AI Agents got Credit Cards. Nobody built the fraud stack 💳; Upstart’s Bank charter bid is a breakup letter to its own biz model 🏦; Sam Altman is building the passport office for AI agents 🤖

You're missing out big time... Weekly Recap 🔁

👋 Hey, Linas here! Welcome back to a 🔓 weekly free edition 🔓 of my daily newsletter. Each day, I focus on 3 stories that are making a difference in the financial technology space. Coupled with things worth watching & most important money movements, it’s the only newsletter you need for all things when Finance meets Tech.

If you’re not a subscriber, here’s what you missed this week:

The Ultimate Guide to Claude Skills 🧠 [You’re typing the same instructions every morning. After reading this, you’ll never do it again]

Andrej Karpathy’s Method To 10X Your Claude Skills 🧠 [You built the Skills. Now here’s the step-by-step system that makes them dramatically better while you sleep]

Sequoia’s “Services: The New Software” Thesis Will Mint Billionaires and Bankrupt Copycats 📈 [The autopilot playbook, the margin trap, the $0.03 problem, and a practical framework for AI builders, investors, and operators who need to decide what to do next]

Mastercard paid $1.8 billion for stablecoin FinTech BVNK because it can’t afford not to 🤫🪙 [what the deal is all about, why it matters for Mastercard and what it means for the broader FinTech & Finance space + bonus deep dive into Mastercard’s latest financials, how it’s building the trust layer for AI agents & the ultimate list of stables resources inside]

Stripe just built the toll booth for the machine economy 🤖🪙 [breaking down the Machine Payments Protocol, why it’s huge & how MPP stacks against other Agentic Protocols + bonus deep dive into Stripe building the infra for AI-driven payments and how Google wants to become the Android of Commerce]

Turn Claude Cowork Into Your Personal COO 🧠 [Most people are using the most powerful AI agent ever released to answer questions. Here’s the framework that turns Claude Cowork into an operator that runs your work while you sleep]

Turn Claude in Excel Into Your Senior Financial Analyst 📈 [Excel users are leaving 90% of Claude on the table. Here’s the framework & 15 prompts that turn a $20 sidebar into the most powerful analytical tool in your spreadsheet 🤖]

Visa developed a credit card for AI and shipped it the same day stablecoins got their own payment standard 🤖💳 [what it is & why Visa is doing it, how it stacks with MPP and what to expect next + bonus deep dive into Visa’s latest financials, and how I turned Claude Cowork into my personal COO that does the work while I sleep]

Ramp just bought a 15-person Swedish FinTech. It was really buying a continent 🇪🇺💸 [why the acquisition of the 15-person Swedish FinTech is really about “buying” the continent, how both M&As strategically fit into Ramp’s global strategy & what to watch for next + bonus deep dive into the brilliant rivalry of Brex vs. Ramp & how Ramp gave AI agents their cards]

The One-Person Unicorn 🦄 [I built an AI operating system to run a startup with Claude]

Productize Yourself 🧠 [Naval Ravikant’s framework for building a one-person company is the best startup strategy of 2026. Here’s the operating system, and 13 AI prompts to run it]

As for today, here are the 3 incredible FinTech stories that are changing the world of financial technology as we know it. This was yet another solid week in the financial technology space, so make sure to check all the above stories.

AI Agents just got a Credit Card. Nobody built the fraud stack 🤖💳

The news 🗞️ A 15-second video recently broke X & LinkedIn FinTech: Claude, Anthropic’s AI agent, autonomously generating a funded prepaid Visa card, retrieving the full PAN/CVV, and completing an online purchase.

No human touched the checkout.

The tool behind it, AgentCard, uses Anthropic’s Model Context Protocol to issue disposable virtual cards loaded with exact dollar amounts via Stripe. It works anywhere Visa is accepted. Setup takes 5 minutes, no code required.

Let’s take a look at this.

More on this 👉 The spending capability is real and live in beta. But the risk infrastructure for agent-initiated transactions barely exists.

Accenture found that 85% of financial institutions say their current systems can’t handle high-volume agent-driven payments. That gap between capability and defense is where the real money is.

AgentCard’s design is smart. Prepaid, amount-locked cards mean an agent can’t overdraft or go rogue beyond its budget. But the attack surface is new and strange. Prompt injection could trick an agent into buying $500 in gift cards. Hallucinated intent could trigger purchases nobody approved. And every transaction looks identical from the issuer’s side: API call, virtual card, instant checkout.

Traditional fraud signals like device fingerprints, login patterns, and human typing cadence now tell you nothing.

Zoom out 🔎 Looking at the bigger picture, we must note that legacy fraud vendors built their entire models around human behavior. The companies that win the next cycle will be those rebuilding from the ground up for machine actors.

A handful of startups are already positioning here. Oscilar*, out of Palo Alto, shipped autonomous risk agents in 2025 that score transactions in under 100 milliseconds against behavioral baselines designed for non-human patterns. Sardine and SEON are adjacent but haven’t made the same explicit bet on agentic commerce. Mastercard is working on cryptographic Verifiable Intent proofs.

But nobody has really locked it down yet.

ICYMI:

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, the forward picture is less about whether agents will spend money and more about who controls the trust layer when they do. Every virtual card issuer, every Stripe integration, every MCP-connected agent will need real-time risk scoring purpose-built for non-human behavior. McKinsey’s $3-5 trillion projection for agent-driven commerce by 2030 makes the fraud stack a chokepoint, not an add-on. Thus, watch for “Know Your Agent” verification standards to emerge alongside KYC, and expect the first wave of agent-specific liability frameworks from Visa and Nacha before year-end. Most importantly, the companies building fraud infrastructure for machines, not against them, own the rails of whatever comes next.

*Disclaimer: I’m part of Oscilar.

ICYMI:

Upstart’s Bank charter bid is a breakup letter to its own business model 🏦🤷♂️

The news 🗞️ The fintech that built its name connecting borrowers to other people’s banks now wants to become one.

Upstart filed applications with the OCC and FDIC last week to establish Upstart Bank, a branchless, Delaware-based national bank serving all 50 states. The company is also applying to the Fed to become a bank holding company.

If approved, it would take deposits, lend directly from its balance sheet, and operate under a single federal framework instead of a patchwork of state licenses that left 40,000 consumers unable to even apply in 2024.

Let’s unpack this.

More on this 👉 The company insists it isn’t abandoning its partners. About 95% of Upstart-originated loans are currently sold to its 100-plus bank and credit union partners, and Upstart says it intends to maintain that ratio post-charter.

Annie Delgado, the chief risk officer tapped to run Upstart Bank, told American Banker the bank would rely on brokered deposits rather than competing for local customers. Paul Gu, the incoming CEO, framed the move as “the natural evolution of our business.”

The financials back the timing: Upstart posted roughly $1 billion in 2025 revenue, up 64% year-over-year, and swung to an $18.6 million quarterly profit after years of losses.

Zoom out 🔎 But here’s what’s actually happening. Upstart joins a wave that’s starting to look like a migration. At least 18 charter applications hit the OCC last year alone. Revolut, Nubank, Mercury, and Bunq have all filed. Nubank already has conditional approval. Erebor got a full green light in under four months. PayPal and Affirm are pursuing industrial loan company licenses.

The marketplace-and-partner playbook that defined fintech’s first decade is giving way to something more direct.

THE TAKEAWAY ✈️

What’s next? 🤔 First and foremost, we must note that the 95% sell-through pledge deserves skepticism. Once Upstart holds a charter and deposit funding, the unit economics of lending off its own balance sheet will be hard to ignore, especially with 90%+ automation already in place. On top of that, the charter doesn’t just reduce costs; it shifts who captures the spread. Upstart’s bank partners should be reading the fine print carefully, because the distribution channel they’ve relied on is slowly building its own vault. Most importantly, the fintechs aren’t coming for the banks anymore. They’re becoming them.

ICYMI:

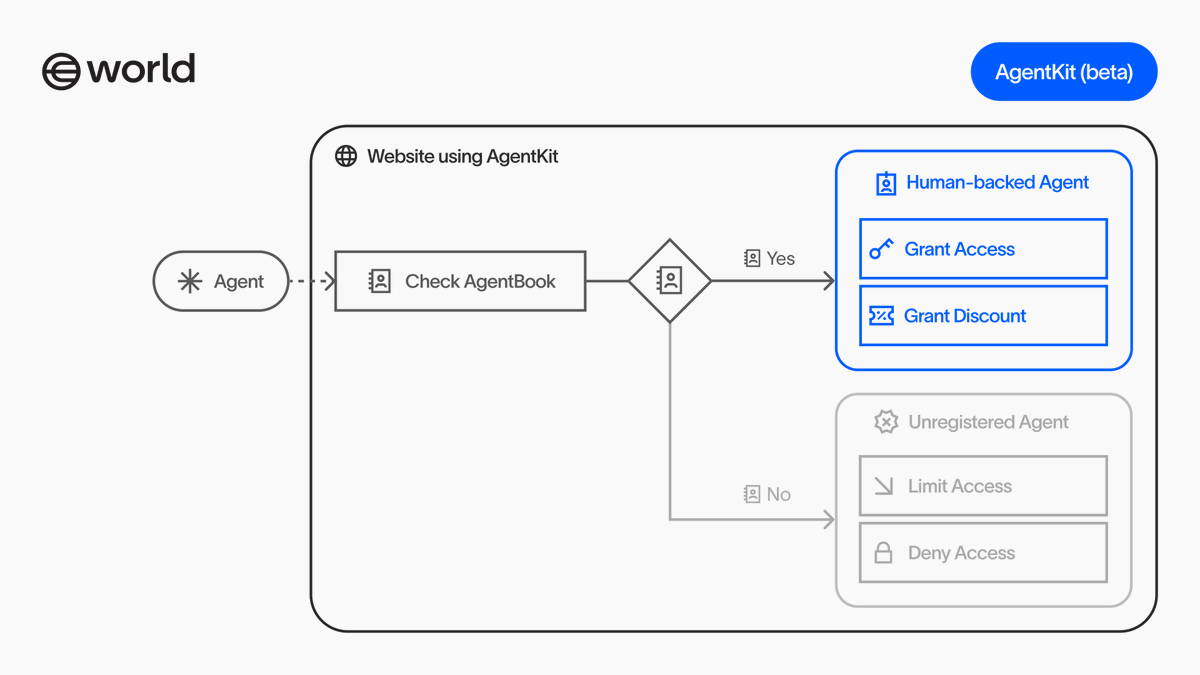

Sam Altman is building the passport office for AI agents 🤖🪪

The news 🗞️ The man whose company created the bot problem now wants to sell the identity layer that governs which bots get in. Makes sense, right? 😅

Let’s unpack this.

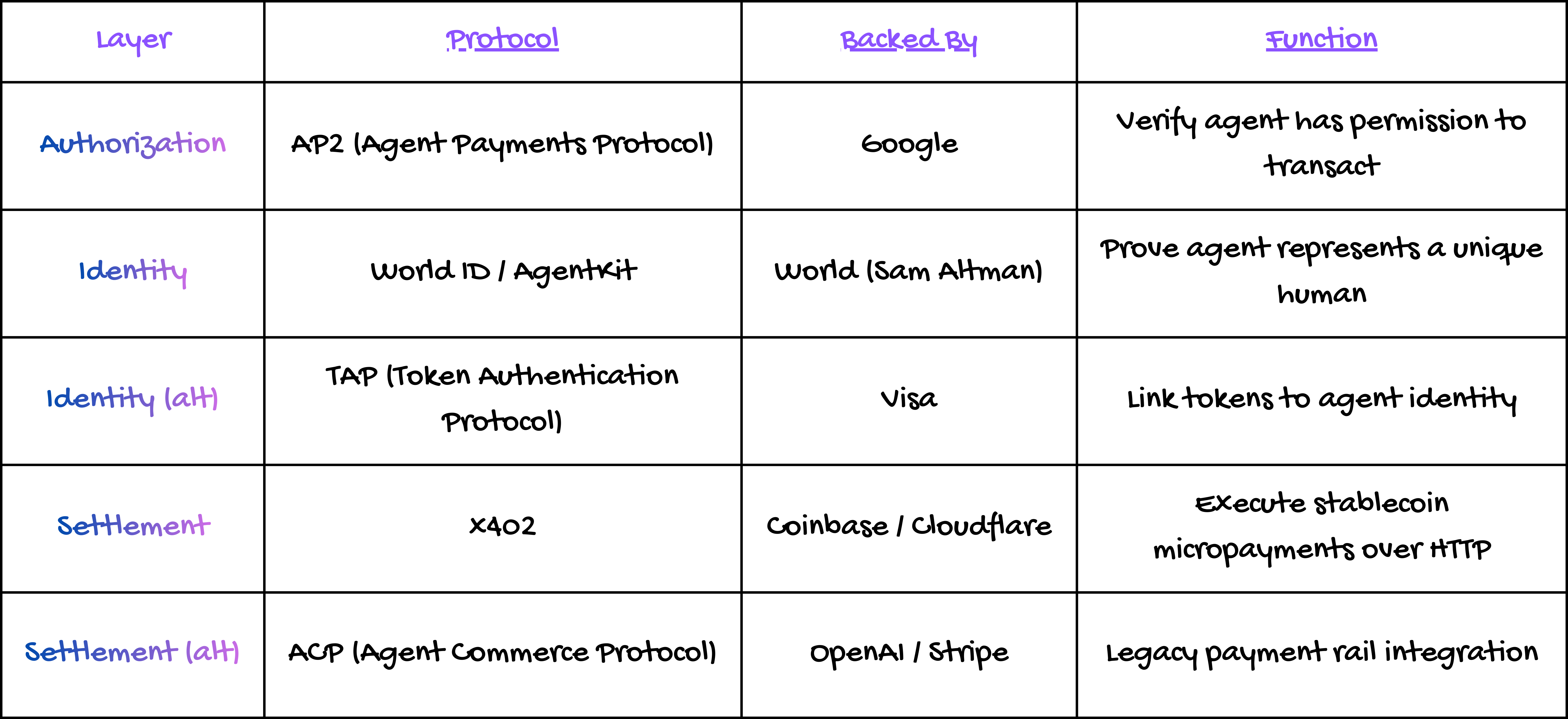

More on this 👉 Yesterday, World - the iris-scanning identity network Sam Altman co-founded - launched AgentKit in beta, a developer toolkit that lets verified humans delegate their World ID to AI agents.

Integrated with Coinbase and Cloudflare’s x402 micropayment protocol, it gives platforms a way to distinguish your personal shopping agent from a coordinated swarm of a thousand bots pretending to be a thousand people. One human, one cryptographic credential, privacy preserved through zero-knowledge proofs, 18 million verified users across 160+ countries already in the network.

Zoom out 🔎 The timing is pointed here. The x402 protocol has processed over 100 million micropayments since launching in 2025, and Stripe, Google, and Anthropic have all built integrations.

Micropayments solve the “how” of agent commerce - agents can pay for API calls, data, and services without human intervention. But payments alone can’t solve Sybil attacks. A well-funded operator can spin up thousands of wallets, each paying fractions of a cent, and no platform can tell them apart. AgentKit adds the missing “who”: proof that a unique biometrically-verified human authorized each agent, without revealing which human.

The use cases write themselves. Resy blocks reservation scalpers not by charging $20 per booking attempt but by enforcing one reservation per verified person. Ticketing platforms stop bot armies. Free-trial abuse disappears.

THE TAKEAWAY ✈️

What’s next? 🤔 Looking ahead, we can clearly see two competing agentic payment ecosystems forming: OpenAI/Stripe (ACP protocol) versus Google/Coinbase (x402). Altman has a foot in both camps - CEO of OpenAI, co-founder of World - which looks less like a conflict and more like a hedge. Finance will be the proving ground: every agent-initiated trade, loan inquiry, or fund transfer needs proof of authority, identity, and compliance in a single integration. Whoever owns that trust layer owns the toll road.

More importantly, the real risk here isn’t technical. It’s that the agentic economy’s identity infrastructure ends up controlled by one company, verified through proprietary hardware, governed by the same person building the agents themselves. Kenya already ruled World’s biometric collection illegal. Spain ordered data deleted. If AgentKit scales to billions of agent interactions, the question isn’t whether proof-of-personhood becomes essential infrastructure. It’s whether a single company should be the one issuing the passports.

ICYMI: The Android of Commerce - How Google Is Building the Interface Between AI & Money 🤖💸 [why recently introduced WebMCP is a game-changer, how it stacks perfectly into Google’s Android of Commerce playbook, things worth watching, what’s next for FinTechs/Banks/Payments companies, etc. + bonus deep dives into Google’s UCP, how I built an AI OS to run startup with Claude, and how AI is eating software today]

What else I’m watching

Experian Integrates Credit Score Tool in ChatGPT 📊 Experian has introduced a postcode-based credit score comparison tool within ChatGPT for UK users. This tool allows users to compare typical credit scores across different postcode areas and age groups using aggregated and anonymized data. It also provides a straightforward way for users to check their personal Experian credit score, aiming to make credit score information more accessible, especially for younger users who frequently use conversational AI for financial queries. ICYMI:

Chaseit.ai Launches AI Loan Servicing Agents 🤖 Chaseit.ai, a Lithuanian fintech startup, has launched AI agents to automate loan servicing and customer communications in call centers. These AI agents can verify customer identity, remind borrowers about payments, negotiate repayment plans, and escalate complex cases to human agents. The company is already handling over 20,000 automated calls daily and aims to expand its services to become a comprehensive loan servicing platform, with plans to raise a seed round in the coming months. ICYMI:

Nordea to Cut 1,500 Jobs with AI 💼 Nordea, the largest bank in the Nordics, is set to reduce its workforce by 1,500 jobs as part of its AI-driven cost-saving strategy, Nordic Scale. The bank aims to achieve at least $600 million in cost savings by 2030 through technology, data, and artificial intelligence. The restructuring will incur costs of about €190 million in Q1 2026 and is expected to result in fewer employees in the future, with approximately 1,500 positions impacted in 2026 and 2027. AI-first or replaced… ICYMI:

💸 Following the Money

Cryptio, a provider of enterprise resource planning software for digital asset operations, has raised $45M in a Series B funding round.

Fuse, an AI-native loan origination and account opening platform trusted by more than 100 credit unions, has raised $25M.

Robinhood Ventures Fund I announced it has closed investments in Stripe and ElevenLabs. Robinhood Ventures Fund I, which is the first fund from Robinhood Ventures, began trading on the New York Stock Exchange on March 6, 2026. ICYMI:

👋 That’s it for today! Thank you for reading, and have a relaxing Sunday! And if you enjoyed this newsletter, invite your friends and colleagues to sign up:

banger!