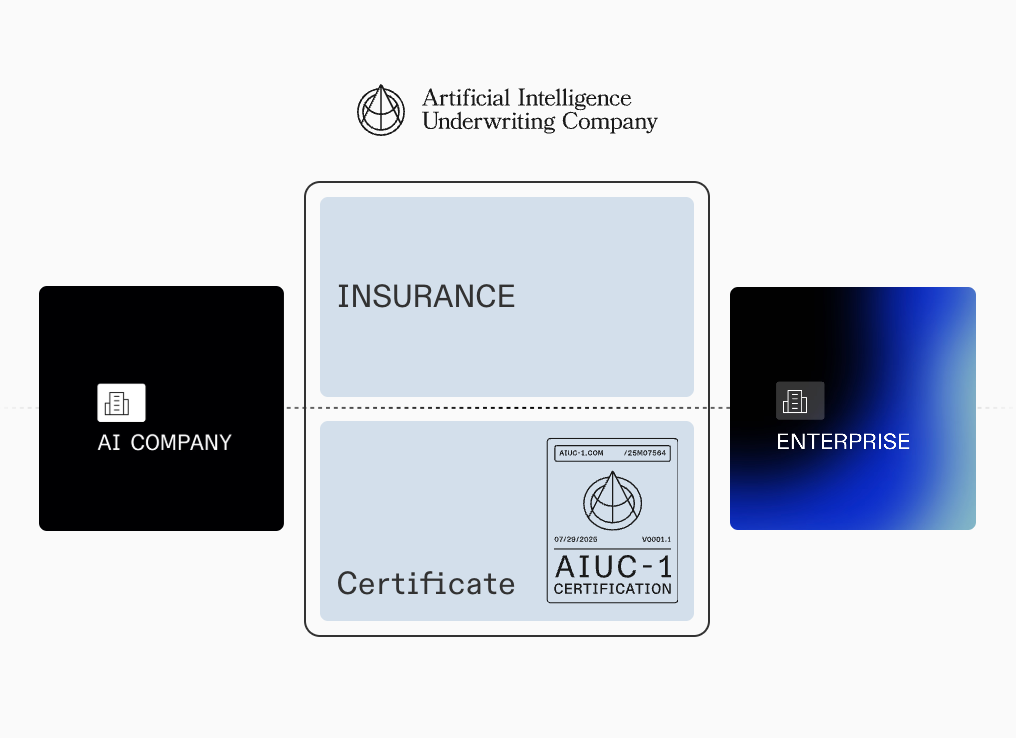

Turns out, the real moat in AI Agents isn’t the model. It’s the insurance policy 🤖🛡️

Following the trends 📈 While the AI industry spent 2025 racing on benchmarks, the insurance industry was quietly pulling the rug out from under enterprise deployments. AIG, Great American, and WR Berkley all moved to exclude AI agent liability from standard policies. E&O carriers started requiring human-in-the-loop review for any AI-generated financial communication, effectively voiding coverage for autonomous agents. A January 2026 Verisk exclusion became available to carriers writing 82% of P&C policies. The message was clear: deploy AI agents at your own risk.

But this week, something interesting happened - ElevenLabs became the first company to close that gap with a live, certification-backed insurance policy covering the actions of its AI voice agents.

Let’s look into this.

More on this 👉 The mechanism matters more than the headline. The Artificial Intelligence Underwriting Company (AIUC) built a three-layer stack:

→ a certification standard (AIUC-1) modeled on SOC-2 but purpose-built for agents,

→ an adversarial audit of 5,000+ simulations across failure modes like hallucinations and prompt injection, and

→ an insurance policy whose pricing is tied directly to audit results. Safer systems get better terms.

The incentive loop is clean.

AIUC itself is worth watching. The $15M seed was led by Nat Friedman. CEO Rune Kvist was the first product hire at Anthropic and sits on the board of the Center for AI Safety. Co-founder Rajiv Dattani ran insurance at McKinsey and was COO of METR, the org that evaluated OpenAI and Anthropic models before deployment.

These are AI safety people who learned insurance, not the reverse.

Zoom out 🔎 The scale context: ElevenLabs powers 3 million deployed voice agents, counts 75% of Fortune 500 as customers, and runs at $330M ARR. Intercom has already certified its Fin agent under the same standard.

Here’s where it gets interesting for finance.

Wolters Kluwer projects 44% of finance teams will use agentic AI in 2026, a 600%+ year-over-year jump. But financial regulators demand auditability, and boards won’t accept unquantified AI risk on the balance sheet.

Certification-backed insurance thus converts the question from “should we deploy?” to “under what terms?” - which is the only framing that gets past a risk committee.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, these are the second-order effect most people will miss: at the core, this creates a hard fork in the AI vendor market. Certified, insurable vendors get access to enterprise procurement pipelines. Everyone else gets frozen out, regardless of technical merit or funding. More importantly, AIUC-1 is on track to become what SOC-2 became for SaaS - a checkbox that quietly determines who can sell to large buyers and who can’t. So if you’re building AI agents for regulated industries and you’re not already thinking about insurability, you’re behind.

ICYMI:

Stripe just turned HTTP 402 into a cash register for AI Agents 🤖💳

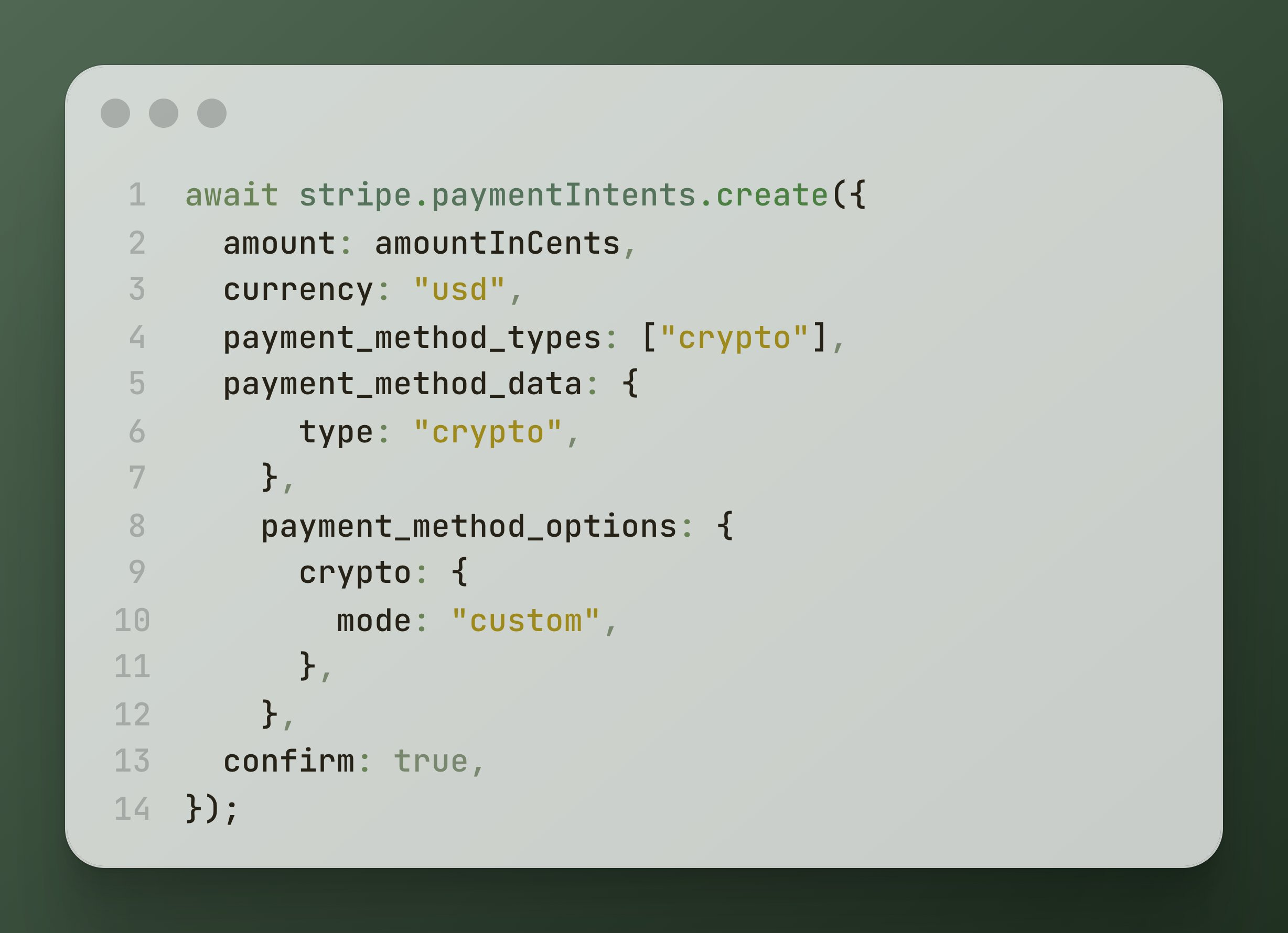

Following the money 💸 $140 billion FinTech giant Stripe quietly dropped the new machine payments preview. And the most revealing thing about it isn’t the crypto. It’s the status code.

HTTP 402 - ”Payment Required” - has been sitting dormant in the web’s architecture since 1997, reserved for a future where the internet would need native payment rails. Stripe, integrating the x402 protocol developed by Coinbase, just activated it.

The system lets AI agents pay for API calls, compute, and data using USDC on Base, settling in seconds for as little as $0.01 per request. No account, no API key, no human in the loop 🤖

An agent hits an endpoint, gets a 402 response with a crypto deposit address, pays from its wallet, and retries. Done ✅

Let’s take a quick look at this to understand why it could be huge and what’s next.

More on this 👉 The mechanics matter here. Stripe generates a unique deposit address per transaction via its PaymentIntents API, absorbs all gas fees, and funnels settled funds into the seller’s existing Stripe balance. Sales tax, refunds, multi-currency payouts - all handled through the same dashboard merchants already use.

Developers add a middleware layer and specify a price in USDC. CoinGecko went live the same day, charging agents a flat penny per data request across 18,000+ tokens and 250 networks, no registration required. Nice!

Zoom out 🔎 The timing tells you something too. Bloomberg reported the same week that Stripe is arranging a tender offer at a $140 billion valuation, up 31% from last year.

Thus, it’s clear that Stripe isn’t experimenting with crypto out of curiosity. It’s staking a claim on the transaction layer between machines before anyone else can standardize it.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, here’s where I’d focus: credit cards charge 2-3% plus a fixed fee, making sub-dollar transactions economically irrational. Stablecoins on L2s don’t have that problem. If agent-driven API consumption scales the way Stripe is betting - Jeff Weinstein, the product lead, frames it as expanding the addressable market from billions of humans to trillions of agents - then whoever owns the payment abstraction layer owns the tollbooth. Stripe’s open-sourcing of tools like purl (a payments-enabled curl) and its existing integrations with LangChain, Vercel, and CrewAI suggest they’re playing for protocol-level lock-in, not just product adoption. Therefore, watch whether competing standards like Lightning Labs’ L402 or Coinbase’s own Agentic Wallets fragment the market or whether Stripe’s developer gravity pulls everything into its orbit. The answer will shape whether machine-to-machine commerce looks more like the open web or more like app stores.

ICYMI:

Grab bought a US FinTech for $0.63 on the dollar, and both sides are celebrating 🤷♂️📈

The news 🗞️ A Southeast Asian ride-hailing company just acquired an American investing app, and the deal tells you more about the state of U.S. fintech than it does about Grab.

Let’s unpack this.

More on this 👉 Grab Holdings signed definitive agreements on February 12 to buy 100% of Stash Financial, the subscription-based micro-investing platform, at a $425 million enterprise value.

Remember that Stash had raised roughly $670 million in venture funding. Do the math now 🤕

Brandon Krieg and Ed Robinson, Stash’s co-CEOs, are staying on, and the app keeps its brand, its model, and its U.S. operations intact.

→ For Stash, this is the best available exit in a market where fintech IPOs remain quite frozen.

→ For Grab, it’s a disciplined entry into the world’s largest financial services market using someone else’s regulatory scaffolding.

Win-win. Kinda.

Zoom out 🔎 The structure of the deal is worth studying here. Grab pays for 50.1% upfront in cash and stock, then acquires the remaining 49.9% over three years at fair market value. In other words, if Stash doesn’t perform, Grab’s total outlay shrinks. If it does, both sides win on a higher valuation. Win-win.

The $60 million EBITDA target by 2028 is the number to watch. Stash is already cash-flow positive, which makes it an anomaly among consumer fintechs and explains why Grab moved now, just days after reporting its first full-year net profit ($200 million on $3.4 billion in revenue). Should I do a deep dive into Grab’s latest financials? Let me know:

The strategic logic is quite straightforward here. Grab’s 50M user base in Southeast Asia generates enormous transaction data from rides, deliveries, and payments. Stash’s AI-driven investing tools need exactly that kind of behavioral signal to personalize recommendations.

Anthony Tan framed this as a fintech knowledge transfer, and he’s right, but the real asset is Stash’s SEC-compliant infrastructure. Building that from scratch would take years. And now Grab has it for pennies on the dollar 😎

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, if this works, expect a wave of Asian super apps acquiring undervalued U.S. fintechs that raised at 2021 prices and can’t exit through public markets (maybe Varo or Public?). Sea Group and Gojek might feel pressure to respond. Meanwhile, Robinhood and Acorns just got a new competitor with a parent company that has no problem subsidizing growth from profitable mobility revenue. The second-order effect most people will miss is this: Grab now has a template for buying regulated financial infrastructure in mature markets. The U.S. might be first. It won’t be last.

ICYMI:

What else I’m watching

Bank of Ireland’s AI Fraud Detection 💳 The Bank of Ireland used AI to assess 1 billion card transactions for fraud in 2025, preventing €9.7 million in losses. The most common fraud types were investment scams, re-direction scams, and romance scams. The bank’s machine learning model includes behavioral analytics and anomaly detection, with agentic AI powering workflow management. The bank has an AI academy and a dedicated fraud and financial crime department. During the holiday season, the fraud prevention team received over 10,000 calls, indicating increased fraudster activity. ICYMI:

Banks Pilot Agentic Payments 💳 DBS and Westpac are partnering with Visa and Mastercard to pilot agentic payment technology. DBS is the first bank in Asia Pacific to pilot Visa Intelligent Commerce, while Mastercard and Westpac have conducted transactions in Australia and New Zealand. Mastercard has also demonstrated the technology in India. The pilots aim to show how AI-powered agents can securely complete transactions on behalf of customers. ICYMI:

Google’s Agentic Shopping Launch 🛍️ Google is rolling out its agentic commerce technology, allowing US shoppers to buy items from Etsy and Wayfair in AI Mode in Search and the Gemini app. The Universal Commerce Protocol (UCP) aims to standardize business interactions with AI agents. Shopify, Target, and Walmart will soon be added. Google envisions UCP extending beyond retail to create seamless commercial experiences. Other companies like Stripe and Visa are also developing similar protocols. ICYMI:

💸 Following the Money

Fractional real estate investment platform Stake has raised $31M in a funding round led by the Gulf’s third biggest bank, Emirates NBD.

Admiral Group to acquire Flock, a digital commercial fleet insurance provider with an innovative telemetry-based proposition. The transaction values the equity in Flock at £80M and is subject to regulatory approval.

Crypto exchange Kraken is furthering its acquisition spree with the purchase of token management platform Magna. This marks the exchange’s 6th acquisition over the past 12 months, including its at-the-time record-breaking $1.5B purchase of the U.S. futures platform NinjaTrader.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Solid read, didn't think about Voice AI that way... does this mean ElevenLabs became harder to beat?