Revolut is finally a bank in the UK 🇬🇧🏦; Mastercard & Google just open-sourced the missing trust layer for AI that spends money 🤖💸; Ramp just gave AI Agents their own credit cards 😳💳

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

Sequoia’s “Services: The New Software” Thesis Will Mint Billionaires and Bankrupt Copycats 📈 [The autopilot playbook, the margin trap, the $0.03 problem, and a practical framework for AI builders, investors, and operators who need to decide what to do next]

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

Productize Yourself 🧠 [Naval Ravikant’s framework for building a one-person company is the best startup strategy of 2026. Here’s the operating system, and 13 AI prompts to run it]

Turn Claude Cowork Into Your Personal COO 🧠 [Most people are using the most powerful AI agent ever released to answer questions. Here’s the framework that turns Claude Cowork into an operator that runs your work while you sleep]

Turn Claude in Excel Into Your Senior Financial Analyst 📈 [Excel users are leaving 90% of Claude on the table. Here’s the framework & 15 prompts that turn a $20 sidebar into the most powerful analytical tool in your spreadsheet 🤖]

Japan’s cash graveyard just found its gravedigger: why PayPay may be the most asymmetric FinTech IPO of the decade 😳🇯🇵 [unpacking the closed-loop payments model, the lending engine hiding inside, and the SoftBank governance question to figure out whether this is the most asymmetric fintech IPO setup in years + cornerstone bets from Visa, Qatar Holding, and Abu Dhabi Investment Authority tell you the smart money is already paying attention & a bonus dive into Brazil’s PicPay inside]

The Android of Commerce - How Google Is Building the Interface Between AI & Money 🤖💸 [why recently introduced WebMCP is a game-changer, how it stacks perfectly into Google’s Android of Commerce playbook, things worth watching, what’s next for FinTechs/Banks/Payments companies, etc. + bonus deep dives into Google’s UCP, how I built an AI OS to run startup with Claude, and how AI is eating software today]

X Money’s real product isn’t banking - it’s lock-in 📲🔐 [why banking isn’t the real product here, what Elon’s master plan really is & what to watch next + bonus deep dive into Muskonomy, the closed-loop economy no bank can touch]

Nasdaq’s tokenization play isn’t about 24/7 trading. It’s about who issues the token 📈🪙 [why it’s not about 24/7 trading at all, where the real value unlock is & what to expect next]

A Million Dollars a Slide 💸 [Auquan’s pitch deck is a masterclass in selling a problem before you sell a product]

Turn Claude From a Chatbot Into a Thinking Partner 🧠 [Most people prompt Claude like it’s Google. Here’s the framework Anthropic actually recommends]

Turn Claude Sonnet 4.6 Into Financial Analyst That Never Sleeps 📊 [Most analysts are leaving 90% of Claude on the table. Here’s the framework that turns the world’s best-value AI into a senior financial analyst]

As for today, here are the 3 fascinating FinTech stories that are transforming the world of financial technology as we know it. This was yet another wild week in the financial technology space, so make sure to check all the above stories.

Revolut is finally a bank in the UK 🇬🇧🏦

The BIG News 🔥 The 4-year wait for the most valuable FinTech in Europe is finally over, but the UK banking licence itself isn’t the news 🤫

What matters here is what the Prudential Regulation Authority actually stress-tested before signing off: Revolut’s worldwide compliance infrastructure, not just its UK operations.

Let’s unpack this, understand why it matters, and what’s next for the $75 billion fintech heavyweight.

More on this 👉 Revolut received full UK banking approval yesterday, exiting an extended mobilisation phase that ran 20 months - nearly double the standard timeline. Ouch 😬

The PRA’s review went far beyond domestic readiness. Regulators explicitly examined the company’s risk management, AML controls, and IT systems across 40+ countries, knowing that overseas watchdogs would treat the UK approval as a reference point.

Nik Storonsky has admitted that Revolut’s early “grow fast and break things” philosophy was a mistake, and the company has since hired hundreds in risk and compliance to prove it.

Zoom out 🔎 The immediate unlocks are straightforward:

→ FSCS deposit protection for 13 million UK customers,

→ lending products (personal loans, credit cards, overdrafts), and

→ unlimited deposit-taking that creates a low-cost funding base to diversify beyond FX and crypto fees.

Existing customers will migrate from the e-money entity to Revolut Bank UK Ltd over several months.

But the second-order effect is where the real value sits. Revolut filed for a US national bank charter on roughly March 5 - timing that’s not coincidental. The PRA’s approval now functions as a credibility stamp for the OCC and FDIC review, arriving just as the Trump administration signals openness to new bank entrants.

A new US CEO (ex-Visa) and $500 million earmarked for the American push reinforce that this is a sequenced strategy, not a coincidence.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch three things from here. First, UK credit losses: Revolut has never managed a domestic lending book through an economic cycle, and the UK consumer outlook is soft. Second, IPO timing - the licence removes the last major overhang, and a 2026-27 London listing now looks probable (at least technically). Third, whether the 100-million-customer target by mid-2027 holds up against the operational drag of being a regulated bank in dozens of jurisdictions simultaneously. All in all, the tension between Revolut’s Super App ambitions (crypto, AI, insurance) and traditional banking guardrails still hasn’t been resolved. It’s just been licensed. But the capabilities are much bigger now as well, so there’s nothing else apart from being bullish here.

ICYMI:

Mastercard and Google just open-sourced the missing trust layer for AI that spends money 🤖💳

Following the machine economy 🤖 Only ~16% of U.S. consumers trust AI to make payments on their behalf. Mastercard and Google just shipped the spec designed to change that.

Last week, Mastercard quietly released Verifiable Intent, an open-source framework that creates cryptographic proof an AI agent is doing exactly what its human authorized - nothing more, nothing less.

Think of it as a digitally signed power of attorney with machine-enforceable constraints: amount caps, merchant allowlists, budget periods, and product categories.

The agent can act autonomously, but the boundaries are tamper-evident and auditable. It’s built on SD-JWTs aligned with W3C Verifiable Credentials and works across Google’s Agent Payments Protocol, Universal Commerce Protocol, and anything else that wants to plug in.

Let’s break this down, and most importantly - understand why it could change the game of agentic payments.

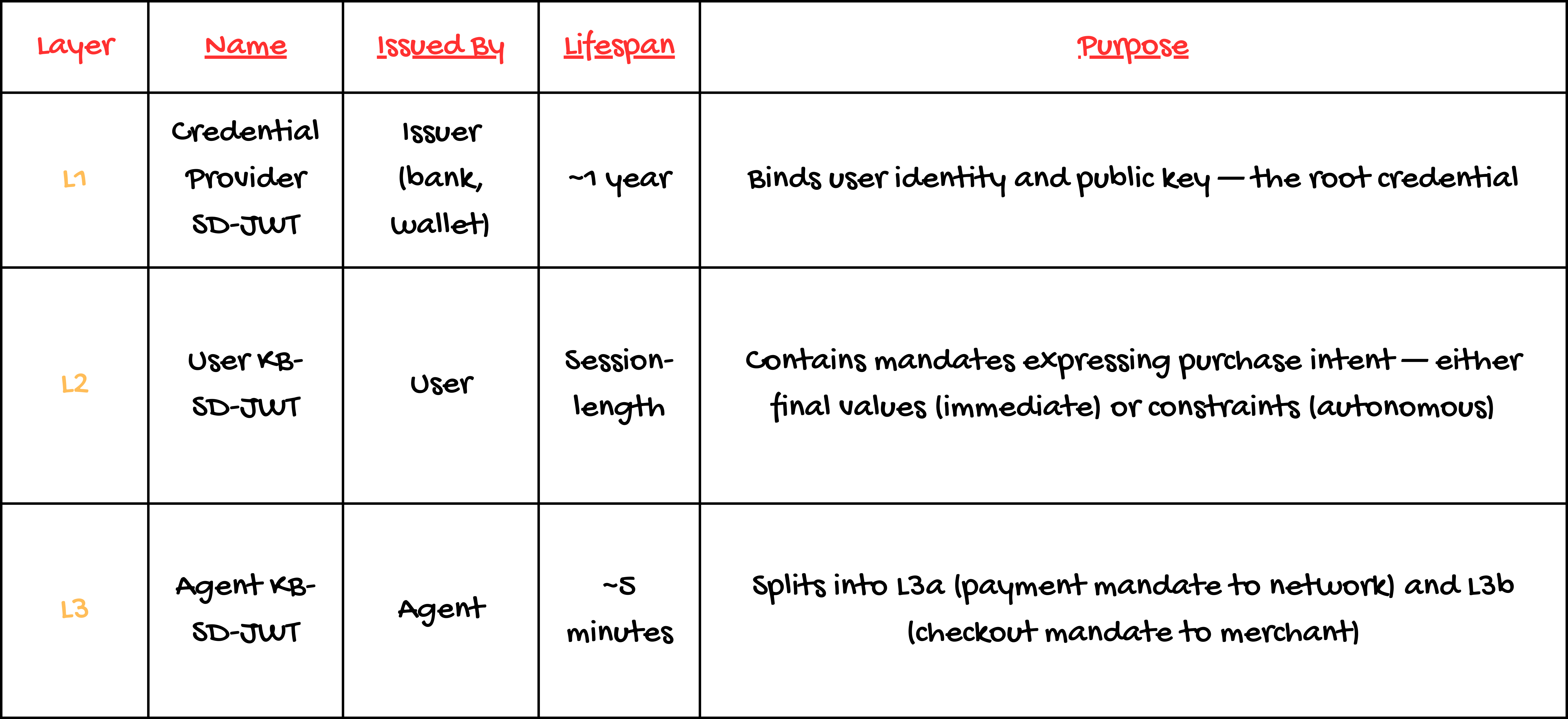

More on this 👉 The architecture of Verifiable Intent runs three layers.

→ A credential provider (bank, wallet) binds the user identity.

→ The user issues a scoped mandate to their agent.

→ When the agent transacts, it signs proof of compliance against that mandate.

Merchants see only what they need. Issuers can distinguish legitimate agent activity from compromise.

Disputes get simple: the cryptographic trail either confirms the agent stayed in bounds or it doesn’t.

Adyen, Fiserv, Checkout.com, Worldpay, and IBM have already endorsed it.

The Python SDK and runnable examples are live on GitHub under Apache 2.0 today.

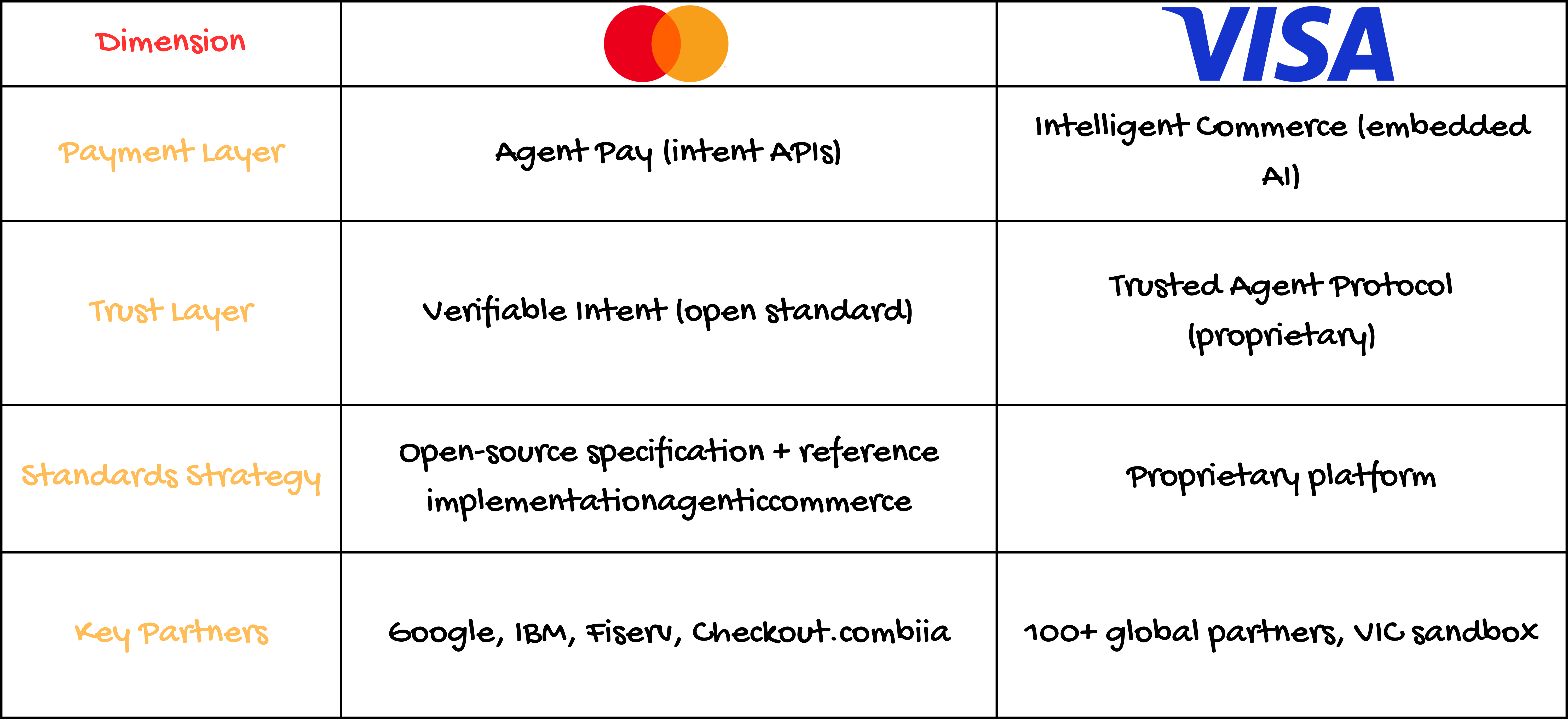

Zoom out 🔎 The strategic logic here is pure Mastercard. Open-source the standard, let everyone adopt it, then sit at the center of the verification network - the same playbook that made EMV chip ubiquitous while keeping the card networks indispensable.

Visa’s Intelligent Commerce sandbox has more live agent transactions, but no equivalent open intent spec.

That’s a telling choice: Visa is building a product, Mastercard is seeding infrastructure. History tends to favor the latter.

THE TAKEAWAY ✈️

What’s next? 🤔 Every payments era has a trust primitive that unlocks it. Mag stripes answered “is this card real?” Tokenization answered “can we keep credentials safe online?” Now, Mastercard & Google published the answer to the next question: “did this AI agent actually have permission to spend that money?” For fintechs building AI-native interfaces - Revolut integrating Claude, Klarna’s AI assistant, anyone wiring LLMs into financial workflows - this collapses the biggest open question their compliance teams face. The liability surface for autonomous agent spending just got a formal, auditable boundary. But the fastest adoption won’t come from consumer shopping agents. It’ll come from B2B procurement, where AI agents reordering supplies within cryptographically enforced corporate spending policies is a CFO’s dream with an immediate ROI case. Watch enterprise card programs quietly converting to scoped agent mandates within 18-24 months. The race now isn’t to build the best AI shopping agent. It’s to become the default trust layer those agents rely on. Mastercard just fired the starting gun and handed out the track at the same time. Well played, well played 👏

ICYMI: The Android of Commerce - How Google Is Building the Interface Between AI & Money 🤖💸 [why recently introduced WebMCP is a game-changer, how it stacks perfectly into Google’s Android of Commerce playbook, things worth watching, what’s next for FinTechs/Banks/Payments companies, etc. + bonus deep dives into Google’s UCP, how I built an AI OS to run startup with Claude, and how AI is eating software today]

Permanent Number Two: Mastercard’s quality is unquestionable, but so is the valuation 🤔📈 [deep dive into their Q4 2026, what stood out, and whether Mastercard is worth your time & money in the years to come]

World’s Tollbooth: Visa’s unbeatable moat justifies premium valuation, but upside is limited 🤷♂️💳 [breaking down the most important Q1 2026 financial facts & figures, understanding what they mean, and what’s next for Visa]

Ramp just gave AI Agents corporate cards, and solved the right problem 🤖💳

The news 🗞️ AI agents can reason, plan, and execute multi-step workflows. What they couldn’t do, until this week, was spend money without someone handing them a credit card number and hoping for the best.

$32 billion FinTech giant Ramp just solved that, so let’s unpack this.

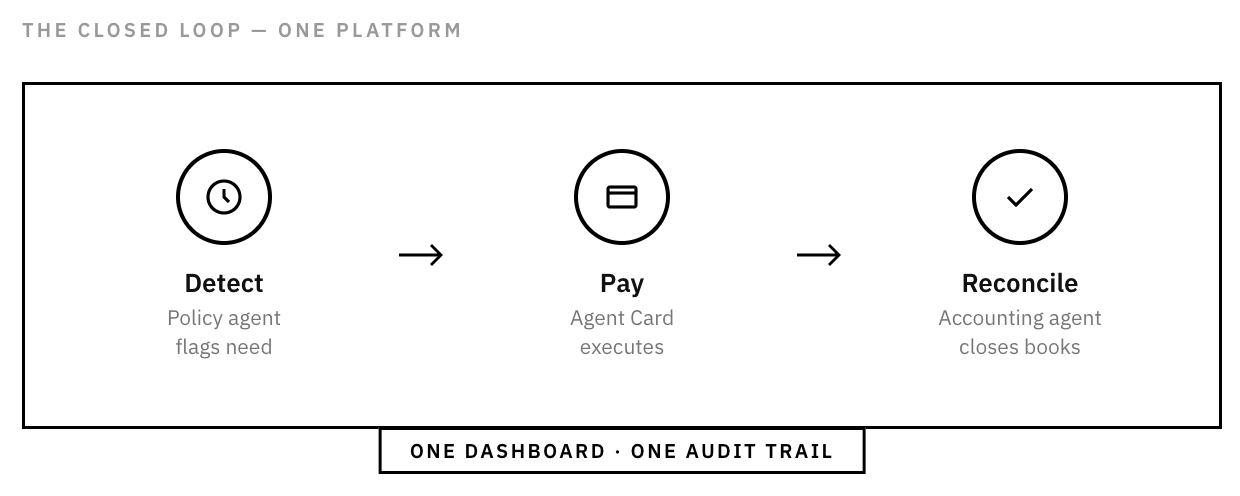

More on this 👉 Ramp’s new Agent Cards are virtual corporate cards issued to AI agents under a business’s existing Ramp account. The agent never sees a card number.

→ It calls an API, CLI, or Anthropic’s Model Context Protocol to request a payment;

→ Ramp’s backend enforces hard spend limits, merchant whitelists, and category blocks before anything clears.

→ Every transaction logs with full context - which agent, what task, what reasoning led to the purchase.

Early access is waitlist-only, tied to Ramp’s 50,000-business customer base.

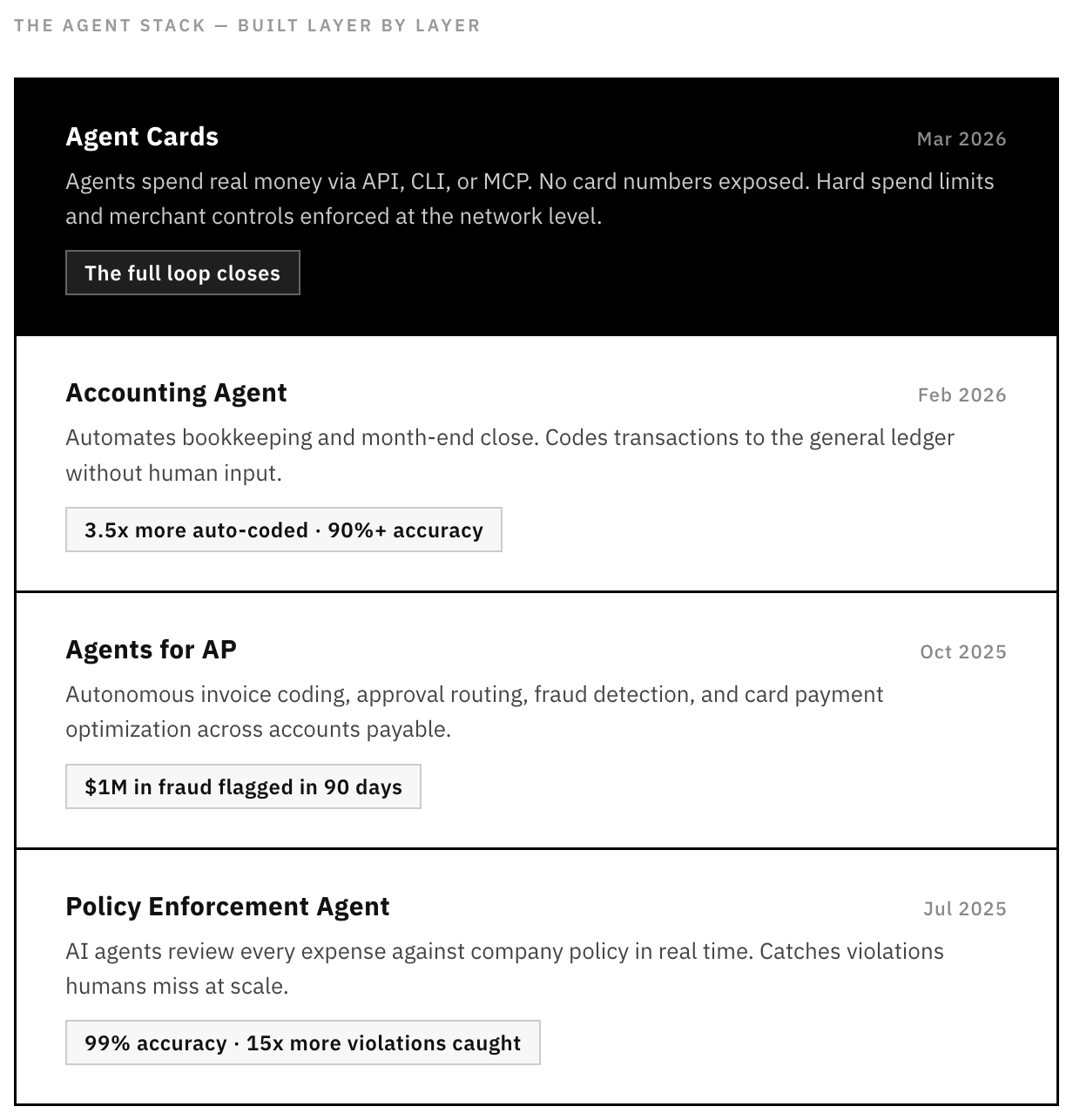

Zoom out 🔎 The product itself is straightforward. What makes it interesting is what it sits on top of. Ramp spent the past year shipping AI agents for expense policy enforcement (99% accuracy, 15x more violations caught), accounts payable (flagging $1M in invoice fraud in 90 days), and automated bookkeeping.

Agent Cards are the last layer: agents that already read, decide, and reconcile can now pay. The full loop closes inside one platform, one dashboard, one audit trail.

The timing matters because the rest of the ecosystem is converging fast. Visa recently launched Intelligent Commerce with 100+ partners and agent-specific tokenization. Mastercard rolled Agent Pay to all U.S. cardholders and most recently - Verifiable Intent. Stripe and OpenAI published an Agentic Commerce Protocol.

McKinsey projects up to $1 trillion in U.S. agent-orchestrated retail by 2030. Everyone agrees agents will transact. The open question was who would own the governance layer for corporate spend. Ramp just planted a flag.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, watch two things. First, whether Ramp’s data moat -billions in monthly business spend, GL coding patterns, vendor relationships across 50k customers - lets it make smarter authorization decisions than pure-play card issuers like Lithic or Marqeta can match. Second, the liability question no one has answered: when an agent overspends or buys the wrong thing, who’s on the hook? Ramp, the agent builder, or the business? The product works today because spend limits are tight and use cases are narrow. The real test comes when someone sets a $50,000 procurement budget and lets an agent run. That’s going to be the deciding factor, but either way - Agentic Finance is the future.

ICYMI:

What else I’m watching

BBVA Enhances Audits with AI 🤖 BBVA has integrated an AI assistant to streamline its internal audit processes, reducing manual programming and documentation work. This tool, developed within ChatGPT Enterprise, guides auditors within a consistent framework, improving productivity by around 10% in data-intensive audits without replacing human judgment. The initiative is part of BBVA’s broader collaboration with OpenAI to enhance efficiency and consistency in audits. ICYMI:

ECB Unveils Tokenized Financial Ecosystem Plan 🏛️ The European Central Bank (ECB) has introduced Appia, a long-term initiative to shape a European tokenized financial ecosystem using central bank money. Alongside Pontes, a DLT platform launching in Q3 2026 for central bank money settlement, Appia aims to explore the design of a wholesale financial ecosystem based on tokenization and DLT. Following extensive experiments with market participants, the ECB plans to publish a blueprint for this ecosystem in 2028, with ongoing work informing the development of tokenized market infrastructures and services. ICYMI: Nasdaq’s tokenization play isn’t about 24/7 trading. It’s about who issues the token 📈🪙 [why it’s not about 24/7 trading at all, where the real value unlock is & what to expect next]

Robinhood Launches Platinum Card 💳 Robinhood has introduced an invite-only platinum credit card with a $695 annual fee, targeting the high-income market with benefits such as higher credit limits, 5% cash back on dining, health and wellness perks, and 10% cash back on hotels and rental cars. The card aims to offer over $3000 in annual value. Additionally, Robinhood is launching custodial accounts, enabling parents and guardians to invest on behalf of minors, with assets transferred to the child upon reaching the age of majority. ICYMI: Robinhood: the $4.5 billion revenue dark horse that Wall Street still underestimates 🤷♂️📉 [deep dive into their Q4 & full year 2025 financials, what stands out, and why I’m still really bullish]

💸 Following the Money

Kast, a global financial platform built on stablecoin rails founded by former Circle executive Raagulan Pathy, has raised $80M in a Series A funding round co-led by QED Investors and Left Lane Capital. ICYMI:

Outpost, an AI-powered platform that enables merchants to sell worldwide with zero liability, has raised $17.5M in Series A funding led by Ribbit.

Irish insurtech Kayna raises €1.5M.

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

This is gold - thanks so much - arguably the best weekly issue this year so far... Aciu!