Anthropic is now banking infra 🤖🏦; Revolut GlobalHire isn’t an HR product. It’s a payments product 👥💵; AI Agents started opening bank accounts 🤖🏦

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The Definitive Guide to Perplexity Computer 🖥️ [How Perplexity’s 19-model AI Agent works, what it costs, and whether it’s worth $200/month in 2026]

How to Build an AI Agent from Scratch (With Working Code) 🤖 [The design framework, working code, and hard-won lessons that take you from “I want to build an AI Agent” to a working one - in under 60 minutes]

Skill Graphs: The Architecture That Solves the AI Agent Context Window Problem 🤖 [Your AI agent gets dumber the more you teach it. Skill graphs fix that - here’s the architecture, the cognitive science, and a complete build-from-scratch tutorial]

Inside Revolut’s PRAGMA: The Foundation Model Trained on 40 Billion Banking Events 🧠 [Architecture, performance benchmarks vs. Stripe, Mastercard, and Visa, regulatory risks, and why PRAGMA may be the most consequential AI bet in consumer finance]

OpenAI is building a personal CFO in plain sight 🤖📊 [what their Hiro Finance M&A is all about, why they needed them & how it stacks into their bigger long-term strategy + bonus deep dive into OpenAI’s Agentic Singularity strategy inside]

10 AI Prompt Skills That Actually Change How ChatGPT, Claude, and Gemini Respond 🤖 [Stop telling AI to “write clearly.” Give it real frameworks with measurable constraints and watch the output transform]

The File That Turns Claude Code Into Your Best Engineer 🧠 [A complete guide to CLAUDE.md, rules, skills, subagents, and hooks - everything you need to make Claude Code your 10X Engineer]

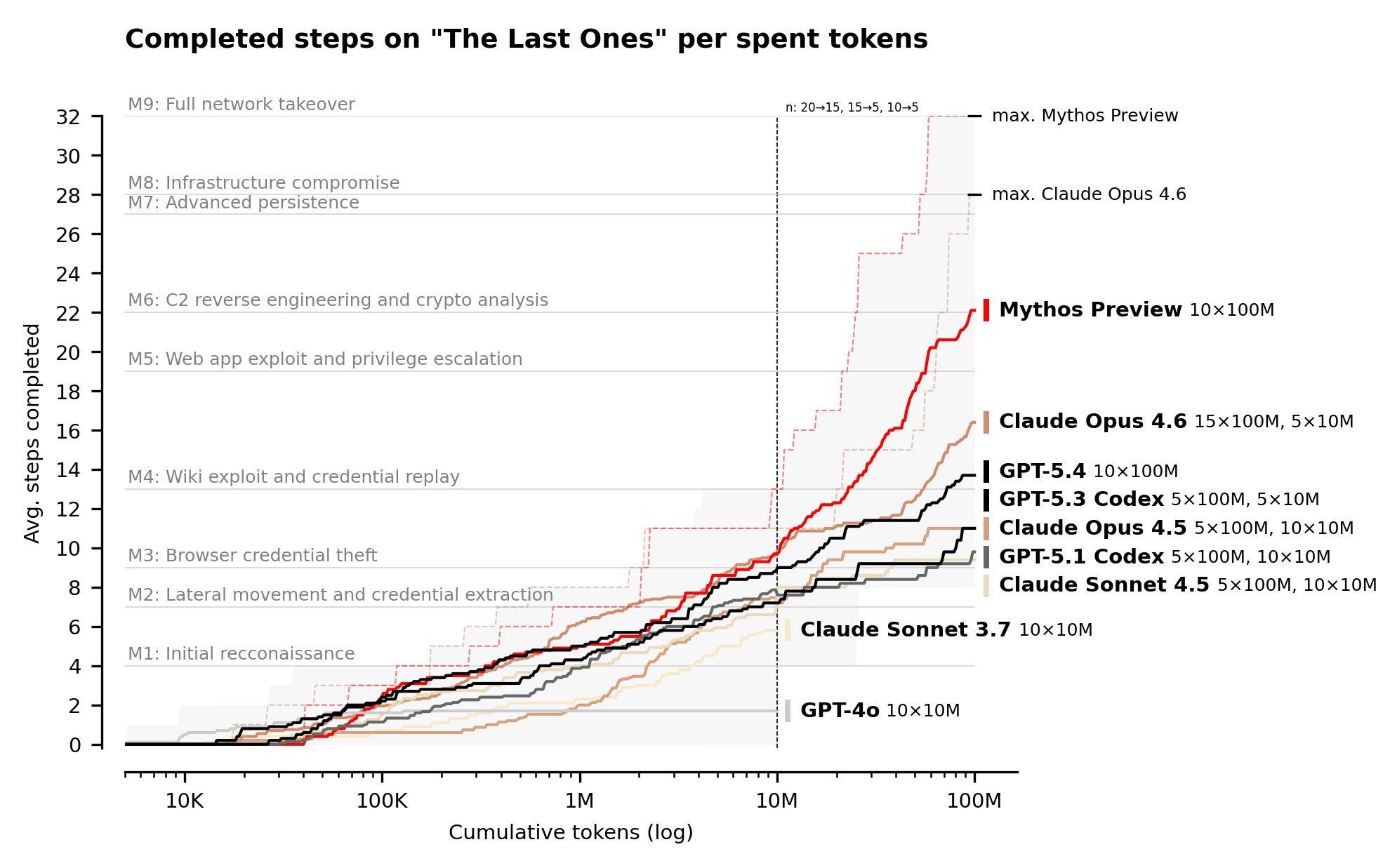

One unreleased AI model just triggered a global financial emergency 😳🚨 [why Claude Mythos prompted the US Treasury, the Fed, the Bank of Canada, and UK financial regulators to hold emergency meetings with their largest banks, where the biggest risks are & what’s next + bonus deep dive into Anthropic’s leaked Claude source code & how I turned Claude Code into my 10X engineer]

American Express skipped the Agent Protocol wars and bought the risk instead 🤖🛡️ [what The Amex Agentic Commerce Experiences (ACE) is all about, why it matters & what to expect next + bonus dives into Shopify’s Agents, AI Agents now opening bank accounts & how to build your first AI agent from scratch inside]

Shopify just made every AI agent a Shopify Agent 🛍️🤖 [what it’s all about & why it’s a brilliant play + bonus deep dive into Shopify’s financials & a full guide of building an AI Agent from scratch]

Turn Claude Cowork Into Your Personal COO 🧠 [Most people are using the most powerful AI agent ever released to answer questions. Here’s the framework that turns Claude Cowork into an operator that runs your work while you sleep]

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

As for today, here are the 3 fascinating FinTech stories that are changing the world of financial technology as we know it. This was yet another intense week in the financial technology space, so make sure to check all the above stories.

Anthropic is now banking infra 🤖🏦

The news 🗞️ Anthropic’s UK head Pip White told Bloomberg this week that Mythos, the company’s cyber-capable frontier model, will reach UK financial institutions within days through an expansion of Project Glasswing.

But the real story isn’t the rollout. It’s that cybersecurity parity for global banks now depends on who Anthropic decides to let in.

Let’s unpack this.

More on this 👉 Mythos has already surfaced thousands of zero-day vulnerabilities across every major operating system and browser in internal testing, some sitting undiscovered for over two decades. The UK’s AI Security Institute confirmed Wednesday the model is “a step up over previous frontier models” at simulating multistep cyber attacks.

Bank of England Governor Andrew Bailey thus called for rapid global regulator evaluation. Treasury Secretary Bessent and Fed Chair Powell had already pulled Wall Street CEOs into emergency meetings after the initial US launch partners (JPMorgan, Microsoft, Apple, AWS, Cisco) got access.

Zoom out 🔎 Anthropic is framing this as safety-first gating. That’s half true. Mythos is powerful enough that unrestricted release would be reckless. But the same restraint creates one tier of institutions with AI-hardened perimeters and another without. Banks inside Glasswing can now run continuous automated pentests against their own COBOL-and-API spaghetti before attackers do. Banks outside it are defending yesterday’s stack against tomorrow’s threats 🤷♂️

The uncomfortable part for anyone holding bank equity: this is not the only frontier lab with this capability, and it will not stay contained. Distillation, leaks, and state-actor equivalents are a question of when. The window where Glasswing partners hold asymmetric defensive advantage is measured in months, not years.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch three things. First and foremost, whether the FCA and PRA formalize AI-assisted vulnerability testing into operational resilience rules, which would convert access into compliance. Second, whether cyber insurance pricing bifurcates along Glasswing lines; underwriters love observable moats. Last but not least, whether tier-two UK banks and building societies get access, or get left absorbing systemic risk on behalf of the majors. Anthropic’s London office scaling from 200 to 800 staff by Q1 2027 suggests they expect demand to outrun their ability to supply it. But the firms that wait to be invited are already behind.

ICYMI: One unreleased AI model just triggered a global financial emergency 😳🚨 [why Claude Mythos prompted the US Treasury, the Fed, the Bank of Canada, and UK financial regulators to hold emergency meetings with their largest banks, where the biggest risks are & what’s next + bonus deep dive into Anthropic’s leaked Claude source code & how I turned Claude Code into my 10X engineer]

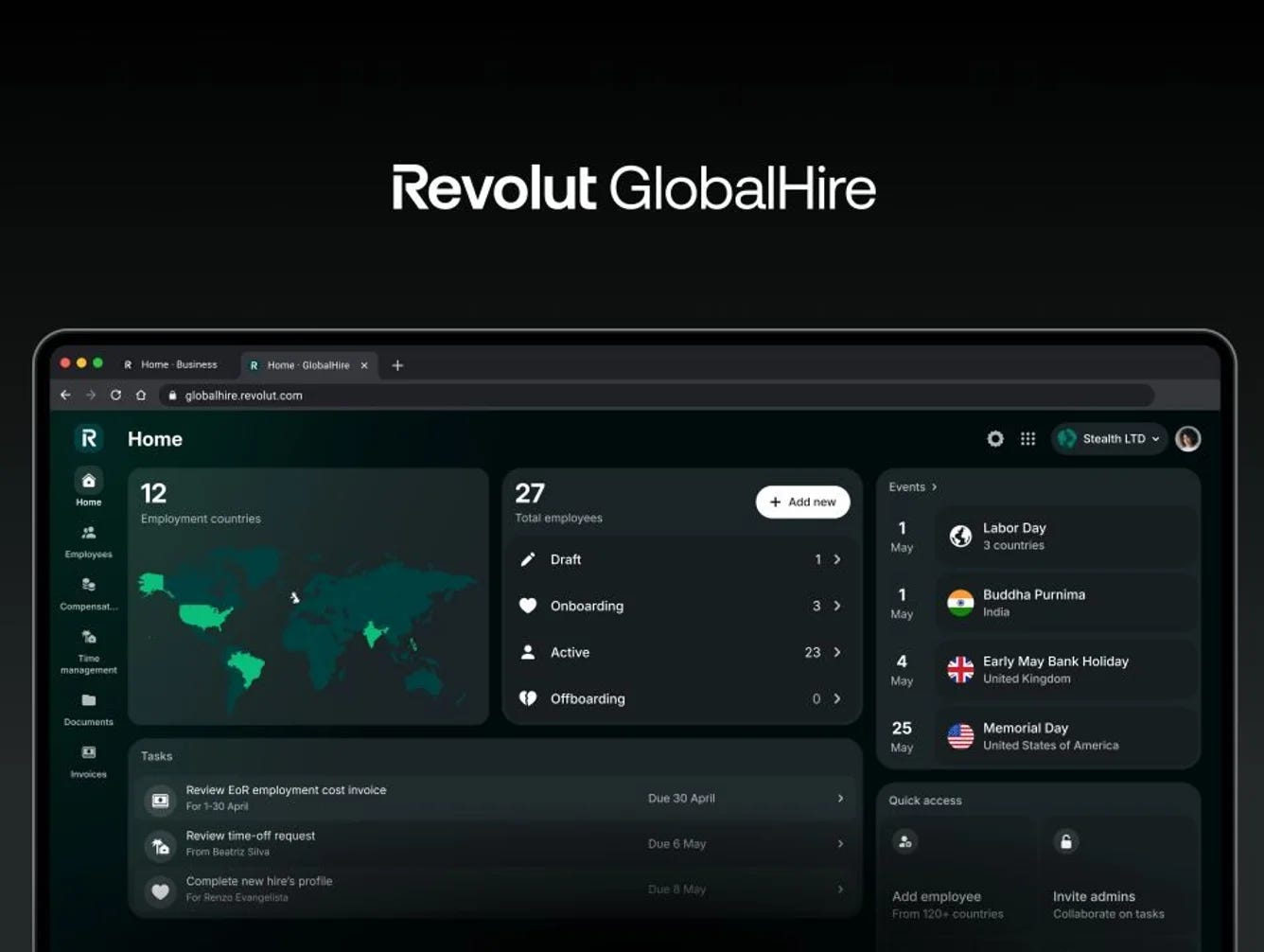

Revolut GlobalHire isn’t an HR product. It’s a payments product 👥💵

The news 🗞️ Every Employer of Record (EOR) company has the same dirty secret: the hardest part of hiring someone in Manila or Tallinn isn’t the legal paperwork. It’s moving money across borders without losing 3–5% to FX markups and third-party payment rails. Revolut just made that the entire point.

Let’s unpack this.

More on this 👉 Yesterday, Revolut launched GlobalHire for its UK Business customers, offering full EOR coverage across 160+ countries at £499 per employee per month, undercutting Deel’s $599 industry standard.

The pricing gap is real but secondary.

The structural move here is that payroll runs natively through the customer’s Revolut Business account at interbank FX rates, zeroing out the currency conversion fees that every other EOR provider either charges or absorbs. Revolut processes $365 billion in annual transaction volume across 39 countries. The hardest operational layer in EOR is literally its core business.

Zoom out 🔎 The timing here is deliberate. GlobalHire sits atop two existing layers: Revolut Business (800K customers, 16% of group revenue) and Revolut People, the HRIS platform Revolut dogfooded internally for its own 10,000+ employees before commercializing it.

Together, they form something none of the pure-play EOR providers can replicate: a single system where a company’s financial infrastructure and people infrastructure share the same data backbone.

And that backbone now includes PRAGMA, Revolut’s foundation model trained on 24 billion banking events from 26 million users. PRAGMA’s product recommendation accuracy improved 40.5% over prior baselines, and its ability to detect recurring transactions means Revolut can identify existing international payroll flows inside Business accounts and target them for conversion before any sales rep picks up the phone. Win-win.

THE TAKEAWAY ✈️

What’s next? 🤔 Obviously, EOR giants like Deel ($1.4B ARR, $17.3B valuation) or Rippling won’t be displaced overnight. It has 35,000+ customers and is building owned entities in 100+ countries. But the mid-tier EOR market faces an existential squeeze. Omnipresent has already sold to Deel for ~$15 million, well below its total funding. Revolut’s entry with deep pockets and a captive distribution base of 800K businesses will only accelerate that consolidation. But the second-order effect worth tracking is far more interesting here. Every GlobalHire payroll event feeds new token types into PRAGMA, enriching the model’s understanding of each business customer, which thus improves credit scoring, cross-sell targeting, and fraud detection across the entire Revolut stack. In other words, the B2B Super App thesis just got its strongest proof point. Therefore, Revolut isn’t entering EOR per se. It’s making employment a financial product, and the companies that built great HR software on top of bad financial plumbing are about to find out what that means for their margins. Yet another reason to be bullish on Revolut.

ICYMI:

Revolut is the most profitable FinTech on Earth, and it hasn’t even started lending yet 🤯📈 [unpacking the fee-income fortress that makes Revolut structurally different from every competitor, the lending optionality coiled inside that balance sheet, the regulatory dominoes now falling in sequence, and whether $75B is expensive or whether the market is about to find out it was way too cheap + more bonus reads on Revolut, how it’s leveraging AI & bonus deep dives into the latest financials of Nubank, SoFi, Robinhood, and Coinbase inside]

AI Agents started opening bank accounts now 🤖🏦

The news 🗞️ For two years, AI agents have been able to write code, browse the web, send emails, and reason through complex problems. The one thing they couldn’t do was spend money. Meow just fixed that.

Let’s unpack this.

More on this 👉 Last week, fintech startup Meow (founded 2021, ~$30M raised from Tiger Global, QED, and Lux, already managing billions in assets) launched a native MCP server at meow.com/mcp that turns its entire banking stack into a promptable tool.

Any MCP-compatible agent - Claude, ChatGPT, Gemini, Cursor - can now open FDIC-insured business checking accounts, issue virtual and physical corporate cards, execute ACH, wire, and crypto transfers across 50+ currencies, pull balances, audit spend, and manage invoicing.

No dashboard. No login. One natural-language prompt.

Zoom out 🔎 The weekend adoption numbers tell the story brilliantly: CEO Brandon Arvanaghi reported agents “signing up in droves” within 72 hours of launch.

Turns out, the demand was already there, just waiting for infrastructure to catch up.

But what makes Meow’s approach credible rather than reckless is the guardrail architecture. Agents operate under scoped permissions with role-based controls, daily limits, and mandatory human approvals (via chat, SMS, or Telegram) for high-value actions. Account numbers stay hidden from the LLM. Every transaction is auditable. Meow isn’t a bank itself; Cross River Bank and Grasshopper Bank provide the FDIC backing, which means the compliance rails were already built before agents ever touched them.

More importantly, the real unlock here isn’t convenience. It’s that finance was the binding constraint on end-to-end agentic workflows. An agent that can research a market, build a product, and write marketing copy, but can’t pay a contractor or invoice a client is still a toy.

Now it isn’t.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch for three things over the next two quarters. First, a fast-follow race: Mercury, Brex, Ramp, and Stripe will all ship MCP endpoints or lose developer mindshare to a company a fraction of their size. Second, the first “agent gone wrong” wire transfer story, which will test whether Meow’s guardrails hold and shape how regulators frame liability for autonomous financial actors. Third, and most interesting: multi-agent payment flows where one agent hires and pays another. That’s where agent-native banking stops being a developer convenience and starts looking like infrastructure for a genuinely new type of economy. The companies building for that world today won’t have to retrofit later. Agentic is the future.

ICYMI:

What else I’m watching

Lloyds Installs AI in Boardroom 🤖 Lloyds Banking Group has introduced an AI “board bot,” developed by Board Intelligence, to assist its board in reviewing confidential materials and preparing for meetings, aiming to reduce human bias in decision-making. The bot provides guidance across cybersecurity, sustainability, financial analysis, and M&A. ICYMI:

Nu Mexico Reaches 15M Customers 🇲🇽 Nu NU -2.60%↓ Mexico has surpassed 15M customers, becoming one of Mexico’s top three financial institutions by user base and achieving 36% year-over-year growth - even faster than its Brazilian operations. Nu’s nationwide success stems from its 24/7 digital, branchless model, resolving over 30,000 needs daily while maintaining human connection. The Flywheel model drives efficiency: scale and technology refine products, reduce costs, and reinvest in user experience. Financial performance reflects this growth, with a 61% rise in the credit portfolio and 21% growth in deposits. ICYMI: Nubank’s Q4 2025: Latin America’s digital banking juggernaut is just getting started (but the market already knows it) 😤📈 [deep dive into their Q4 & full 2025 year financials, breaking down the most important facts and figures, understanding what they mean & what’s next for NU 0.00%↑]

GoCardless Hits Profitability Milestone 📈 GoCardless has achieved its first profitable quarter, driven by a 22% revenue increase and 27% reduction in net losses for FY25. Cost controls, including layoffs and relocating roles to Eastern Europe, contributed to a 55% decrease in losses the prior year. The firm posted its first EBITDA-positive quarter in Q4 FY25 and expects its first profitable year in FY26. Losses before tax narrowed to £24.2M from £31.2M, despite restructuring costs. Acquired by Mollie in December, GoCardless processes over $130B annually for 100,000+ businesses across 30+ countries. ICYMI: Mollie seals GoCardless takeover, creating European payments powerhouse to rival Stripe and Adyen 💳🇪🇺 [what it’s all about & why it makes a ton of sense + bonus dive into Stripe’s recent M&A game, and how they want to own the full AI payments stack]

💸 Following the Money

Polygon Labs is in talks to raise up to $100M for a new stablecoin payments business, according to a report from The Information.

Deutsche Börse has spent $200M to buy a 1.5% fully diluted stake in crypto platform Kraken, deepening an existing strategic partnership between the two firms.

Ralio, a UK startup building a payments platform purpose-built for AI agents, has raised $2.5M in an oversubscribed pre-seed funding round.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Wow, this is awesome! Anthropic is cooking... What's next??