Plaid’s AI now sees what no single bank can 👀🏦; Santander just open-sourced its AI governance stack. No other major bank has 🤖🏦; Meta wants to clone Polymarket & Kalshi 🤷♂️🏦

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

GLM-5.2: The ChatGPT Moment for Local AI 🤖 [Why the first open-weight model that rivals Claude Opus 4.8 and GPT-5.5 — and runs on a single Mac — changes the game for every founder, builder, and investor]

Turn Claude Into an AI Research Powerhouse With Stanford’s STORM Method 🧠 [Stanford’s proven AI research framework, adapted for Claude — with copy-paste prompts and a ready-made Skill]

Unlock Claude Fable 5 Lite on Claude Opus 4.8 🔓 [The full Fable 5 system prompt and the step-by-step guide to turn Claude Opus 4.8 into a Fable-class AI assistant after Anthropic shut it down]

Loop Engineering: How to Design AI Loops That Build, Ship, and Improve While You Sleep 🔁 [From a three-line bash script to multi-day Claude Fable 5 autonomy — everything founders, builders, and investors need to stop prompting agents and start designing the systems that prompt them]

How to Pre-Mortem Any Decision With AI: The Future Failure Audit Skill for Claude 🔮 [The highest-leverage Claude skill most founders are missing. It assumes your plan has already failed, finds the hidden assumption that kills it, and rewrites it before you commit a single dollar]

Interactive Brokers just let Grok, Claude, and ChatGPT into your portfolio - on purpose 🤖📊 [what IBKR’s new AI capabilities are all about, how it compares to what Robinhood & eToro have launched, and why it might be the most defensible play + bonus deep dive into Coinbase pivot to Financial OS for AI Agents, how Anthropic wants to be Wall Street’s OS, and AI Playbook for Finance inside]

SoFi acquired Composer and bet against the Agentic AI trading rush 🤖💸 [what Composer by SoFi is all about, why it’s interesting, how it stacks against AI initiatives from Coinbase & Robinhood, and what’s next + bonus deep dive into Interactive Brokers’ new AI features & how to build an AI Agent from scratch inside]

Wall Street banks are now America’s AI border guards 🤖🇺🇸 [why JPMorgan & Goldman Sachs pulled Claude models from its employees’ toolkits & what does this indicate about the future AI deployments + bonus deep dives into GLM-5.2, the strongest open AI model today & how to run it on your local computer, and how to Unlock Claude Fable 5 Lite on Opus 4.8 inside]

Coatue’s May 2026 Report: The $12 Trillion AI Bet and Who Ends Up on the Wrong Side 📊 [Coatue’s latest public markets report reveals the most extreme winner/loser split in tech stock history, a $12 trillion AI capex wave, and one brutal framework that predicts exactly who wins]

Anthropic Just Told AI Founders Exactly What to Build in 2026 🦄 [1 million conversations. 9 consumer AI domains. A full founder playbook - plus where Anthropic’s own products will and won’t compete]

As for today, here are the 3 fascinating FinTech stories that are transforming the world of financial technology as we know it. This was yet another insane week in the financial technology space, so make sure to check all the above stories.

Plaid’s AI now sees what no single bank can 👀🏦

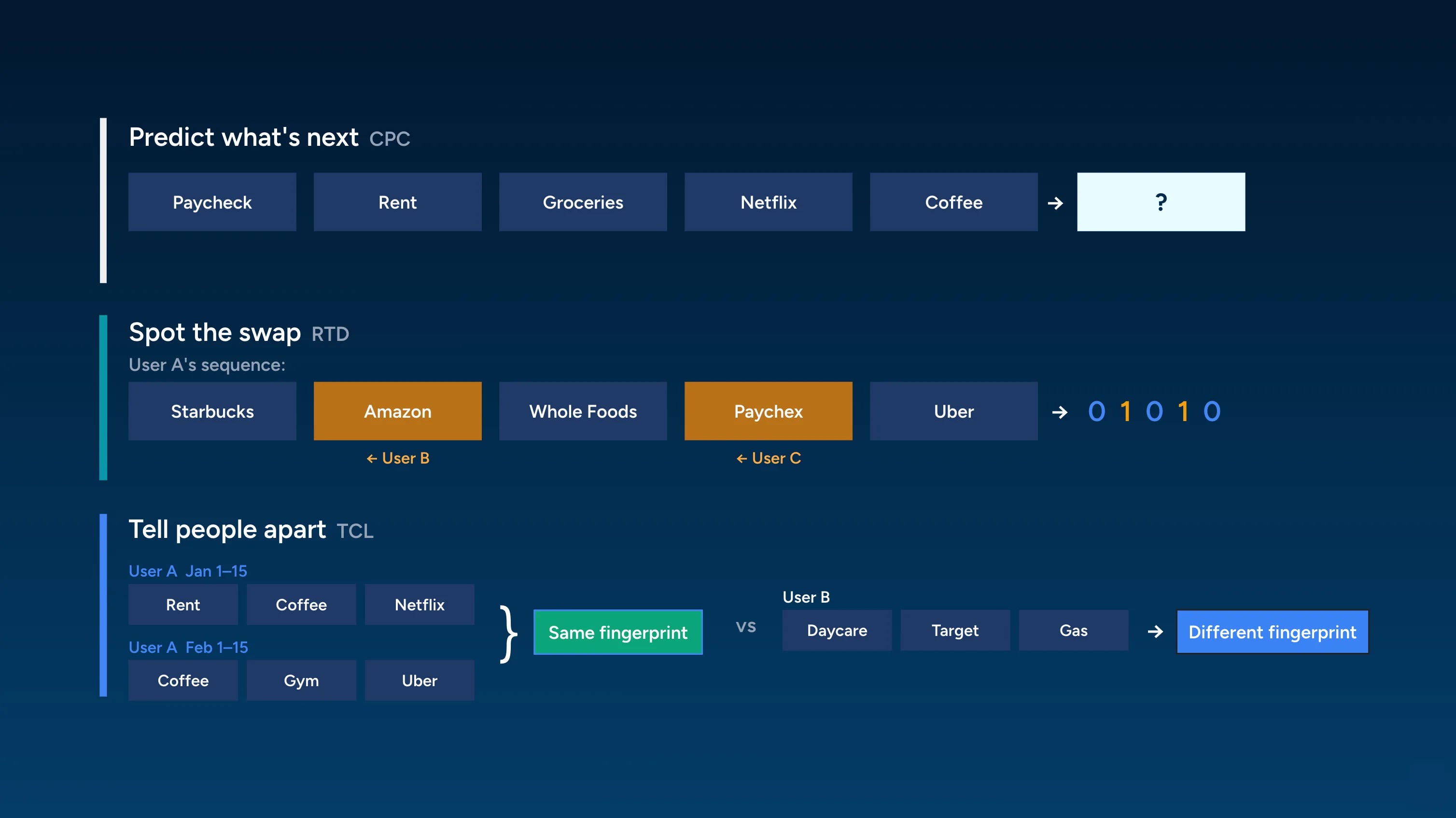

Following the trends 🤖 Every fintech with enough transaction data is now training a foundation model on it. Plaid just showed why the company sitting between the banks and the apps may have the best seat in the house.

Let’s take a closer look at this, understand why it matters, and what’s next.

More on this 👉 Plaid’s new sequential foundation model, building on the transaction model it shipped in April, doesn’t just classify individual payments. It reads the full timeline: order, cadence, recurring patterns, the relationship between a direct deposit on Friday and a flurry of bill payments on Monday.

A $100 transfer means something different after a paycheck than it does sandwiched between overdrafts and payday loans. The model learns that difference through self-supervised pretraining on data spanning thousands of institutions and millions of users.

The early numbers are specific enough to take seriously.

At a fixed 1% action rate on ACH payments, the model catches 26.5% more dollar value in returns - better fraud detection without punishing legitimate transactions.

In credit underwriting, it delivers 13.6% lower default risk while holding approval rates at 70%.

These flow through existing Plaid integrations, meaning every connected fintech gets the upgrade without building anything new. Win-win.

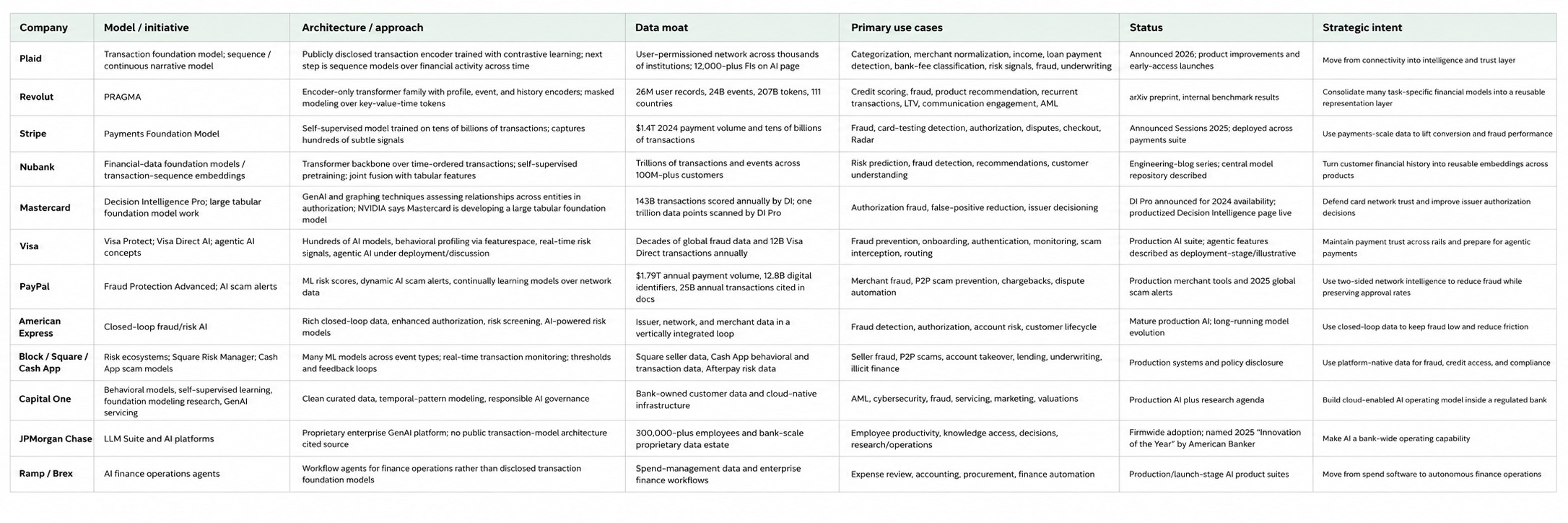

Zoom out 🔎 Of course, Plaid isn’t alone here. Stripe trained its Payments Foundation Model on tens of billions of transactions and claims a 64% cut in card-testing fraud. Revolut’s PRAGMA, trained on up to 40 billion events from ~26 million users, reported a 130% lift in credit-scoring precision. Nubank built nuFormer on 100 billion+ transactions across 100 million+ customers.

The pattern is identical everywhere: self-supervised pretraining on proprietary sequences, general-purpose embeddings, and cheap downstream adaptation.

But what separates Plaid from the pack is breadth without ownership bias. Stripe sees payments. Revolut sees its own users. Plaid sees across the ecosystem at thousands of banks, for users of competing apps. That cross-institutional view is nearly impossible to replicate and exactly what you’d want for a model that generalizes.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, the strategic implication is quite straightforward here. Plaid spent a decade becoming indispensable as plumbing. Now it’s making itself indispensable as intelligence. Fintechs that once used Plaid to pull bank balances will increasingly depend on it to assess creditworthiness and flag risky transfers. Each new event type Plaid folds into the model (balances, account connections, product usage) widens the moat without clients lifting a finger. Looking ahead, the first thing to watch is whether Plaid starts pricing intelligence products separately from connectivity, thus creating a new revenue tier that reflects the value gap between raw data and interpreted data. Second, how regulators respond when a single infrastructure provider’s model influences credit and fraud decisions across thousands of apps at once. Because the power to understand financial behavior at the ecosystem scale is real. But so is the scrutiny that comes with it.

ICYMI: Inside Revolut’s PRAGMA: The Foundation Model Trained on 40 Billion Banking Events 🧠 [Architecture, performance benchmarks vs. Stripe, Mastercard, and Visa, regulatory risks, and why PRAGMA may be the most consequential AI bet in consumer finance]

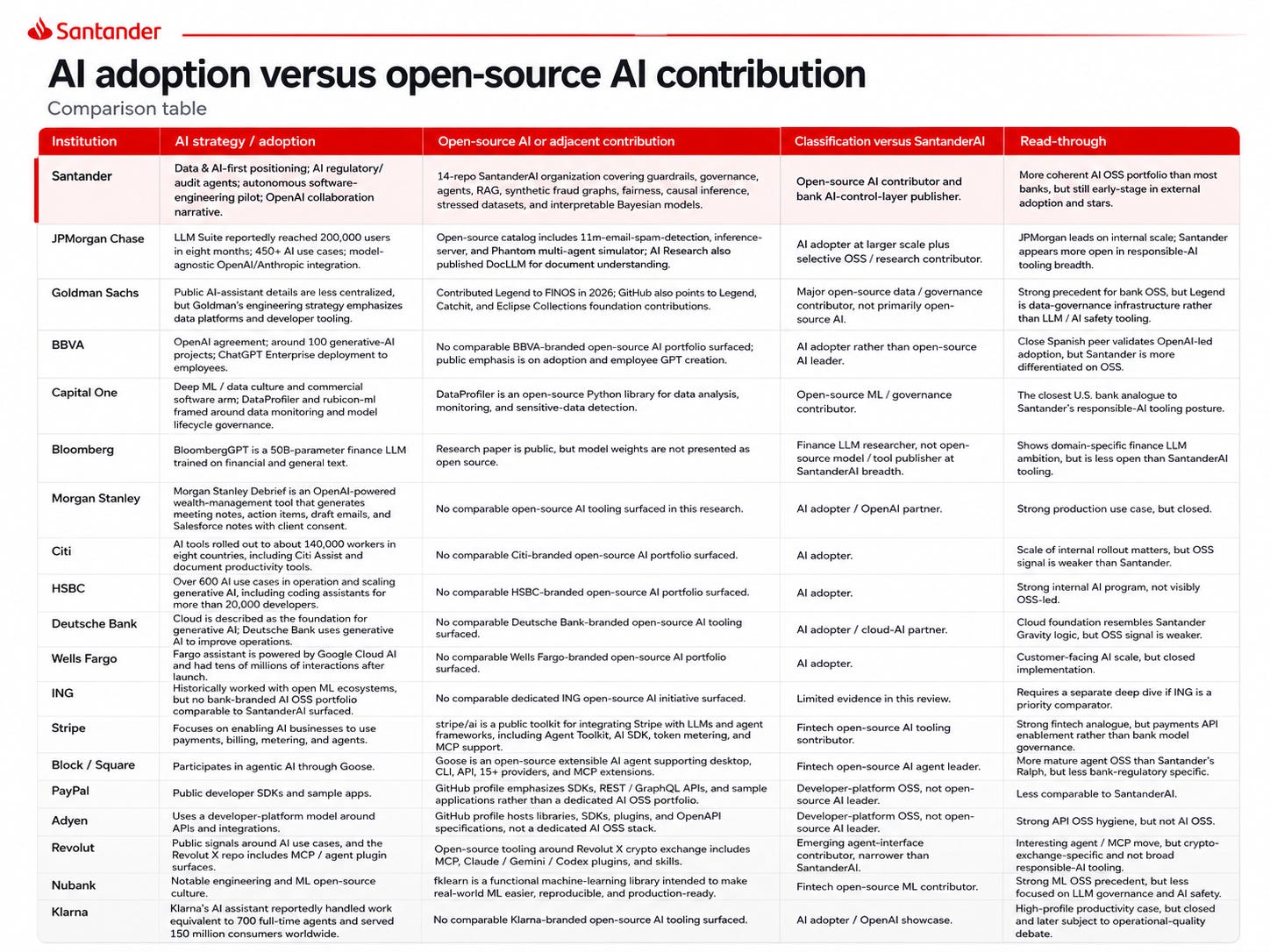

Santander just open-sourced its AI governance stack. No other major bank has 🤖🏦

Following the trends 🤖 Every bank in the world is racing to deploy AI. Santander just gave away the brakes.

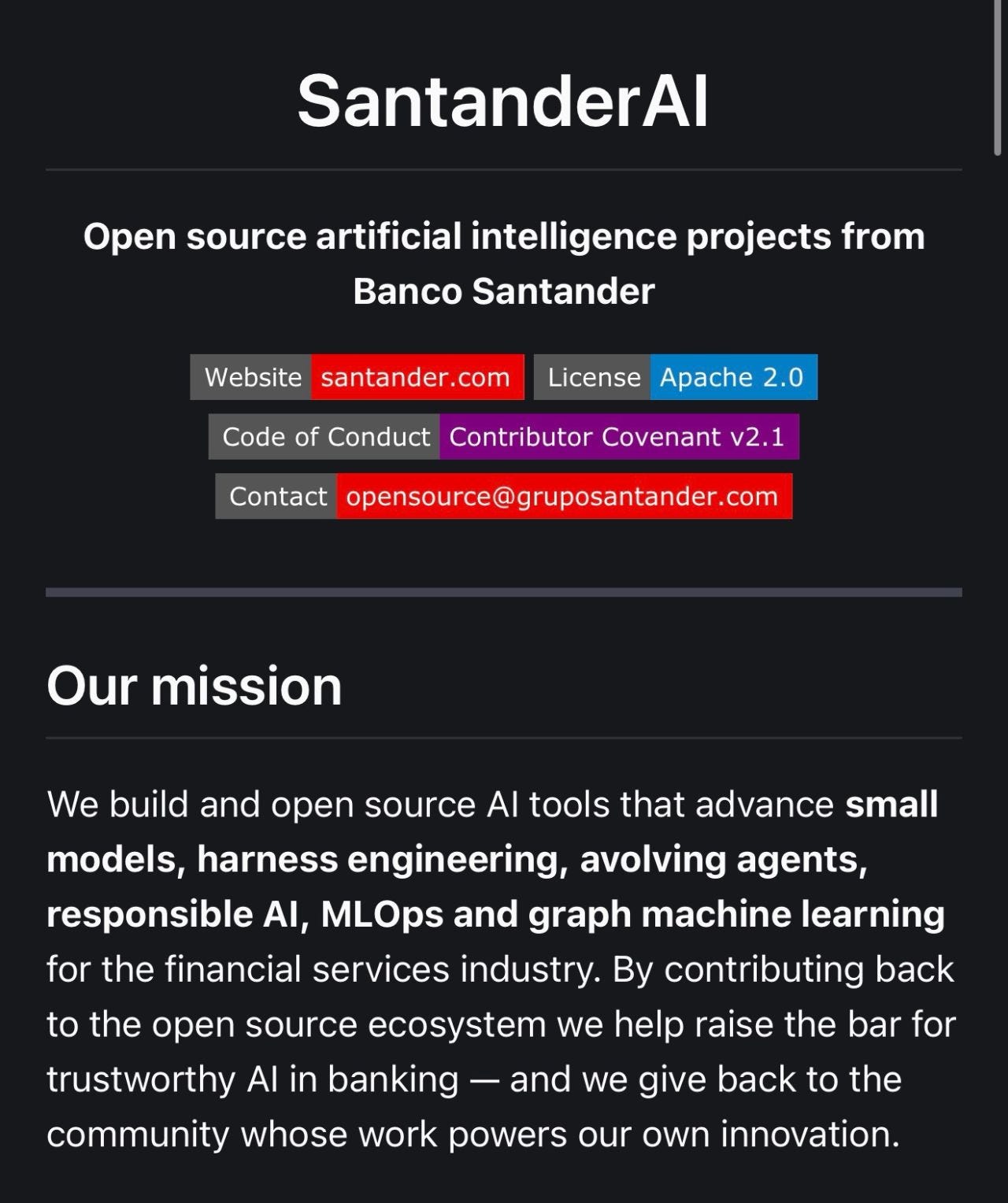

On June 21, Spanish banking giant Banco Santander became the first major global bank to open-source its entire AI governance and safety infrastructure.

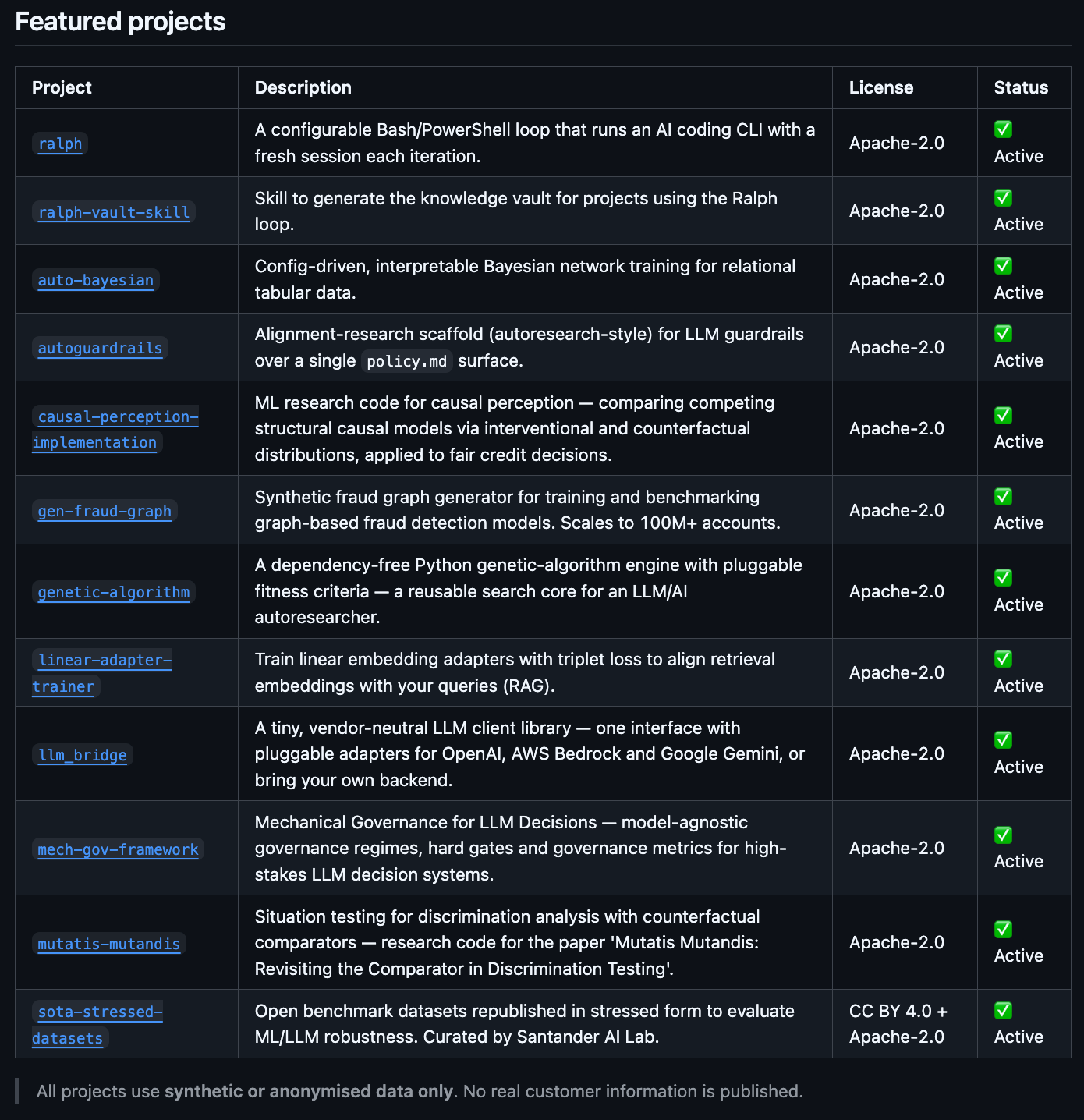

Fourteen repositories on GitHub, all under Apache 2.0.

→ Guardrail optimization, mechanical decision enforcement, fairness testing, and synthetic fraud graph generation.

→ The full code, free for any competitor, fintech, or regulator to fork.

Not JPMorgan. Not Goldman. Not HSBC. No peer has made a comparable release.

Santander came in first and set the precedent.

Let’s take a closer look at this, break down each repo, the strategic calculus behind handing competitors your compliance playbook, and what SantanderAI means for every institution deploying AI under the EU AI Act.

More on this 👉 The repos target the hardest problems in deploying LLMs in banking.

autoguardrails iterates on a mutable policy file to minimize jailbreak attack success rates while enforcing a benign-pass floor so the system can’t win by refusing everything.

mech-gov-framework provides mechanical decision governance with hard gates, argument-quality checks, and tamper-resistant commit-reveal entropy for auditability.

mutatis-mutandis runs counterfactual fairness testing for credit decisions.

gen-fraud-graph generates synthetic financial graphs scaling to 10M accounts and 90M transactions for training graph neural networks without real customer data.

The timing is brilliant here as it tracks to the EU AI Act’s shift from framework to enforcement, with credit scoring sitting in the “high-risk” category. Banks need to prove their AI is auditable and bias-tested, and most are building those capabilities in expensive isolation.

Santander is thus betting that open-sourcing the control layer costs less and buys more: faster hardening through community scrutiny, plus influence over what regulators treat as the baseline.

Zoom out 🔎 Once you zoom out, the strategic calculus is straightforward here.

Models and proprietary data are where banks actually compete. Meanwhile, governance infrastructure is where they all pay the same tax.

Commoditize the tax, and competition shifts to execution speed and domain expertise, where a bank that generated €35 million in AI business value in Q1 alone and targets €1B+ through 2028 has natural advantages. Win-win!

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, there are two things to watch. First and foremost, whether other European banks fork these repos or contribute upstream. If mech-gov-framework starts appearing in regulatory submissions as a reference implementation, Santander will effectively have written the first draft of an industry standard - without anyone voting on it. That would be quite cool! 😎 Second, whether published guardrail logic gives adversaries a better map. At the core, open-source security tends to strengthen defenses faster than it enables offense, but banking hasn’t really tested that assumption with AI governance tooling yet. Zooming out, there’s one big thing at play here - if the control layer is better shared than hoarded, the compliance moat around AI in banking drains. The winners hence won’t be the banks with the best safety frameworks. They’ll be the ones that deploy fastest once safety is table stakes. Hence, position yourself accordingly.

ICYMI: Inside Revolut’s PRAGMA: The Foundation Model Trained on 40 Billion Banking Events 🧠 [Architecture, performance benchmarks vs. Stripe, Mastercard, and Visa, regulatory risks, and why PRAGMA may be the most consequential AI bet in consumer finance]

Meta wants to clone Polymarket & Kalshi, but it can’t clone the regulatory moat 🤷♂️🏦

The BIG News 🔥 Mark Zuckerberg’s playbook has exactly one page, and he just turned to it again.

Let’s take a closer look at what it’s all about this time.

More on this 👉 According to a New York Times exclusive, Zuckerberg has tasked a small team with building “Arena,” a standalone prediction markets app that would sit outside the Facebook and Instagram ecosystem. The initial version would use a points system rather than real money, though the company hasn’t ruled out real-money betting down the road. The app would cover politics, sports, entertainment, and world events.

The pattern is unmistakable.

→ Snapchat proved ephemeral stories worked; Instagram Stories followed.

→ TikTok proved short video worked; Reels followed.

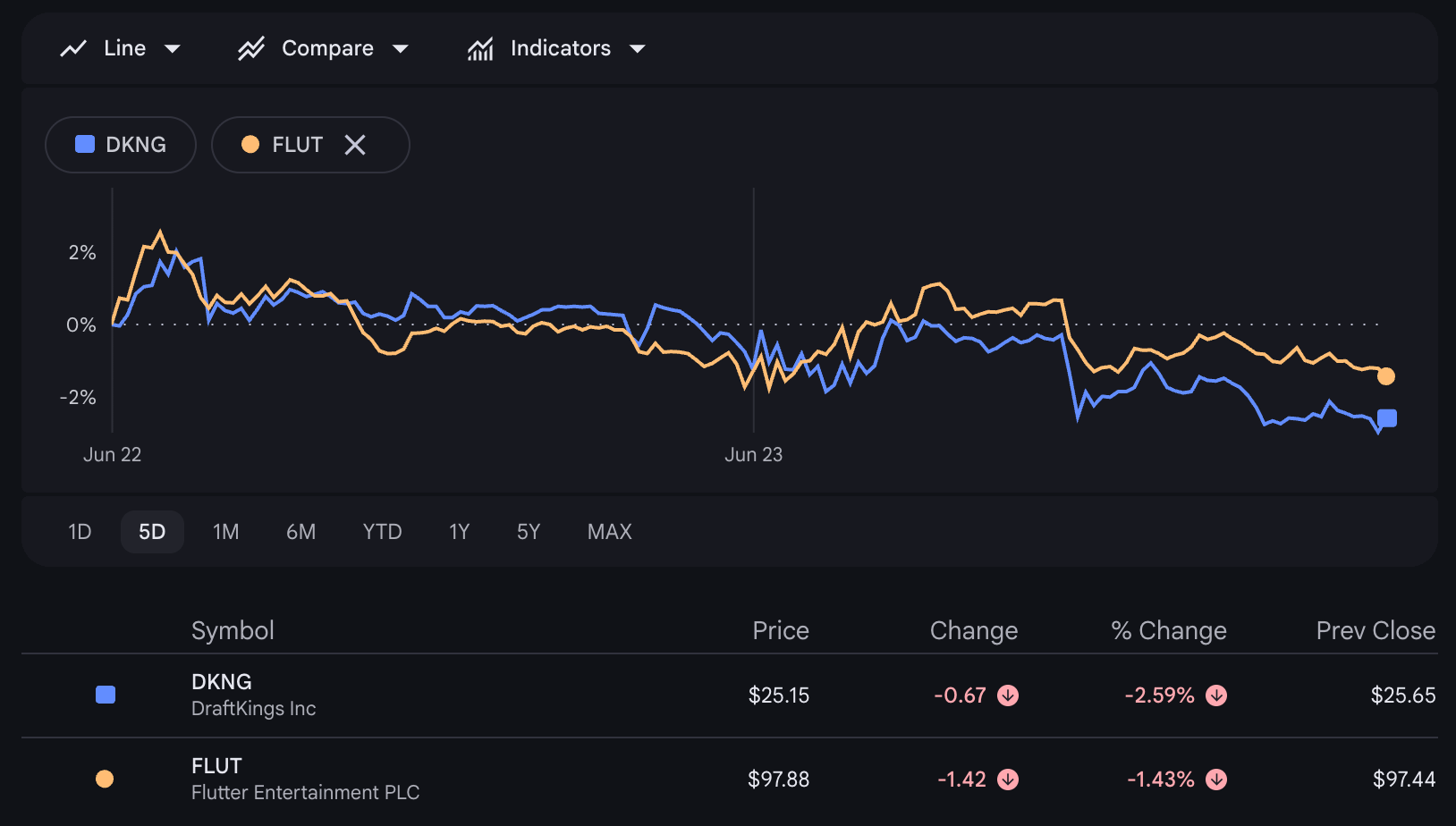

→ Polymarket and Kalshi proved prediction markets worked, handling a combined $50 billion in trades last year and already surpassing $130 billion in 2026. Arena follows.

Zuckerberg basically lets startups burn through capital, thus proving demand, then deploys 3.56 billion daily active users against them. It has worked before, and it has worked very well.

Zoom out 🔎 This sounds good and easy on paper, but we must understand that prediction markets aren’t a UI format you can bolt onto an existing feed.

They’re a regulated financial product sitting in a legal gray zone between information markets, derivatives, and gambling. Remember that Kalshi spent years earning CFTC approval and still faces state-level lawsuits. Meanwhile, Polymarket built its infrastructure on crypto rails and has weathered insider-trading scandals, including federal charges against a U.S. Special Forces member who allegedly netted $400,000 betting on a classified operation in Venezuela.

Thus, the compliance overhead, resolution mechanisms, and market integrity systems these companies built aren’t features Meta can ship in a sprint.

And we can remember that Meta actually already tried this once. In 2020, it launched Forecast, a points-based prediction app focused on COVID outcomes. It shut down in 2022 with minimal traction 🫠

On top of that, the company’s track record with standalone apps is consistently poor. A 2019 initiative called “New Product Experimentation” produced apps for podcasts, travel, music, and matchmaking. Few gained any following.

So what’s different now? Timing and scale of the opportunity. The prediction markets category barely existed as a consumer product three years ago. Today, it’s integrated into sports broadcasts and awards shows. The gap between “interesting experiment” and “real business” has closed, and Meta’s distribution advantage is genuinely unmatched in consumer tech.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, here’s what to watch. For Kalshi and Polymarket, Meta’s entry is a mixed signal. It validates the category at the highest possible level, which helps fundraising narratives and draws more users into prediction markets broadly. But if Arena gains traction, Meta’s ability to cross-promote through Instagram Stories and Facebook groups could commoditize the standalone apps that built this market. DraftKings and Flutter shares already dipped on the news.

But what’s even more interesting is the deeper second-order effect. Big Tech entering prediction markets will accelerate regulatory clarity faster than any lobbying campaign could. Lawmakers who ignored Kalshi’s CFTC battles will pay attention when Meta is involved. That regulatory infrastructure, once built, may actually entrench the incumbents who already have it. So yes, Zuckerberg can copy the product. But he can’t copy the license, and licence is the key here.

ICYMI:

🧠 What else I’m watching

Enterprise AI’s control tower problem 🤖 Most companies are still treating AI like another SaaS rollout: buy the model, plug it into the stack, wait for productivity. I think that misses the harder part by a lot. The model can think (let’s not debate this here!), but the business still has to decide what it’s allowed to touch. Take IT as an example. An agent can spot an incident and suggest a fix. But can it check permissions, route the approval, update the ticket, trigger remediation, and leave an audit trail? That’s why the next enterprise AI race is already moving from smarter models to Sense → Decide → Act → Secure. Without that layer, agents are expensive advice. With it, they become governed execution. And that’s where companies like ServiceNow get really interesting: it already sits inside the workflows where enterprise work gets routed, approved, resolved, and recorded. The more autonomous agents become, the more valuable that control layer gets. Brilliant positioning 👏 You can learn more about how ServiceNow is moving from AI chaos to AI control here.

N26 (Finally) Turns Profitable 📈 German FinTech N26 achieved its first full year of net profitability in 2025, with €1.6 million net income, up from a €42 million loss in 2024. The German digital bank surpassed €500 million in revenue, with customer deposits exceeding €10.5 billion and transaction volume rising 14% to €170.7 billion. The turnaround follows a leadership overhaul and regulatory challenges. Will be very interesting to see if this sustainable growth continues. ICYMI: Starling Bank’s 2026 financials: 2.5x Monzo’s profit on half the revenue, and a £70M SaaS pipeline that changes the IPO math 📈🧠 [unpacking the most important financial facts & figures, how it stacks against Monzo & Revolut, & why Starling’s balance sheet is a fortress + bonus deep dives into the latest financials of Monzo & Revolut inside]

Atom Bank AI Lending ⚡ Atom Bank has implemented Flowable’s AI-ready lending platform, reducing commercial real estate loan approval times by 30%. The system enables AI-augmented underwriting, eliminates administrative tasks, and scales loan volumes without proportional headcount increases. Brokers benefit from seamless login and real-time tracking. The platform future-proofs Atom’s architecture. It will be interesting to see if this will set a new benchmark for lending efficiency. ICYMI:

💸 Following the Money

Deluxe, the company that invented the chequebook, has agreed a $625M cash deal to buy payments processor Celero Commerce.

French sustainable finance startup Green-Got has shattered European crowdfund records by raising €8M ($9M) from 5,286 investors on Crowdcube in just 52 minutes.

Japanese financial group SBI Holdings has co-led a $5.6M pre-Series A funding round for Pints AI, an agentic artificial intelligence startup specialising in the financial services sector.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

good read, thanks Linas!

another awesome read - thanks for sharing this one!