Visa’s AI bet: be the Bouncer, not the Register 🤖💳; Anthropic just found the cheat code for Enterprise AI: BUY your customers 🤫💰; Ramp's CLI for AI Agents 🤖💳

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The Definitive Guide to Perplexity Computer 🖥️ [How Perplexity’s 19-model AI Agent works, what it costs, and whether it’s worth $200/month in 2026.]

Skill Graphs: The Architecture That Solves the AI Agent Context Window Problem 🤖 [Your AI agent gets dumber the more you teach it. Skill graphs fix that - here’s the architecture, the cognitive science, and a complete build-from-scratch tutorial]

10 AI Prompt Skills That Actually Change How ChatGPT, Claude, and Gemini Respond 🤖 [Stop telling AI to “write clearly.” Give it real frameworks with measurable constraints and watch the output transform]

The File That Turns Claude Code Into Your Best Engineer 🧠 [A complete guide to CLAUDE.md, rules, skills, subagents, and hooks - everything you need to make Claude Code your 10X Engineer]

Anthropic stopped selling Intelligence and started selling Infrastructure 🤖💸 [breaking down Claude Managed Agents, why the architecture is really a platform lock-in strategy disguised as a product launch, which startups just lost their reason to exist + how to solve AI Agent context window using Skill Graphs & deep dive into Anthropic’s leaked Claude Source inside]

Revolut just launched AIR, its AI Assistant. PRAGMA is why that matters 🤖📲 [why the actual competitive threat isn’t Starling or Monzo Bank but Apple & Google embedding finance into the OS + bonus deep dive into Revolut’s 2025 financials, how Stripe built AI but for payments, & how to make AI your Sr. Financial Analyst inside]

dLocal is building a monopoly in plain sight, and the market hasn’t fully priced the risk 👀📈 [deep dive into dLocal’s Q4 2025 & full 2025 year financials, unpacking the most important facts & figures to see whether DLO 0.00%↑ is worth your time and money in the years to come + bonus deep dives into the latest financials of other LatAm gems MercadoLibre & Nubank inside]

The Coinbase Bank that doesn’t want to be a bank 🤷♂️🏦 [what Coinbase becoming a national trust bank is truly about & what to expect next + bonus deep dive into Coinbase’s latest financials & more FinTechs becoming banks inside]

Turn Claude Cowork Into Your Personal COO 🧠 [Most people are using the most powerful AI agent ever released to answer questions. Here’s the framework that turns Claude Cowork into an operator that runs your work while you sleep]

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

Productize Yourself 🧠 [Naval Ravikant’s framework for building a one-person company is the best startup strategy of 2026. Here’s the operating system, and 13 AI prompts to run it]

These AI Startups Just Raised $187M, and They Reveal Exactly Where the Market Is Headed 🚀 [These founders secured $187M in Q1 2026. We analyzed their pitch decks, VC backing, and business models to uncover the patterns every AI founder & investor should know]

As for today, here are the 3 incredible FinTech stories that are transforming the world of financial technology as we know it. This was yet another wild week in the financial technology space, so make sure to check all the above stories.

Visa’s AI bet: be the Bouncer, not the Register 🤖💳

Following the trends 🤖 Visa wants to be the reason an AI agent trusts a merchant enough to hand over money.

Let’s take a closer look at this.

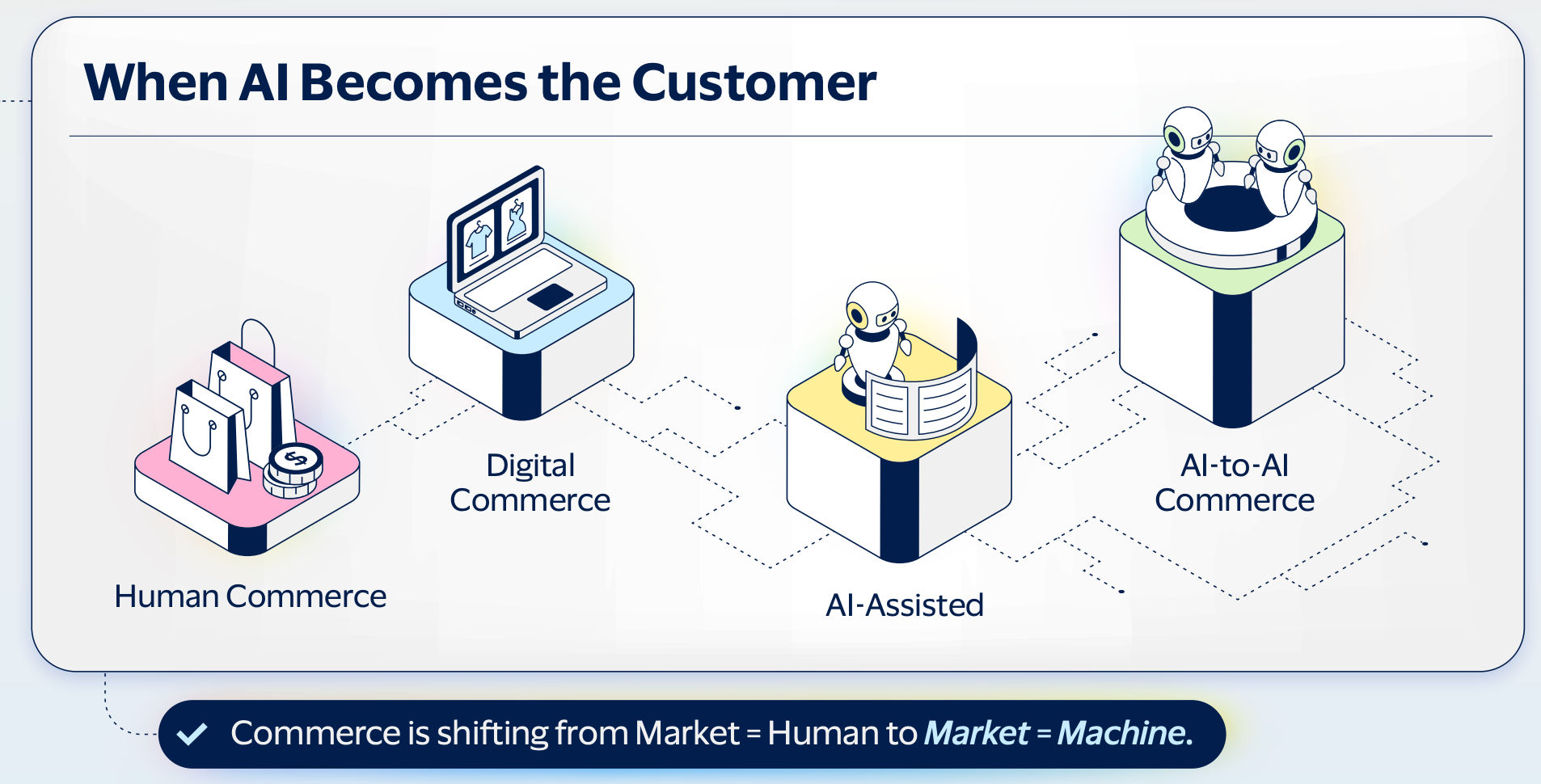

More on this 👉 The payments giant released survey data this week framing what it calls “B2AI” commerce: a world where AI agents don’t just recommend products but compare, negotiate, and buy on behalf of consumers.

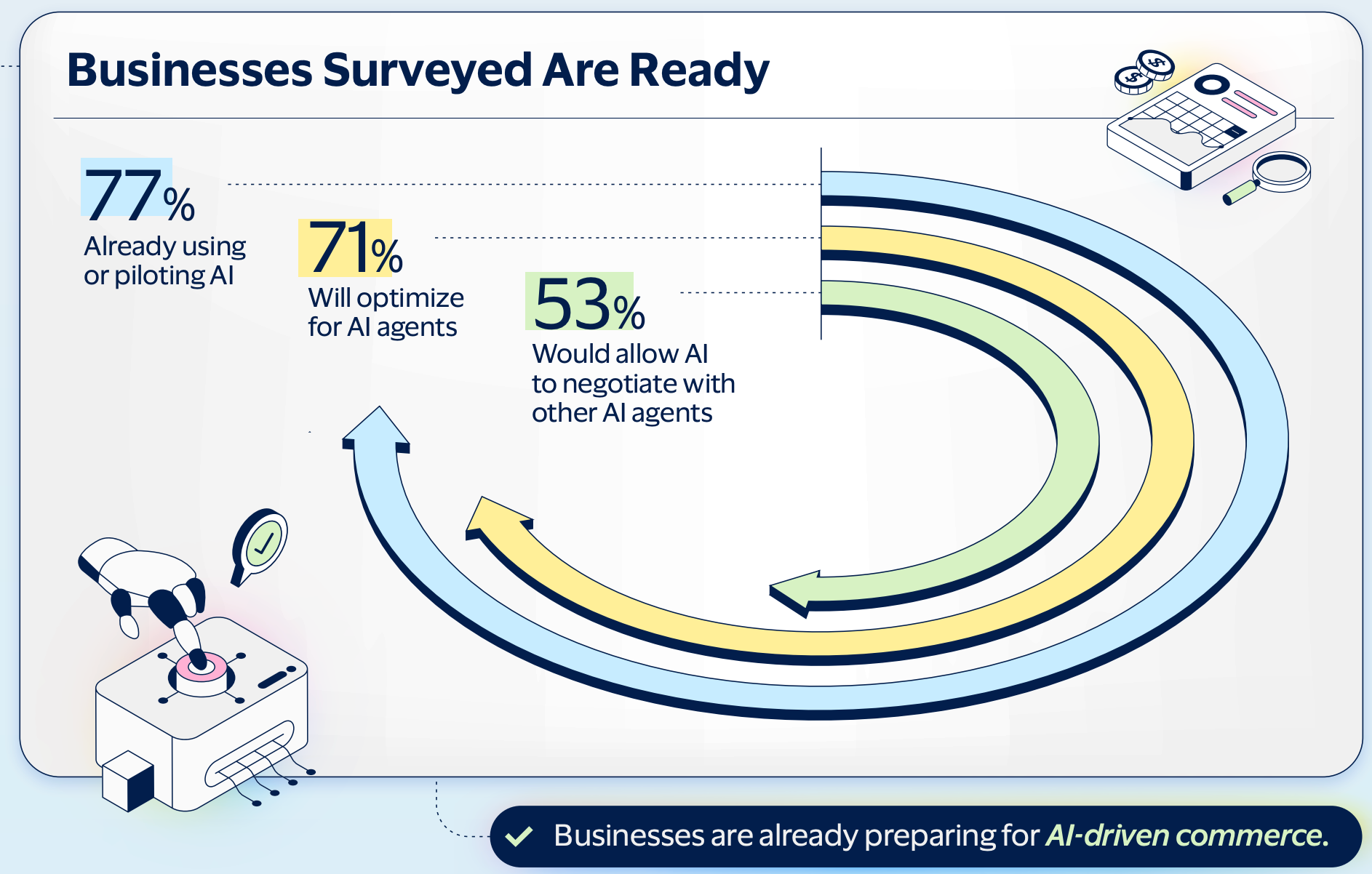

The numbers from roughly 2,000 Americans and 500 businesses tell a split story. On the business side, enthusiasm is running hot: 53% say they’re ready for AI-to-AI negotiation, 77% are already piloting AI in operations, and 88% would feed pricing and inventory data directly to enterprise AI systems. Businesses see agent-readable commerce as inevitable and want in early.

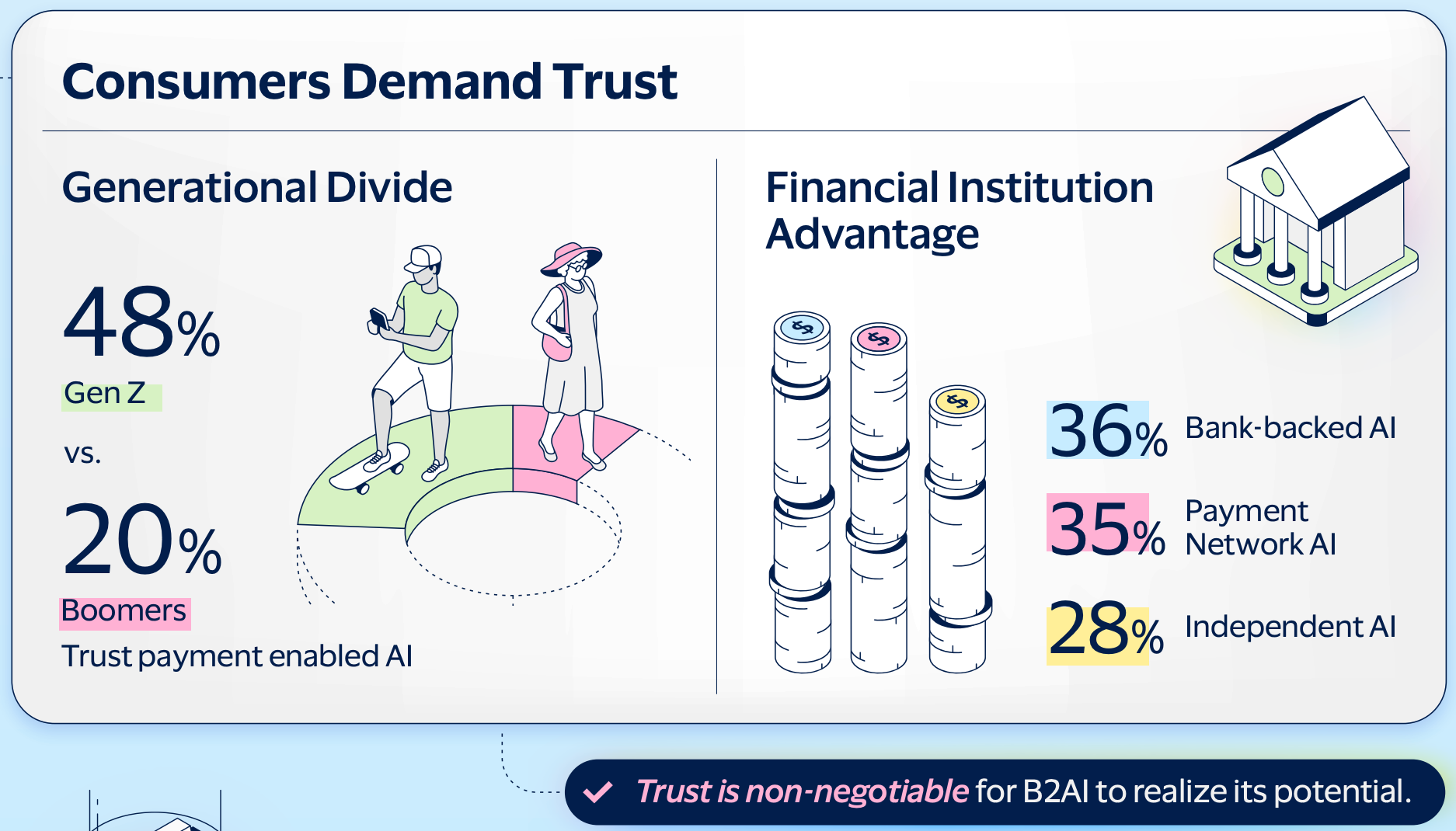

Consumers are a different story. Sixty percent won’t let AI spend a dollar without explicit approval. Only 27% are comfortable with fully autonomous AI purchasing. The trust hierarchy is telling: 36% trust bank-backed AI, 35% trust payment-network-enabled AI, and just 28% trust independent AI agents.

Visa is reading that gap correctly. When nearly 40% of respondents say the ability to override a transaction is what would make them trust AI payments, the value proposition isn’t speed or intelligence. It’s the kill switch.

The generational data confirms the direction of travel. Forty-eight percent of Gen Z trusts payment-enabled AI versus 20% of Boomers.

Hence, the adoption curve isn’t a question of IF. It’s a question of WHO mediates it.

THE TAKEAWAY ✈️

What’s next? 🤔 At the core, here’s what Visa is actually doing with “B2AI” as a concept: staking a claim as the trust and identity layer between AI agents and merchants before anyone else gets there. If agent commerce scales, the traditional card swipe becomes one of many possible rails. But verified identity, fraud detection, and transaction credentialing? Those are harder to replicate. Visa is hence betting that in a world where your AI agent picks the vendor, the brand on the checkout button matters less than the brand guaranteeing the agent isn’t getting scammed. On top of that, the second-order question most people will miss is this: who handles risk decisioning when transactions happen at machine speed, without a human in the loop? Legacy fraud systems were built to evaluate human behavior patterns. An AI agent buying on your behalf doesn’t type, doesn’t hesitate, doesn’t have a behavioral fingerprint. That’s a completely different risk surface. Companies like Oscilar* are already building for this, using agentic AI to make real-time fraud, identity, and compliance decisions at the speed these transactions will demand. That said, watch whether Mastercard MA 0.00%↑, Stripe, or Adyen counter-position in the next two quarters. Because the race to own agentic trust infrastructure just started, and Visa fired the starting gun, mostly to make sure it was already running.

ICYMI:

Visa developed a credit card for AI and shipped it the same day stablecoins got their own payment standard 🤖💳 [what it is & why Visa is doing it, how it stacks with MPP and what to expect next + bonus deep dive into Visa’s latest financials, and how I turned Claude Cowork into my personal COO that does the work while I sleep]

*Disclaimer: I’m part of Oscilar

Anthropic just found the cheat code for Enterprise AI: BUY your customers 🤫💰

Following the money 💸 Turns out, the fastest way to sell enterprise software isn’t to sell it at all - it’s to invest in your customers and let them mandate adoption.

Let’s take a quick look at this and unpack Anthropic’s playbook.

More on this 👉 $380 billion AI giant Anthropic is now putting $200 million into a joint venture targeting a $1 billion raise, with Blackstone, General Atlantic, and Hellman & Friedman among the PE firms in talks to co-invest. The vehicle will function as a consulting and deployment arm, embedding Anthropic engineers directly inside portfolio companies to wire Claude into core workflows: finance, ops, customer service, and coding.

Something the 1% Claude users are doing right now, just on the enterprise scale.

ICYMI:

It’s a massive win-win here. PE firms get an AI efficiency lever to boost margins and exit multiples. Anthropic gets something far more valuable than consulting fees - it gets top-down distribution across thousands of companies without grinding through a single RFP.

Zoom out 🔎 The timing matters here. Anthropic says it’s on pace for over $30 billion in annualized revenue and is talking to banks about an IPO. Locking in predictable enterprise ARR through PE mandates is the cleanest possible pre-IPO narrative.

OpenAI sees the same opportunity: it’s building a rival vehicle (internally called DeployCo) with TPG, Advent, Bain Capital, and Brookfield, reportedly at a larger scale and with sweeter economics, including guaranteed 17.5% minimum returns on preferred equity. Both labs arrived at the same conclusion simultaneously - models alone don’t win; implementation flywheels do.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, we must note that the playbook isn’t new. Palantir ran a version of this for years, embedding forward-deployed engineers to make its software sticky. What’s different is the coercive power of PE ownership. A PE firm doesn’t need to convince portfolio CEOs to try Claude; it can tell them to. That short-circuits the adoption curve in a way no sales team can replicate. Looking ahead, watch two things. First, whether early deployments produce real, measurable ROI or become expensive shelf-ware - PE firms will be ruthless about pulling the plug if margins don’t move. Second, the competitive dynamics: PE firms are already playing Anthropic and OpenAI against each other for better terms, which means the labs may be buying distribution at increasingly unfavorable economics. Thus, the race to own the enterprise AI’s implementation layer is on, and neither lab can afford to lose it. But winning might not be cheap either.

ICYMI:

Ramp just shipped a CLI for AI Agents, and it’s smarter than it sounds 🤖💳

The news 🗞️ One of the most interesting infrastructure decisions in fintech over the last month looks, at first glance, like a step backward.

Let’s unpack Ramp CLI, why it’s interesting, and what’s next.

More on this 👉 FinTech giant Ramp just released a command-line interface - 50+ tools across cards, bills, expenses, travel, approvals, reimbursements - designed not for humans but for AI agents.

Install via curl, authenticate, and your agent gets structured JSON at roughly 105 tokens per call. The demo shows an agent scanning hundreds of transactions, flagging two missing receipts, locating a file on the user’s desktop, base64-encoding it, and uploading it to the correct transaction.

No custom code. No clicks.

Zoom out 🔎 But the real story here isn’t “AI does expenses now.” It’s the engineering tradeoff Ramp made and what it signals.

Anthropic’s Model Context Protocol has become the default standard for connecting agents to tools, but MCP servers are heavy. A single GitHub MCP server dumps ~55k tokens of schema before the agent does anything useful. Stack a few integrations, and you’re burning 70%+ of the context window on overhead.

Ramp’s CLI sidesteps all of it. Benchmarks show CLI approaches running 4-32x cheaper than MCP equivalents, with fewer timeouts. When you’re processing thousands of finance tasks daily across 50k+ customers, that cost gap is existential. As one commenter put it: “cost turns into a product feature once you run this stuff all day.”

Ramp also paired the CLI with Agent Cards - programmable virtual cards with scoped limits, merchant controls, and full audit trails. No card numbers touch the agent. Finance is the perfect proving ground for agentic software because every action is quantifiable and auditable, and errors have dollar signs attached.

ICYMI: Ramp just bought a 15-person Swedish FinTech. It was really buying a continent 🇪🇺💸 [why the acquisition of the 15-person Swedish FinTech is really about “buying” the continent, how both M&As strategically fit into Ramp’s global strategy & what to watch for next + bonus deep dive into the brilliant rivalry of Brex vs. Ramp & how Ramp gave AI agents their cards]

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch for two things. First, whether other vertical SaaS companies follow Ramp’s lead and ship lightweight CLIs alongside their web UIs, treating agents as a first-class user persona rather than an API afterthought. Second, and less obvious: the governance layer. Ramp has audit logs and policy-scoped skills today, but the industry has no standard for “verifiable agent actions” on financial transactions. Whoever builds that trust infrastructure - immutable trails proving an AI did what it claims - owns a chokepoint (hint: Visa is trying to do this right now 👀). Hallucinating a receipt category is annoying. Hallucinating a $200k bill payment is a lawsuit. The companies that solve agent trust for money will solve it for everything else.

ICYMI:

What else I’m watching

Visa Deploys AI Dispute Resolution 🛠️ Visa is launching 6 AI-powered dispute resolution tools to help merchants and financial institutions reduce administrative costs and fraud losses. The suite includes three merchant-focused tools: a resolution network for pre-dispute handling, a recovery manager using GenAI for automated representment with win prediction scoring, and Order Insight to prevent disputes by clarifying transaction details. For issuers and acquirers, tools like Dispute Intelligence, Dispute Doc Analyser for AI-driven document summaries, and a centralized Visa Dispute Case Manager streamline workflows. In 2025, Visa processed a record 106 million disputes globally. ICYMI:

Bolt Slashes Staff for AI Shift 🤖 Bolt, once valued at $11 billion, has laid off a third of its workforce, with CEO Ryan Breslow citing the need to adapt to an AI-centric future and intense competition. The company is also terminating most independent contractors and has struggled to pay vendors like AWS, even offering employees equity in lieu of pay earlier this year. Founded in 2014, Bolt rose to prominence before facing controversies, including a legal battle over a $30M personal loan Breslow took from the company. After a market downturn and multiple rounds of cuts, Breslow returned as CEO last year to launch a “SuperApp” combining crypto and payments, but financial struggles persist. Bolt joins other fintechs like Block and Solaris in using AI as a rationale for job cuts. Yet another reminder that it has never been a better time to productize yourself 😉 ICYMI:

ASIC Warns of AI Scam Surge 🚨 Australia’s financial watchdog, ASIC, is warning that AI is “super-charging” scams, after removing nearly 12,000 phishing and investment scam websites in 2025 - a 90% jump from the previous year. The regulator also dismantled over 1,100 fraudulent investment ads on social media. ASIC Commissioner Alan Kirkland highlights AI’s role in creating polished fake ads, professional videos, and targeted campaigns to trick victims into sharing personal details or money. Australians lost $2.18B to scams in 2025, with investment scams alone costing $837.7M. ICYMI:

💸 Following the Money

Embedded finance provider Cross River has secured a $50M capital raise to fuel investment in AI and crypto.

UK-based international money transfer firm Paysend has secured a $25M follow-on investment from Claret Capital Partners.

Indian loans platform KreditBee has raised $280M at a valuation of $1.5B.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Damn... this is probably the most packed issue this year... 10x thanks!