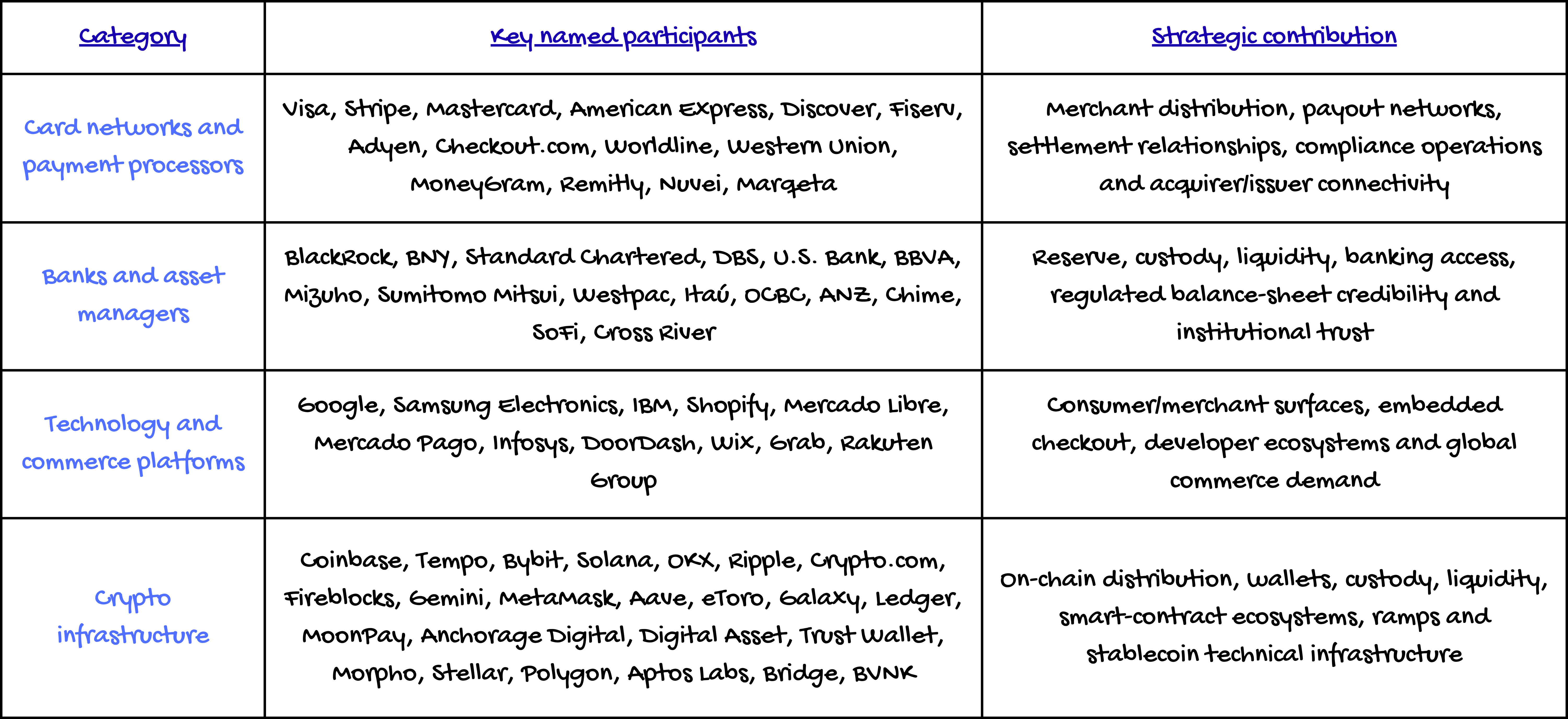

Visa and Stripe back Open USD, a stablecoin that pays its partners 😳🪙; 𝕏 Money just launched with 6% APY and a Visa Card. Stripe, Apple Pay, and your bank have a problem 😳💳

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Claude Fable 5 Is Back. Here’s Exactly What to Build Before the Free Window Closes ⌛ [The highest-leverage use cases, money-making workflows, and copy-paste prompts for founders, builders, investors, and entrepreneurs, while Fable 5 is still included in your plan]

Attention Is the New Startup Infrastructure: The Founder’s Playbook for Winning in the AI Age 📚 [Inside a16z’s “go-direct as a service” model — and the exact moves founders need to turn attention into customers, hires, and capital]

GLM-5.2: The ChatGPT Moment for Local AI 🤖 [Why the first open-weight model that rivals Claude Opus 4.8 and GPT-5.5 — and runs on a single Mac — changes the game for every founder, builder, and investor]

Turn Claude Into an AI Research Powerhouse With Stanford’s STORM Method 🧠 [Stanford’s proven AI research framework, adapted for Claude — with copy-paste prompts and a ready-made Skill]

SoFi’s Q1 2026: the Everything App is becoming an everything earner 📱💸 [deep dive into SoFi’s Q1 2026, breaking the most importat financial facts & figures to see if it’s worth your time and money + bonus deep dives into Robinhood & Coinbase inside]

ChatGPT linked your bank account. Budgeting apps are just the first casualty 🤖📊 [what expanding access to personal finance feature for ChatGPT tells us & which fintechs are now the most vulnerable + bonus dive into OpenAI’s Super App Strategy and The Founders Playbook for Winning Attention in the AI Age inside]

Unlock Claude Fable 5 Lite on Claude Opus 4.8 🔓 [The full Fable 5 system prompt and the step-by-step guide to turn Claude Opus 4.8 into a Fable-class AI assistant after Anthropic shut it down]

Loop Engineering: How to Design AI Loops That Build, Ship, and Improve While You Sleep 🔁 [From a three-line bash script to multi-day Claude Fable 5 autonomy — everything founders, builders, and investors need to stop prompting agents and start designing the systems that prompt them]

How to Pre-Mortem Any Decision With AI: The Future Failure Audit Skill for Claude 🔮 [The highest-leverage Claude skill most founders are missing. It assumes your plan has already failed, finds the hidden assumption that kills it, and rewrites it before you commit a single dollar]

Coatue’s May 2026 Report: The $12 Trillion AI Bet and Who Ends Up on the Wrong Side 📊 [Coatue’s latest public markets report reveals the most extreme winner/loser split in tech stock history, a $12 trillion AI capex wave, and one brutal framework that predicts exactly who wins]

Anthropic Just Told AI Founders Exactly What to Build in 2026 🦄 [1 million conversations. 9 consumer AI domains. A full founder playbook - plus where Anthropic’s own products will and won’t compete]

The Claude Code Creator Just Mapped Out How AI Will Rewrite the Future of Work 🤖 [Anthropic’s Boris Cherny says job titles are “melting” into five new roles. Here’s the data-backed playbook for individuals, managers, and investors to stay ahead in the AI era]

As for today, here are the 2 incredible FinTech stories that are changing the world of financial technology as we know it. This was yet another wild week in the financial technology space, so make sure to check all the above stories.

Before we dive in, a quick word from our sponsor.

Cloud created cloud security.

Mobile created mobile identity.

AI agents are creating non-human identity risk.

Enterprises are now deploying agents that access systems, trigger workflows, and act on behalf of employees.

The problem: You can’t govern what you can’t see.

When an AI agent acts on behalf of an employee, accesses sensitive data, or executes business processes, traditional assumptions about identity and accountability begin to break down. A compromised prompt, excessive permissions, or a poorly governed agent can introduce risks that security teams struggle to detect and contain.

For leadership teams, this is more than a technical challenge, it’s a governance challenge. As AI moves from experimentation to enterprise-scale deployment, identity must become foundational infrastructure.

Okta’s 5-Minute Strategic AI Readiness Assessment helps benchmark where your identity infrastructure stands before autonomous bots become boardroom risk.

Take the assessment here.

Visa and Stripe back Open USD, a stablecoin that pays its partners 😳🪙

The BIG News 🔥 Yesterday, 140 companies that collectively touch most of the world’s payment volume decided they’d rather own the stablecoin than rent it.

Open USD, backed by Visa, Mastercard, Stripe, BlackRock, BNY Mellon, Coinbase, Shopify, Rakuten, and DoorDash, among many others, is a new dollar-pegged stablecoin built around one inversion: the partners who drive adoption capture nearly all the reserve yield, not the issuer.

Zero mint and redemption fees. No volume caps.

No wonder Circle’s stock dropped nearly 14% within hours…

So let’s take a closer look at this and break down the real economics behind Open USD, what each type of partner stands to gain, why JPMorgan and the largest U.S. banks are assembling a rival stablecoin bloc, and the three signals that will tell you whether Open USD reshapes payments or fractures under the weight of its own coalition.

More on this 👉 The coin’s structure is standard: 1:1 dollar backing, reserves in Treasuries and cash, multi-chain issuance across Solana, Stellar, Base, and Polygon. Open Standard, the independent entity behind it, will be run on an interim basis by Zach Abrams, who built Bridge before Stripe acquired it. Governance sits with a board of partner representatives rather than a single controlling company.

The timing tracks to the GENIUS Act, signed in 2025, which gave the U.S. its first federal framework for payment stablecoins and made a compliant multi-stakeholder model like this viable in a way it wasn’t two years ago.

The economics are what truly matter here. Remember that Tether pulled in over $13 billion in profit recently, almost entirely from reserve interest. Circle runs the same model. Open USD flips that arrangement by distributing reserve earnings to partners, minus a small operational fee. Open Standard calls it “earn by default.”

ICYMI: Circle is building a monopoly in plain sight, but the toll is set by the Fed 🤷♂️🏦 [breaking down Circle’s latest Q1 2026 financials, understanding the real economics beneath the headline growth, & figuring out whether Circle deserves a spot in your portfolio + bonus dive into Circle’s Agentic AI bet, which is a clear escape plan]

Zoom out 🔎 The partner logic is clear & straightforward across categories.

→ Visa and Mastercard ride stablecoin rails without ceding economics to an issuer.

→ Stripe, which owns Bridge, gets default stablecoin infrastructure for its merchant base.

→ Banks like BNY pick up custody and reserve roles.

→ Coinbase gets native activity on Base and a hedge against USDC dependence, though it’s explicitly not abandoning Circle’s token.

→ Shopify and DoorDash get cheaper, faster payouts to merchants and contractors worldwide.

The absent names matter too. Maybe even more. JPMorgan, Bank of America, and the EWS/TCH consortium are building a competing stablecoin aimed at G7 payments. Tether, Circle, and PayPal sit outside entirely.

Thus, two rival blocs are now forming in real time.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, the real question now is not whether Open USD can compete with USDC or USDT on technical things. It’s whether 140 partners can govern anything at speed. Klarna, Fiserv, and several other consortium members are simultaneously developing proprietary stablecoins themselves, which thus creates obvious centrifugal pressure. That said, watch for three signals: how fast supply scales after the planned launch later this year, whether Stripe makes OUSD the default for its millions of businesses, and how Circle reprices in response. If Stripe embeds OUSD into checkout the way it once embedded card processing, distribution may decide this fight before governance friction can slow it down. Looking at the bigger picture, we must also note that when Visa and BlackRock restructure who captures stablecoin yield, the debate over whether stablecoins matter is pretty much finished. Every payments company now has to pick which side of the economics it wants.

ICYMI:

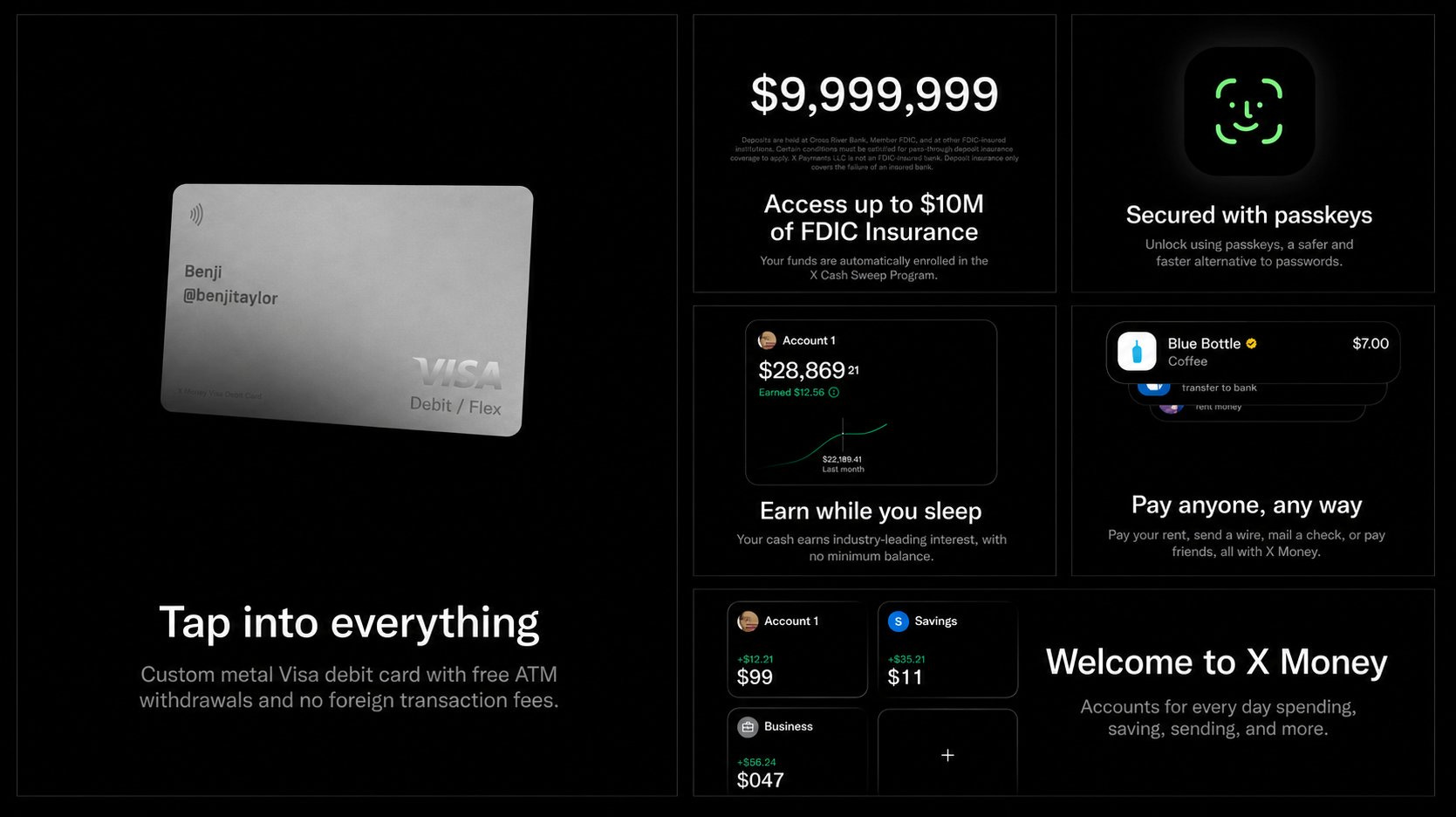

𝕏 Money just launched with 6% APY and a Visa Card. Stripe, Apple Pay, and your bank have a problem 😳💳

The BIG News 🔥 Elon Musk just turned 600 million timelines into bank branches, and the economics make more sense than they look at first glance.

𝕏 Money went live late last week with a 6% APY on cash balances, a metal Visa debit card, instant peer-to-peer transfers, and FDIC insurance up to $10 million.

The yield alone beats every high-yield savings account in the U.S. But the yield is the distraction, not the strategy.

What happens when a platform with 600 million users and near-zero customer acquisition costs decides it doesn’t need to profit from your deposits the way JPMorgan or Goldman does?

Stripe can’t match those economics. Neither can any neobank on the market.

Let’s take a closer look at this, break down the economics behind the 6%, and what 𝕏 Money’s launch means for Visa, Stripe, Apple Pay, and every bank in America.

More on this 👉 𝕏 rolled out 𝕏 Money in late June 2026 to U.S. Premium+ subscribers: a full embedded banking stack built on Cross River Bank’s BaaS infrastructure with Visa on the rails. And the feature set is aggressive.

→ A 6% APY on cash balances.

→ A metal Visa debit card laser-engraved with your 𝕏 handle, not your legal name.

→ 3% cashback.

→ Instant P2P transfers via Visa Direct.

→ Bill pay, early direct deposit, and FDIC coverage up to $10 million through an automated sweep program across partner banks.

The 6% is the headline grabber, and it’s doing exactly what it’s designed to do.

With the Fed funds rate around 4.25–4.5% and top HYSAs maxing out near 5%, 𝕏 is clearly subsidizing the spread. But here’s what most people miss: 𝕏 doesn’t need deposit economics to work. Traditional banks earn on the gap between what they pay depositors and what they charge borrowers. 𝕏 earns when you open the app instead of Chase.

In other words, every dollar parked in 𝕏 Money keeps you scrolling, and every scroll is ad inventory. Maybe it also nudges you toward that $40/month Premium+ subscription. So the deposit isn’t the product. The attention is.

Zoom out 🔎 The customer acquisition math is absurd in 𝕏’s favor. A standalone neobank spends $30–80 to land a checking customer. 𝕏’s cost is approximately zero. Those 600 million users are already there, already habituated, already opening the app dozens of times daily.

Cross River handles compliance, custody, and regulatory overhead. 𝕏 provides distribution. The BaaS playbook is well-worn (Affirm and others have run it through Cross River), but nobody has tried it at this scale inside an existing engagement loop.

The creator economy angle matters too. Routing payouts through 𝕏 Money turns the platform into financial infrastructure for the people who generate its content (thus, a potential risk for Stripe, Airwallex, Payooner, among other FinTechs). Faster payouts and a debit card branded with your online identity make for a pointed retention play against both YouTube and TikTok.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch two key things going forward. First and foremost, rate durability. The 6% will come down, and the real test is whether users stick when it does. If they do, the Super App thesis has legs in the West. Second, the account-suspension risk. Tying your primary banking relationship to a platform with opaque moderation policies creates a genuinely new category of consumer risk that regulators will eventually want to address (especially European regulators don’t like Super Apps in any shape or form). Money transmitter licensing is state-by-state in the U.S. and country-by-country everywhere else. But if 𝕏 clears those hurdles, it validates something the Western market has long assumed was impossible: a real WeChat-style Super App outside China. If it can’t, 𝕏 Money stays a very good neobank feature welded onto a social network. Of course, that isn’t nothing, but it isn’t the vision Elon Musk wants either.

ICYMI:

🧠 What else I’m watching

AI Payment Debut 💳 Crédit Agricole, Mastercard, and Worldline completed France’s first agentic payment transaction in production. A customer used a digital agent to search for festivals by budget, event type, and location, then requested the AI to initiate the purchase. Crédit Agricole handled authentication and authorization with secure, traceable processing. Mastercard France MD says this paves the way for large-scale European deployment. Will this transform payments? Because we’re still very early. ICYMI: Visa and Mastercard’s Agentic AI payment platforms have a volume problem 🤖📊 [what it’s all about, why it matters & why payment titans have a volume problem here + bonus reads into other Visa & Mastercard’s agentic AI moves, & how Google wants to be the OS for all commerce inside]

OKX AI Marketplace 🤖 OKX launched OKX AI, a marketplace where AI agents can work and get paid in stablecoins. The platform includes an Agent Marketplace for listing services and a Task Marketplace for posting work, with escrow and instant payment options. Agents share a persistent identity that builds reputation across all tasks. Supported by Ethereum Foundation, and others, OKX AI is positioned as Upwork for agents. ICYMI:

Atom Sale Collapses 💔 The sale of Atom Bank is nearing collapse after failing to attract offers at the £600 million valuation sought by shareholders, reports the FT. Owners BBVA, Toscafund, and Infinity Investment Partners appointed Jefferies to run the sale, but Pollen Street Capital’s bid was too low, and Yorkshire and Leeds Building Societies opted out. With the sale unlikely, shareholders may push for leadership changes. ICYMI: Starling Bank’s 2026 financials: 2.5x Monzo’s profit on half the revenue, and a £70M SaaS pipeline that changes the IPO math 📈🧠 [unpacking the most important financial facts & figures, how it stacks against Monzo & Revolut, & why Starling’s balance sheet is a fortress + bonus deep dives into the latest financials of Monzo & Revolut inside]

💸 Following the Money

Tokenization firm Securitize eyes early July NYSE debut with $400M SPAC deal.

BR-DGE, the high-growth payments technology company, has secured a £10M funding round.

Framework Ventures raises $400M for fourth fund to invest across crypto, AI, and robotics. ICYMI:

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

6%, but what is the risk?

great stuff, saving for later