Revolut built a trading desk with Claude in 30 mins 😳🤖; Card networks just picked a side on stables, & it’s not against them 💳🪙; Meta’s second crypto act works because it’s not about crypto 📱🪙

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

Productize Yourself 🧠 [Naval Ravikant’s framework for building a one-person company is the best startup strategy of 2026. Here’s the operating system, and 13 AI prompts to run it]

What to Build in 2026 🚀 [The startup ideas every top VC is funding right now, the pitch decks that worked, and how to build them]

Turn Claude Cowork Into Your Personal COO 🧠 [Most people are using the most powerful AI agent ever released to answer questions. Here’s the framework that turns Claude Cowork into an operator that runs your work while you sleep]

Nubank’s Q4 2025: Latin America’s digital banking juggernaut is just getting started (but the market already knows it) 😤📈 [deep dive into their Q4 & full 2025 year financials, breaking down the most important facts and figures, understanding what they mean & what’s next for NU 0.00%↑]

Chime’s flywheel is spinning fast, but can this neobank outrun its own valuation? 🤔🏦 [deep dive into their latest Q4 & full 2025 year financials, breaking down the most important facts & figures, what they mean and whether Chime is worth your time & money in the years to come]

The Android of Commerce - How Google Is Building the Interface Between AI & Money 🤖💸 [why recently introduced WebMCP is a game-changer, how it stacks perfectly into Google’s Android of Commerce playbook, things worth watching, what’s next for FinTechs/Banks/Payments companies, etc. + bonus deep dives into Google’s UCP, how I built an AI OS to run startup with Claude, and how AI is eating software today]

Latin America’s Financial Super App: MercadoLibre’s $29B revenue machine is still in the early innings 🤑📈 [breaking down their latest financials, understanding the bigger picture & why I’m bullish on MercadoLibre + bonus deep dive into Nubank & their latest financials inside]

SoFi just made stablecoin settlement a banking feature, not a crypto experiment 🪙🏦 [what it’s all about, why it could be huge & change lots of things + bonus deep dives into SoFi, Mastercard, and the ultimate list of stables resources inside]

A Million Dollars a Slide 💸 [Auquan’s pitch deck is a masterclass in selling a problem before you sell a product]

Turn Claude From a Chatbot Into a Thinking Partner 🧠 [Most people prompt Claude like it’s Google. Here’s the framework Anthropic actually recommends]

AI Just Killed the User Interface 🧠🖥️ [Anthropic AI launched an app layer inside Claude, & it changed the role of SaaS entirely]

Turn Claude Sonnet 4.6 Into Financial Analyst That Never Sleeps 📊 [Most analysts are leaving 90% of Claude on the table. Here’s the framework that turns the world’s best-value AI into a senior financial analyst]

As for today, here are the 3 incredible FinTech stories that are changing the world of financial technology as we know it. This was yet another insane week in the financial technology space, so make sure to check all the above stories.

Revolut built a trading desk with Claude in 30 minutes 😳🤖

Following the trends 🤖 Two engineers at Revolut X just mass-produced a question that should keep every fintech product leader up at night: if an AI agent can orchestrate your entire system through the API, what exactly is your product team building?

Let’s break this down.

More on this 👉 Nikita Ivanov and Vlad Kaminski, engineers on Revolut’s crypto exchange, connected Claude to the Revolut X API via Anthropic’s Model Context Protocol (MCP) as a side project. Leonid Bashlykov, Revolut’s Head of Crypto Product, then prompted Claude in plain English and had a working market-making strategy running in roughly 30 minutes.

Not a demo. Not a chatbot answering price queries. A full workflow handling inventory management, dynamic quoting, position sizing, execution, monitoring, and Telegram alerts. The kind of thing that normally requires a quant, a developer, backtesting infrastructure, and weeks of iteration.

Let that sink in.

Zoom out 🔎 MCP is the load-bearing detail here. Anthropic released it in November 2024 as an open protocol that lets AI models discover and use external tools through a standardized interface.

Before MCP, every AI integration was bespoke plumbing. Now, a fintech can stand up one MCP server, and any compatible agent can trade, pull data, run backtests, and set alerts against it.

In other words, Revolut built the server; Claude figured out how to use it 🤖

The uncomfortable implication here is less about trading and more about product strategy. Revolut’s own team is now openly asking whether traditional feature roadmaps - design a screen, add a button, ship an update - still make sense when an agent can compose capabilities on its own.

The API surface becomes the product. The UI becomes a monitoring layer.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch for two things in the next 12 months. First, whether Coinbase, Kraken, and Interactive Brokers ship their own MCP layers. If they do, the competitive moat moves from interface design to API richness and execution quality. Second, who builds the permission and risk guardrails that make agent-driven trading palatable to regulators. Crypto is a forgiving sandbox - 24/7 markets, fewer legacy rules. Equities won’t be. The fintech that solves scoped agent permissions (”trade up to $10k/day, BTC and ETH only, kill-switch at 2% drawdown”) for regulated markets will own a very large category. Revolut fired a starting gun. The race is infrastructure, not interfaces. Paradigm shift.

ICYMI:

The card networks just picked a side on stablecoins, and it’s not against them 💳🪙

The news 🗞️ Within 24 hours, both major card networks - Visa & Mastercard - made the same bet. One of them just doesn’t know it yet.

Let me explain.

More on this 👉 On March 3, Bridge - Stripe’s $1.1B stablecoin infrastructure acquisition - announced it’s expanding its Visa-backed stablecoin card program to 100+ countries by year-end, now live in 18. The day before, SoFi and Mastercard announced that SoFiUSD, the bank-issued stablecoin SoFi launched on Ethereum in December, would become a settlement option across Mastercard’s network, with white-label access flowing through Galileo’s 130 million accounts.

Two announcements, two card networks, one conclusion: stablecoin settlement is no longer a pilot.

It’s becoming table stakes.

Zoom out 🔎 The mechanics differ, but the logic is identical. Bridge lets any wallet -Phantom, MetaMask, whoever - issue a branded Visa debit card backed by stablecoin balances. Users spend USDC from their wallets; merchants get fiat; Bridge handles conversion.

Meanwhile, SoFiUSD gives Mastercard a bank-regulated, Fed-reserve-backed stablecoin inside its settlement layer, with none of the opacity concerns that follow USDC or USDT into institutional conversations. Visa is also testing on-chain settlement in parallel through its own pilot, now adding Bridge and Lead Bank alongside Worldpay and Nuvei.

Both networks are quietly rebuilding their back offices while keeping the front-end card experience unchanged.

THE TAKEAWAY ✈️

What’s next? 🤔 What’s easy to miss here is that these moves aren’t symmetric. Visa is betting on infrastructure neutrality - support every stablecoin, every chain, let Bridge abstract the complexity. Mastercard is betting on credential quality - anchor to a regulated bank issuer and win the institutional trust argument. Both strategies could work. They might even reinforce each other if the market segments by use case: consumer spending on Visa rails, institutional settlement on Mastercard’s. Looking ahead, I’d carefully watch Galileo. If SoFi converts even a fraction of its 130 million white-label accounts to SoFiUSD settlement, SoFi stops being a neobank with a stablecoin and becomes the stablecoin infrastructure provider for mid-market fintechs that can’t build this themselves. That’s the non-obvious second-order move. Stripe is playing the same game through Bridge on the card issuance side. Thus, the race isn’t between stablecoins and cards anymore. It’s between Stripe and SoFi for who owns the infrastructure layer underneath both.

ICYMI: SoFi just made stablecoin settlement a banking feature, not a crypto experiment 🪙🏦 [what it’s all about, why it could be huge & change lots of things + bonus deep dives into SoFi, Mastercard, and the ultimate list of stables resources inside]

Meta’s second crypto act works because it’s not about crypto 📱🪙

Following the money 💸 Four years after regulators killed Libra, Meta is back in stablecoins - and the fact that nobody is panicking tells you everything about how much the market has shifted.

Let’s take a quick look at this.

More on this 👉 Meta is now testing stablecoin payments across its apps, with a possible rollout in the second half of 2026, per CoinDesk and Bloomberg. The trial is small. The company has sent an RFP to third-party providers, with Stripe’s Bridge reportedly in the mix.

Spokesperson Andy Stone confirmed the direction on X: “This is about enabling people and businesses to make payments on our platforms using their preferred method.”

No proprietary token this time. No global currency ambitions. Just plumbing.

That’s the point. Libra failed because Facebook tried to become a central bank. The 2019 project spooked regulators, drew fire from Trump himself, and collapsed under the weight of its own ambition.

The 2026 version is the opposite play: Meta as a distribution layer, not issuer. Stripe handles the money movement. Bridge, which Stripe acquired in 2024, handles the stablecoin orchestration. Meta provides the 3.58 billion daily users.

Win-win for everyone.

Zoom out 🔎 The clearest on-ramp is WhatsApp in emerging markets. Hundreds of millions of people in India, Brazil, and Southeast Asia already use it for commerce but remain underserved by traditional banking. Stablecoin rails could undercut the remittance fees those users currently absorb.

Creator payouts on Instagram and Facebook are the second wedge - cross-border settlement that currently bleeds value through legacy corridors.

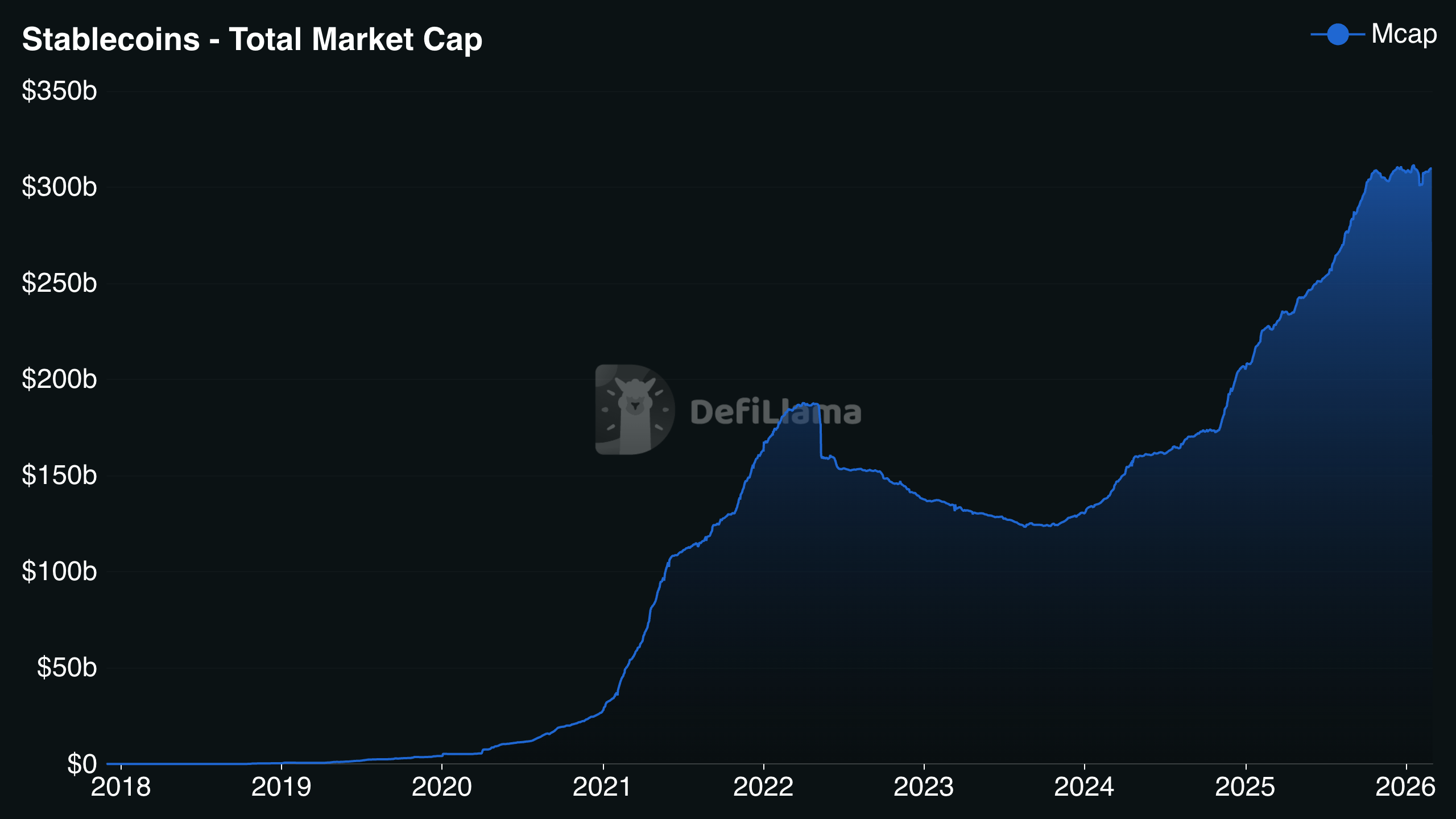

The regulatory picture has also flipped. Trump signed the GENIUS Act last July, giving stablecoin issuers a federal framework. Stablecoin supply passed $300 billion in 2025. Transaction volume hit $33 trillion. Visa and Mastercard are already both on board.

Meta isn’t early to this trade anymore; it’s late, which paradoxically reduces its risk.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, the key thing to watch here isn’t whether Meta launches. It’s the OCC’s proposed rulemaking under the GENIUS Act, which could ban deposit-like rewards on stablecoin balances. PayPal currently offers 3.7% on PYUSD; Coinbase offers 3.5% on USDC savings. If those incentives disappear, stablecoin providers lose their easiest consumer acquisition lever. Meta would need to sell users on lower fees and faster settlement alone - a harder pitch against credit card rewards in developed markets, though still compelling for cross-border flows. The second-order question is this: if the world’s largest social platform normalizes stablecoin payments for billions of users, does that compress margins for every existing payment processor, or does it just validate the rails they’re already building on? Could be both…

ICYMI: Stripe doesn’t need PayPal. That’s why it might buy it 💳♟️ [~3,000 words deep dive into why Stripe doesn’t actually need PayPal and that’s exactly why it might buy it, the real strategic logic most coverage is missing, how Adyen fits into the picture, the Elon Musk angle, and what a deal would mean for the entire payments industry + lots of bonus reads & resources on Agentic Commerce, AI in Finance, etc. inside]

What else I’m watching

Santander and Mastercard Pioneer AI Payments 🤖 Banco Santander and Mastercard have successfully completed Europe’s first live end-to-end payment executed by an AI agent, marking a significant advancement in agentic AI within a regulated banking environment. The solution, processed through Santander’s infrastructure and Mastercard Agent Pay, ensures security and privacy standards while enabling AI agents to conduct transactions on behalf of customers. Currently in the pilot stage, the next phase focuses on achieving technical and operational readiness for AI-driven payments. ICYMI:

CaixaBank Introduces AI Purchase Assistant 🛒 CaixaBank has launched an AI agent to assist customers with in-app purchases, including helping them specify needs, provide information, and resolve queries. Currently, the agent aids customers with pre-approved loan applications, guiding them through loan configurations and terms. Based on Salesforce’s Agentforce, this technology is set to expand across all recruitment chats within the bank’s app, aiming to improve efficiency and customer service. ICYMI:

Citi Launches AI Banking Unit 🏦 Citi has created a new AI-focused Infrastructure Banking unit to provide advisory and lending services for data centers, computing capacity, and related digital assets, anticipating a $3 trillion capital requirement by 2030 for AI infrastructure expansion. The bank has made its first investment in Japan with Sakana AI, a company known for developing innovative AI models and solutions aimed at enhancing operational efficiencies across industries. ICYMI:

💸 Following the Money

Visa is reportedly joining Qatar Holding and the Abu Dhabi Investment Authority to invest more than $200M as anchor investors for the forthcoming US IPO of Softbank’s PayPay. ICYMI: World’s Tollbooth: Visa’s unbeatable moat justifies premium valuation, but upside is limited 🤷♂️💳 [breaking down the most important Q1 2026 financial facts & figures, understanding what they mean, and what’s next for Visa]

Stablecoin payments startup Cyclops raises $8M from Castle Island Ventures, F-Prime, and Shift4.

Flowpay, a European fintech focused on supporting SMEs with access to capital, is expanding across key European markets with the acquisition of Tapline.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

Revolut & Claude? That wasn't on my 2026 bingo card...